Executive Summary

Behind every venture capital decision is a room most founders never see. The investment committee is where ambition is stress-tested against skepticism, and where the enthusiasm of a great founder meeting gives way to the discipline of fiduciary responsibility. Understanding how venture capitalists make decisions is not merely an academic exercise for founders. It is a strategic advantage. The criteria for evaluating new venture proposals are more structured than the mythology of venture capital suggests. They revolve around team quality, market scale, competitive defensibility, and return potential. Beyond these four pillars, fund-level dynamics and the conviction of the sponsoring partner carry real weight. This article unpacks those layers with the clarity of someone who has sat across from investment committees and worked to equip founder teams with the financial narrative and models that make a case compelling enough to survive the room.

What Actually Happens After the Pitch

For founders, the post-pitch silence is often the most disorienting part of the fundraising process. The investor says, “Let me take this to my partnership,” and then the waiting begins. What follows inside that room is far less mystical than it appears from the outside.

Investment committees are not impressed by momentum alone. They are rigorous, unsentimental, and shaped by frameworks developed over hundreds of deals. The best venture firms run pattern-driven decision processes. They have seen enough companies at enough stages to know which signals matter and which ones are noise.

Having structured VC-grade financial models, cohort analyses, and multi-year operating plans for high-growth companies across SaaS, cybersecurity, and mission-driven nonprofit organizations, I have seen firsthand which elements of a founder’s case land and which ones quietly dissolve under scrutiny. The criteria for evaluating new venture proposals tend to follow a consistent architecture, regardless of firm or stage.

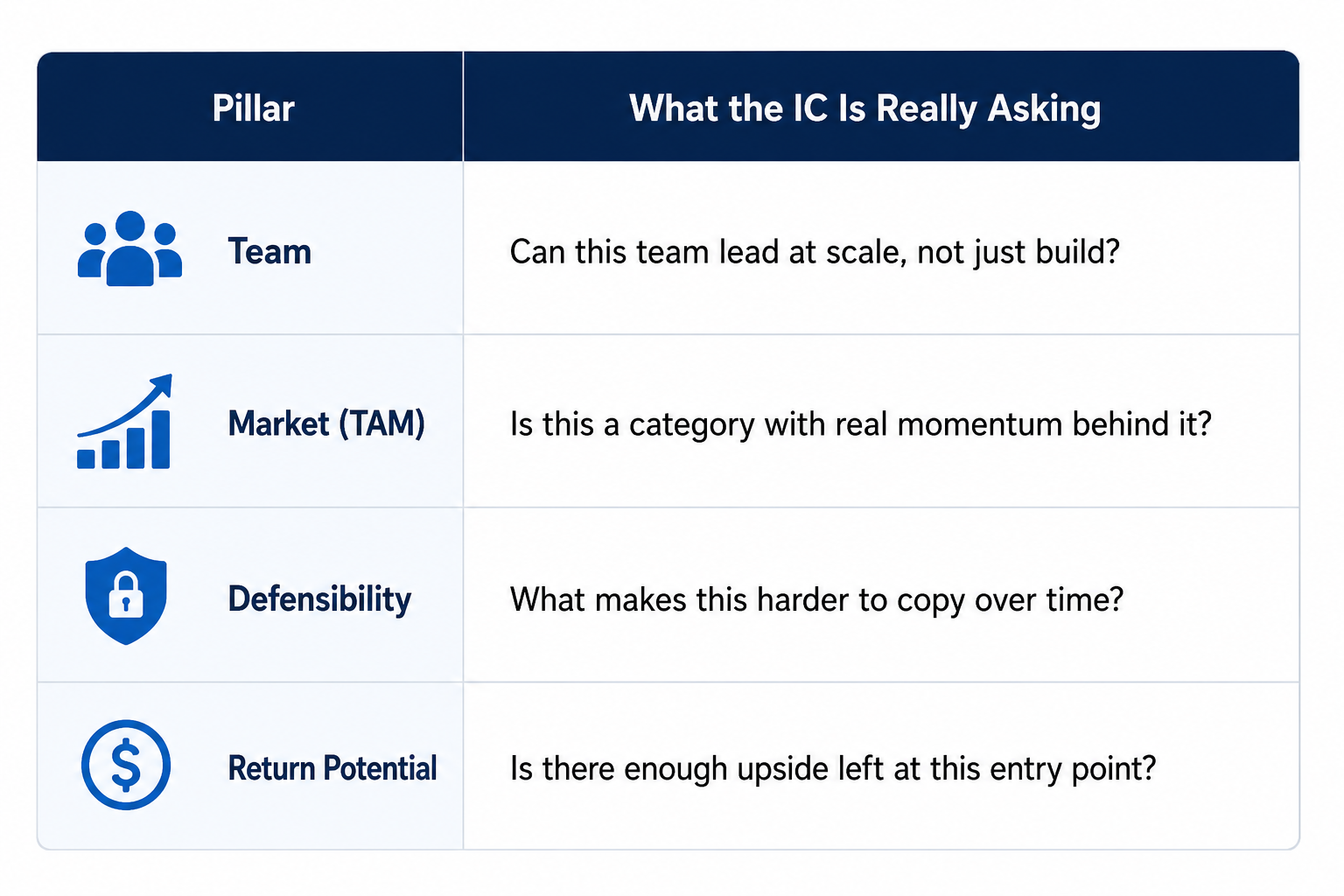

The Four Core Evaluation Pillars

Team Risk: Leadership Under Pressure

The first line of inquiry in nearly every investment committee discussion is not about the product. It is about the people. Even the most compelling market opportunity can be undone by leadership that cannot scale with the business.

The committee is asking a specific set of questions:

- Does this founder know what they do not yet know?

- Are they attracting strong early hires, or is the team thin?

- How did they respond when challenged in the partner meeting?

- Have they demonstrated resilience when the path became unclear?

These are not questions about credentials. They are observations about behavior. A founder with a sophisticated understanding of their own gaps, who has built a capable team around those gaps, signals maturity that investors prize above almost everything else.

Market Size: TAM as a Story, Not Just a Number

Once the team clears scrutiny, the conversation moves to the market. Total addressable market is a concept every founder knows and every investor interrogates differently. The number matters, but the narrative behind it matters more.

Venture capitalists make decisions based on whether a company can reach meaningful revenue scale within the fund’s return window. But they are also asking whether the market itself is moving. A large static market is less interesting than a medium market with strong tailwinds.

- Is the category expanding?

- Is there a behavioral or regulatory shift accelerating adoption?

- Is this the kind of market where a clear winner is likely to emerge?

Having led finance functions in fast-growing sectors including logistics, digital marketing, and cybersecurity, I have seen how a well-constructed market narrative, supported by credible unit economics and bottoms-up modeling, elevates the quality of the investor conversation. It moves the discussion from a debate about assumptions to a shared exploration of potential.

Defensibility: The Moat Question

Abundant capital means fast followers. The investment committee will press hard on what sustainable advantage this company is actually building. Technology alone is rarely enough. The more compelling answers involve compounding advantages.

Network effects, proprietary data, switching costs, regulatory positioning, and deep integration into customer workflows are the kinds of moats that hold. The best founders speak not just about what they are building today but about why the business becomes more defensible as it scales. Investors listen closely for this quality of thinking. It reveals whether the founder is operating tactically or architecting something that compounds over time.

Return Potential: How Much Juice Remains

The fourth pillar is the most financially explicit. Venture returns are driven by outliers. A structurally sound company priced to perfection at entry leaves little room for the multiple expansion that makes a fund-returning investment possible.

The IC will ask directly or indirectly: at this valuation, with this stage of development and this level of prior capital raised, is there a credible path to five times, ten times, or more? If the round is heavily allocated or the entry price reflects optimism that has already been priced in, the committee’s enthusiasm will cool regardless of how strong the underlying business is.

Beyond the Four Pillars: Fund Dynamics and Partner Conviction

The four pillars are necessary but not sufficient. Two additional dimensions shape nearly every investment committee outcome.

The first is fund-level portfolio logic. How much capital remains available for deployment? How concentrated is the existing portfolio in this sector or stage? Will this investment require significant reserves for follow-on rounds? These are structural questions about portfolio construction that have nothing to do with the quality of the company and everything to do with the state of the fund.

The second is partner conviction. When a partner presents a deal with genuine, personal belief in the founder and the opportunity, it registers. Investment committees operate on pattern recognition, but they also honor the professional judgment of a trusted colleague who has done the work. That belief, if credible and well-supported, can carry a deal across the line when the data alone leaves the room uncertain.

What Founders Can Do With This Knowledge

Understanding how venture capitalists make decisions transforms the way a founder prepares. The pitch is not the end of the process. It is the beginning of a relay. The partner who attended the meeting will carry the founder’s story into a room the founder will never enter. Equipping that partner to tell the story effectively is one of the highest-leverage activities a founder can engage in.

This means anticipating the committee’s questions before they are asked. It means building financial models that are transparent, defensible, and structured around the metrics investors use internally. It means being able to speak clearly to team composition, market momentum, competitive positioning, and return architecture in plain language that survives translation.

Why do investors sometimes go quiet after what felt like a strong pitch?

Silence after a promising meeting is almost never personal. It reflects the internal dynamics of the investment committee process. A partner may be navigating internal disagreement, resolving fund-level portfolio questions, or completing reference checks and diligence before bringing a deal forward formally. Founders who understand this are better positioned to stay constructively engaged rather than interpreting silence as rejection. A well-timed, brief follow-up that provides additional data or answers anticipated committee questions demonstrates operational clarity and keeps the momentum of the conversation alive.

Conclusion

The investment committee is where the criteria for evaluating new venture proposals are applied with rigor and without sentiment. It is where the quality of a founder’s preparation, the coherence of the financial narrative, and the strength of the sponsoring partner’s conviction are all weighed together. For founders, demystifying this process is not just useful. It is strategic. The firms that fund great companies are not making blind bets on charisma. They are running structured analyses against a consistent framework. Founders who understand that framework, who build their case with the committee’s questions already answered, enter the fundraising process with a meaningful advantage. The capital deployed from those rooms shapes industries. Understanding how it moves is foundational knowledge for anyone operating at the intersection of venture and enterprise.

Disclaimer: This blog is intended for informational purposes only and does not constitute legal, tax, or accounting advice. You should consult your own tax advisor or counsel for advice tailored to your specific situation.

Hindol Datta is a seasoned finance executive with over 25 years of leadership experience across SaaS, cybersecurity, logistics, and digital marketing industries. He has served as CFO and VP of Finance in both public and private companies, leading $120M+ in fundraising and $150M+ in M&A transactions while driving predictive analytics and ERP transformations. Known for blending strategic foresight with operational discipline, he builds high-performing global finance organizations that enable scalable growth and data-driven decision-making.

AI-assisted insights, supplemented by 25 years of finance leadership experience.