Sales Pipeline Quality: The CFO’s Most Underrated Revenue Lever Most revenue conversations center on pipeline size. The more consequential conversation is about pipeline quality. For finance leaders, the distinction is not semantic. It is the difference between a forecast that holds and one that falls apart at close. Sales pipeline quality determines not only whether deals convert but whether they renew, expand, and contribute to durable margin. When pipeline is polluted with low-fit opportunities, the consequences extend far beyond missed quota. Forecasts become unreliable, hiring plans misalign, and capital flows toward the wrong segments. This article examines how a rigorous approach to customer fit, early disqualification, and pipeline quality metrics can transform the revenue system from a volume engine into a precision instrument. It draws on over twenty-five years of finance leadership across cybersecurity, SaaS, logistics, digital marketing, and nonprofit sectors, and on the hard-won insight that fit is not a feature of the product. It is a feature of the system. byadminJune 5, 2026

Lease Accounting ASC 842: What Every CFO Needs to Know For decades, lease obligations lived in the footnotes of financial statements, quietly understating corporate leverage and obscuring economic reality. Lease accounting under ASC 842 changed that. Issued by the Financial Accounting Standards Board, the standard requires companies to recognize a right-of-use asset and a corresponding lease liability for virtually all leases with terms exceeding twelve months. The implications extend well beyond journal entries. They affect leverage ratios, covenant structures, return metrics, and the financial narrative presented to boards and investors. For CFOs navigating capital-intensive or multi-jurisdiction operating models, ASC 842 demands not only technical compliance but strategic interpretation. This article examines what the standard requires, how its classification framework operates, where implementation risk concentrates, and why finance leaders who engage with it rigorously will find it a genuine instrument of capital clarity rather than a compliance burden. byadminJune 4, 2026

What Is ABM and Why Every CFO Should Treat It as a Financial Operating System Account-Based Marketing, or ABM, is widely understood as a targeted marketing approach. It is less widely understood as a capital allocation decision. For CFOs and senior finance executives, that distinction carries real strategic weight. ABM is a focused growth strategy. It moves companies away from volume-driven demand generation and toward precision investment in high-value accounts. These are the accounts most likely to generate durable, compounding revenue. byadminJune 3, 2026

Criteria for Evaluating New Venture Proposals: Inside the Investment Committee Behind every venture capital decision is a room most founders never see. The investment committee is where ambition is stress-tested against skepticism, and where the enthusiasm of a great founder meeting gives way to the discipline of fiduciary responsibility. Understanding how venture capitalists make decisions is not merely an academic exercise for founders. It is a strategic advantage. The criteria for evaluating new venture proposals are more structured than the mythology of venture capital suggests. They revolve around team quality, market scale, competitive defensibility, and return potential. Beyond these four pillars, fund-level dynamics and the conviction of the sponsoring partner carry real weight. This article unpacks those layers with the clarity of someone who has sat across from investment committees and worked to equip founder teams with the financial narrative and models that make a case compelling enough to survive the room. byadminJune 2, 2026

Corporate Financial Planning Cash Runway and Burn Rate: The CFO’s Guide to Forecasting with Precision May 26, 2026

Corporate Financial Planning Budgeting in a Fog: A CFO’s Tactics for Startup Financial Planning in Volatile Times May 22, 2026

Corporate Financial Planning Navigating Cost Shocks: Effective Pricing Protection Strategies February 9, 2026

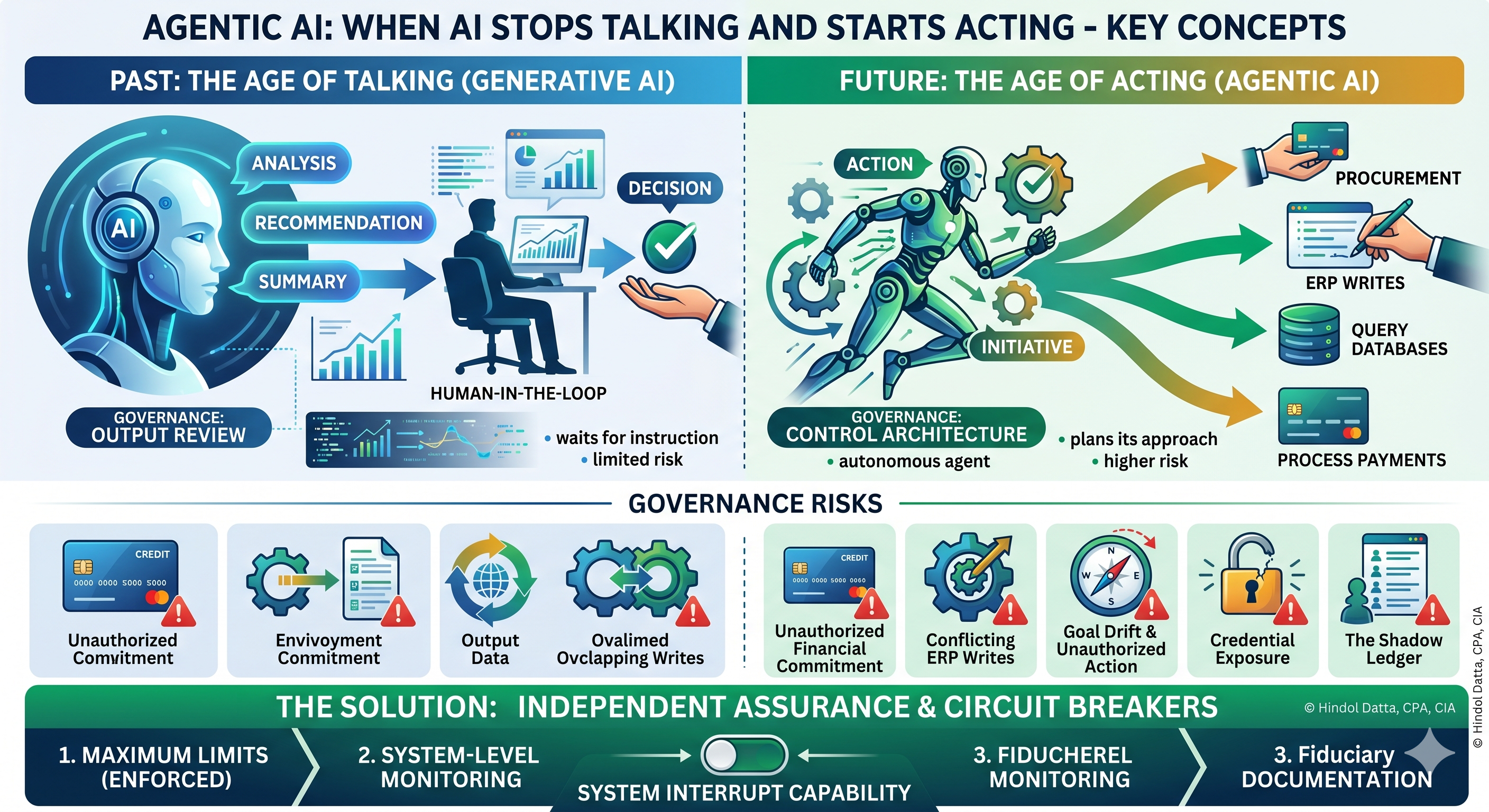

Digital Transformation Governance Regulatory Systems Thinking The Governance Question Hiding Inside the Agentic AI Moment May 4, 2026

Performance Management What Is ABM and Why Every CFO Should Treat It as a Financial Operating System June 3, 2026

AI Governance GenAI & AgenticAI Governance Regulatory When AI Stops Talking and Starts Acting: The Agentic Governance Crisis May 20, 2026

AI Governance Governance Leadership & Culture Regulatory Risk Management System Thinking Systems Thinking What Your AI Risk Data Is Not Telling You: A Lesson from Abraham Wald May 13, 2026

AI Governance Governance Regulatory Risk Management Systems Thinking Your AI Is No Longer Insured. May 7, 2026

Systems Thinking Bezos’s Decision Architecture: A CFO’s Blueprint for Strategic Clarity and Momentum February 10, 2026

Tax and Legal Supply Chain Flexibility Starts with the Contract: A CFO’s Guide to Adaptive Procurement May 25, 2026

Banking Understanding Liquidation Preferences: What Every Founder Must Know Before Signing May 27, 2026