Executive Summary

Understanding liquidation preferences is one of the most consequential disciplines a founder can develop, yet these provisions routinely receive far less attention than valuation multiples or ownership percentages. For founders, this oversight can translate into a dramatically smaller economic outcome than the cap table suggests. This article examines how these provisions function, how they interact across multiple funding rounds, and how senior executives can use exit waterfall modeling to negotiate with clarity and confidence. Drawing on over twenty-five years of capital strategy experience across SaaS, gaming, logistics, cybersecurity, and nonprofit sectors, including participation in capital raises exceeding one hundred and twenty million dollars and M&A transactions exceeding one hundred and fifty million dollars, the analysis below equips founders and their advisors to read term sheets with the precision these instruments demand.

The Gap Between Ownership and Economic Outcome

A cap table shows shares. A waterfall shows dollars. These two documents tell very different stories, and the distance between them is often defined by liquidation preferences. When a founder retains seventy-five percent of a company, the instinct is to expect seventy-five percent of the exit proceeds. That assumption holds only when the capitalization structure is clean. When preferred stock carries liquidation preferences and participation rights, the economic reality diverges from the legal ownership, sometimes sharply.

Understanding liquidation preferences is not a legal formality. It is a strategic discipline. Every CFO who has sat at an exit negotiation table understands that the terms signed at Series A can reappear with enormous force at the closing of a sale three or five years later.

How Liquidation Preferences Work

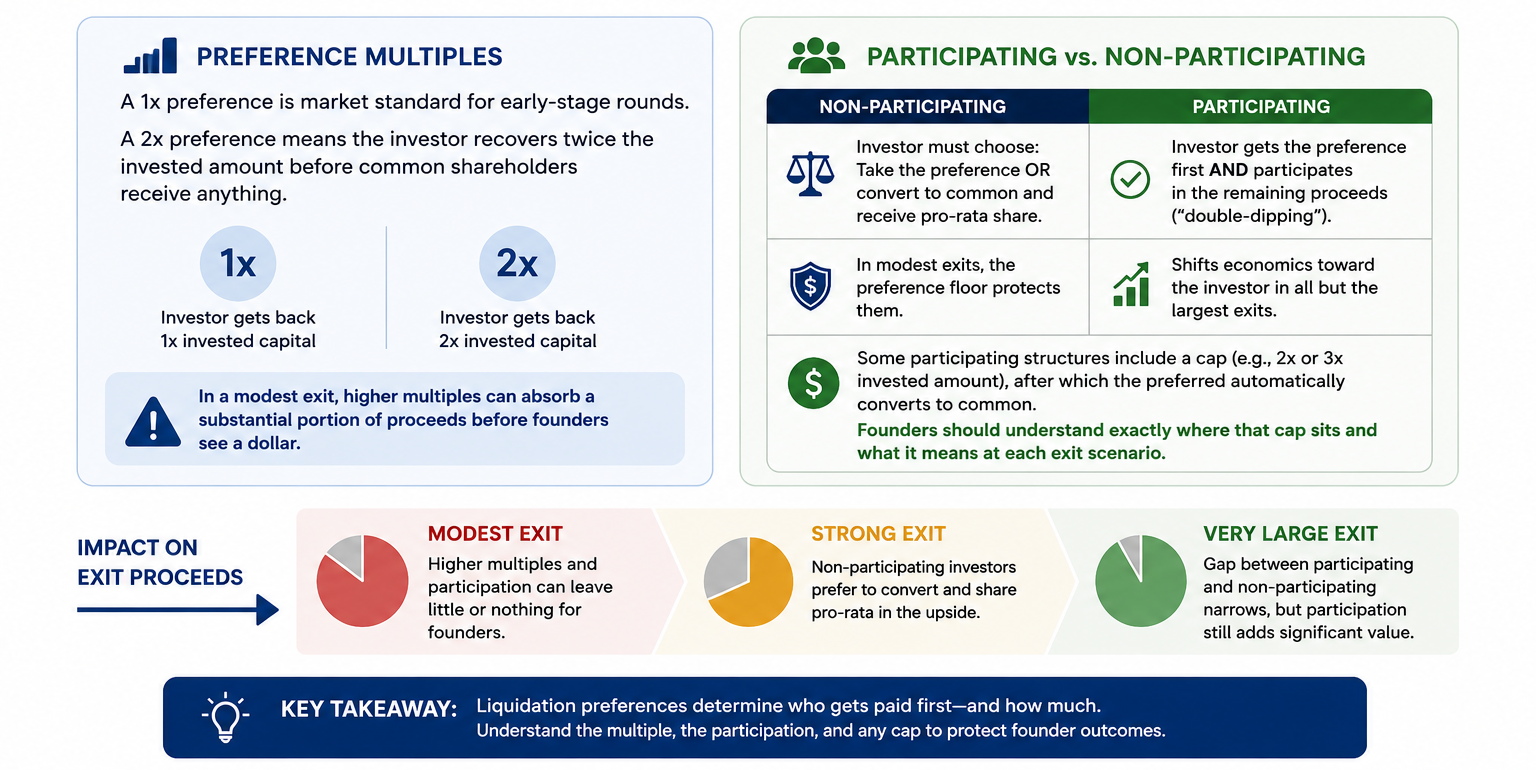

A liquidation preference gives preferred shareholders the right to recover their invested capital before any proceeds are distributed to common stockholders. The standard form is a 1x non-participating preference, meaning the investor receives back the amount invested, and then converts to common stock to participate in any remaining upside proportionally.

The structure becomes more complex in two dimensions: the preference multiple and the participation feature.

Preference Multiples

A 1x preference is considered market standard for early-stage rounds. A 2x preference means the investor recovers twice the invested amount before common shareholders receive anything. In a modest exit, this can absorb a substantial portion of proceeds before founders see a dollar.

Participating Versus Non-Participating Preferred

This is the clause that founders most frequently underestimate. Non-participating preferred shareholders must choose: take the liquidation preference or convert to common stock and receive a pro-rata share of proceeds. In a strong exit, conversion is preferable. In a modest one, the preference floor protects them.

Participating preferred shareholders do not have to choose. They receive their preference first and then participate alongside common shareholders in the remaining proceeds. This is the mechanism sometimes described as double-dipping, and it materially shifts economics toward the investor in all but the largest exits.

Some participating structures include a cap, such as two or three times the original investment, at which point the preferred automatically converts to common. Founders should understand exactly where that cap sits and what it means at each exit scenario.

The Compounding Effect Across Multiple Rounds

The challenge intensifies as companies raise successive rounds. Each new investor typically negotiates for senior preference status, meaning their preference is paid before prior investors. The result is a stacked waterfall in which founders and early employees may find themselves at the bottom of a deep structure.

Consider a company that raises a seed round, a Series A, and a Series B. If the Series B carries senior participating preferred stock, and the Series A and seed carry subordinate non-participating preferred, the distribution sequence in any exit below a certain threshold heavily favors the latest investor. The founders’ economic outcome in a sixty or seventy million dollar sale can be meaningfully below what their percentage ownership would suggest.

This is not a theoretical concern. In my work leading capital transactions across SaaS companies, a gaming enterprise that executed over one hundred million dollars in acquisitions, and a mission-driven education institution where I secured a forty-eight million dollar capital raise, the exit waterfall analysis consistently revealed outcomes that surprised founders who had not modeled the scenarios in advance.

Modeling the Waterfall: A Framework for Clarity

The most effective tool for understanding these terms is a structured exit waterfall model. This is a straightforward analytical exercise that every founding team and their CFO should complete before signing any term sheet and revisit before any subsequent round.

The model maps exit proceeds across a range of outcomes and shows the distribution to each stakeholder class at each level. A well-constructed waterfall makes the implications of preferences and participation visible and comparable.

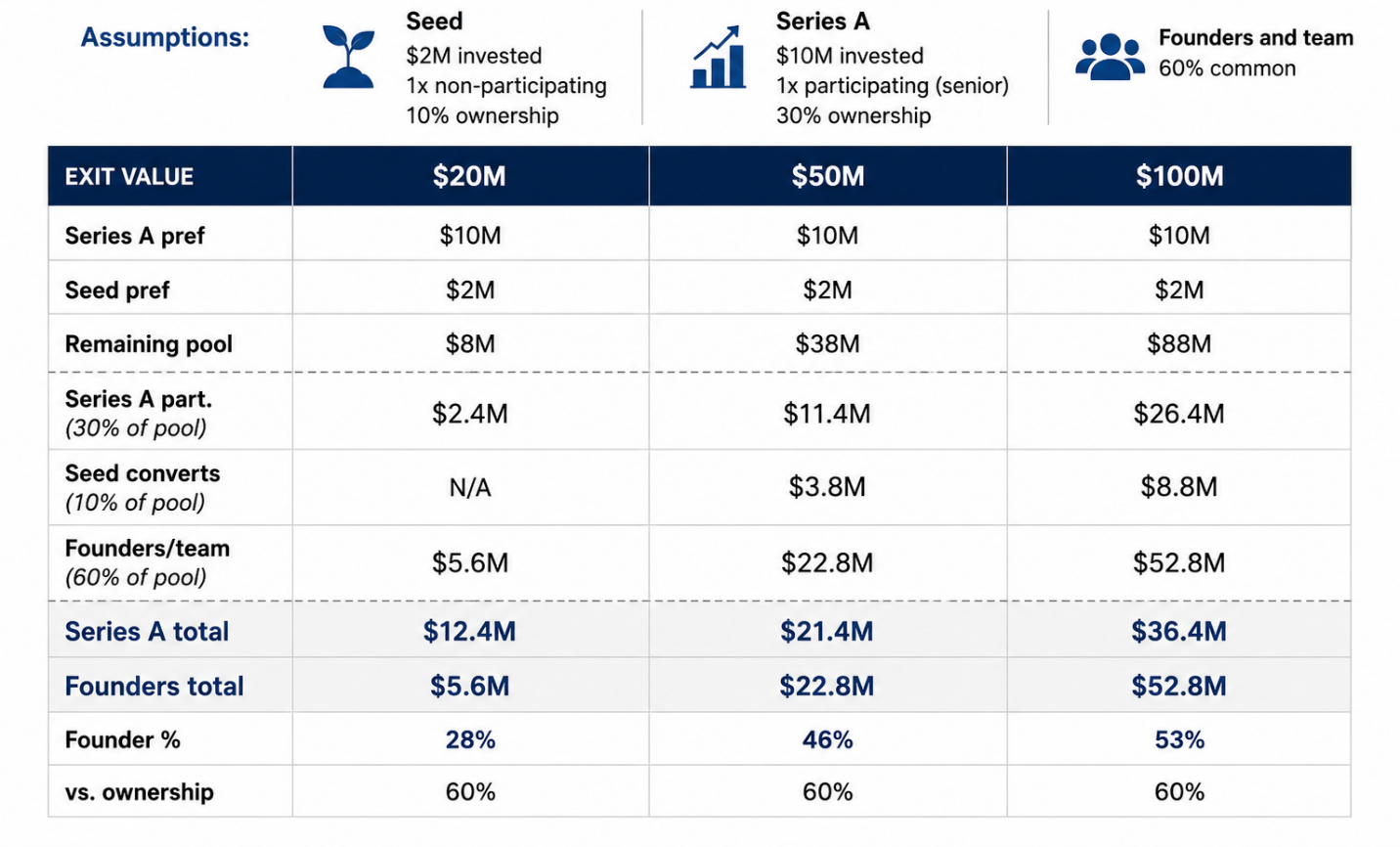

The following table illustrates how proceeds distribute in a simplified two-investor scenario with participating and non-participating preferred across three exit values.

The table illustrates a central truth: at modest exit values, the founder’s economic share diverges significantly from their legal ownership. Only at larger outcomes does the gap begin to close.

Founders should run this model across at minimum three scenarios: a downside case, a base case, and an optimistic case. Each scenario reveals where the leverage sits and which terms matter most.

Negotiating With Awareness

Armed with waterfall modeling, founders can engage in more informed term sheet negotiations. Several principles are worth internalizing.

Clean terms often outperform high valuations. A lower valuation with a 1x non-participating preference may produce a better economic outcome for founders than a higher valuation with participating preferred and stacked seniority. The headline number is not the whole story.

Founders may also consider negotiating:

- Conversion triggers that remove participation rights above a defined exit threshold

- Sunset provisions that convert preferred to common after a specified period without a liquidity event

- Pari passu treatment across rounds rather than stacked seniority

None of these requests is unreasonable. Investors who understand founder motivation and long-term alignment are generally open to structures that preserve incentives without sacrificing their downside protection.

Communication and Governance

Transparency about the cap table and waterfall structure serves the entire organization. Employees holding options deserve to understand what their stake means in realistic exit scenarios, not just in aspirational ones. Leaders who communicate this clearly build more grounded and committed teams.

Boards play a meaningful role in maintaining this balance. A well-functioning board recognizes that punitive capital structures demotivate the operators who are responsible for generating the value in the first place. This is a governance principle as much as a financial one, and it applies across every sector, from early-stage SaaS to established logistics enterprises.

Conclusion

Liquidation preferences and participation rights are not fine print. They are foundational economic architecture. A founder who understands them can negotiate from a position of clarity. One who does not may discover their implications only when it is too late to change them. The modeling is not complex. The discipline required to insist on it is what separates founders who lead their financings from those who are led by them. Over a career spanning capital raises, M&A transactions, and finance transformations across multiple sectors, the consistent differentiator has been awareness. Founders who modeled their waterfalls asked better questions, negotiated better terms, and ultimately retained more of the value they worked to create. That awareness begins with understanding the terms before the ink dries.

Disclaimer: This blog is intended for informational purposes only and does not constitute legal, tax, or accounting advice. You should consult your own tax advisor or counsel for advice tailored to your specific situation.

Hindol Datta is a seasoned finance executive with over 25 years of leadership experience across SaaS, cybersecurity, logistics, and digital marketing industries. He has served as CFO and VP of Finance in both public and private companies, leading $120M+ in fundraising and $150M+ in M&A transactions while driving predictive analytics and ERP transformations. Known for blending strategic foresight with operational discipline, he builds high-performing global finance organizations that enable scalable growth and data-driven decision-making.

AI-assisted insights, supplemented by 25 years of finance leadership experience.