Executive Summary

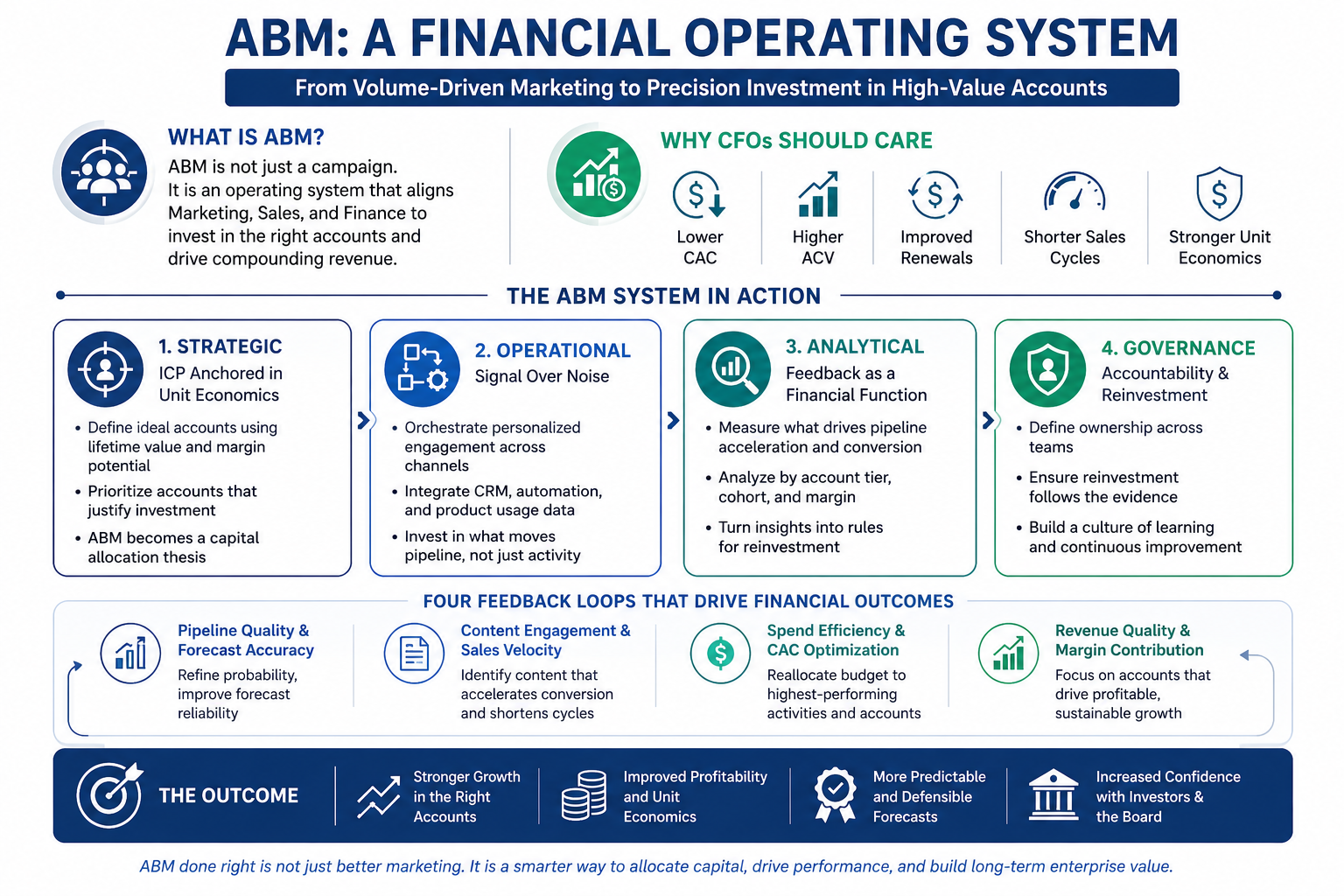

Account-Based Marketing, or ABM, is widely understood as a targeted marketing approach. It is less widely understood as a capital allocation decision. For CFOs and senior finance executives, that distinction carries real strategic weight. ABM is a focused growth strategy. It moves companies away from volume-driven demand generation and toward precision investment in high-value accounts. These are the accounts most likely to generate durable, compounding revenue.

When aligned to financial objectives, ABM shapes how marketing spends and how Finance forecasts. It also determines how Sales is incentivized and how the business learns. This article examines ABM through the lens of a finance executive with over twenty-five years of operating experience. That experience spans cybersecurity, SaaS, logistics, digital marketing, and nonprofit sectors. It covers four dimensions: the architecture of a mature ABM system, the feedback loops that drive precision, the structural conditions that enable scale, and the strategic role ABM plays in capital market conversations.

ABM Is Not a Campaign. It Is an Operating System

The conventional definition of ABM frames it as a marketing strategy that concentrates resources on a curated set of target accounts, treating each as a market of one. That framing is accurate but incomplete. The more revealing view is that ABM is an operating system that converts fragmented go-to-market activity into aligned investment. This framing unlocks its full value for Finance.

Traditional demand generation optimizes for volume. ABM optimizes for fit. That shift has immediate financial implications. When marketing targets the right accounts with precision, customer acquisition cost becomes a function of specificity rather than scale. Sales cycles compress. Average contract values rise. Renewal rates improve. These are not marketing metrics. They are unit economics.

The question every CFO should ask is not “What is ABM?” but rather “Where in our operating model should ABM sit?” In mature organizations, the answer is everywhere. It touches campaign design, account tiering, content investment, tool procurement, forecast methodology, and incentive structure. ABM is only as valuable as the cross-functional architecture that supports it.

Having built finance functions across sectors where go-to-market precision is a competitive necessity, including cybersecurity, enterprise SaaS, and digital marketing, I have seen how organizations that treat ABM as a marketing initiative extract modest gains. Organizations that treat it as a financial operating system extract compounding ones.

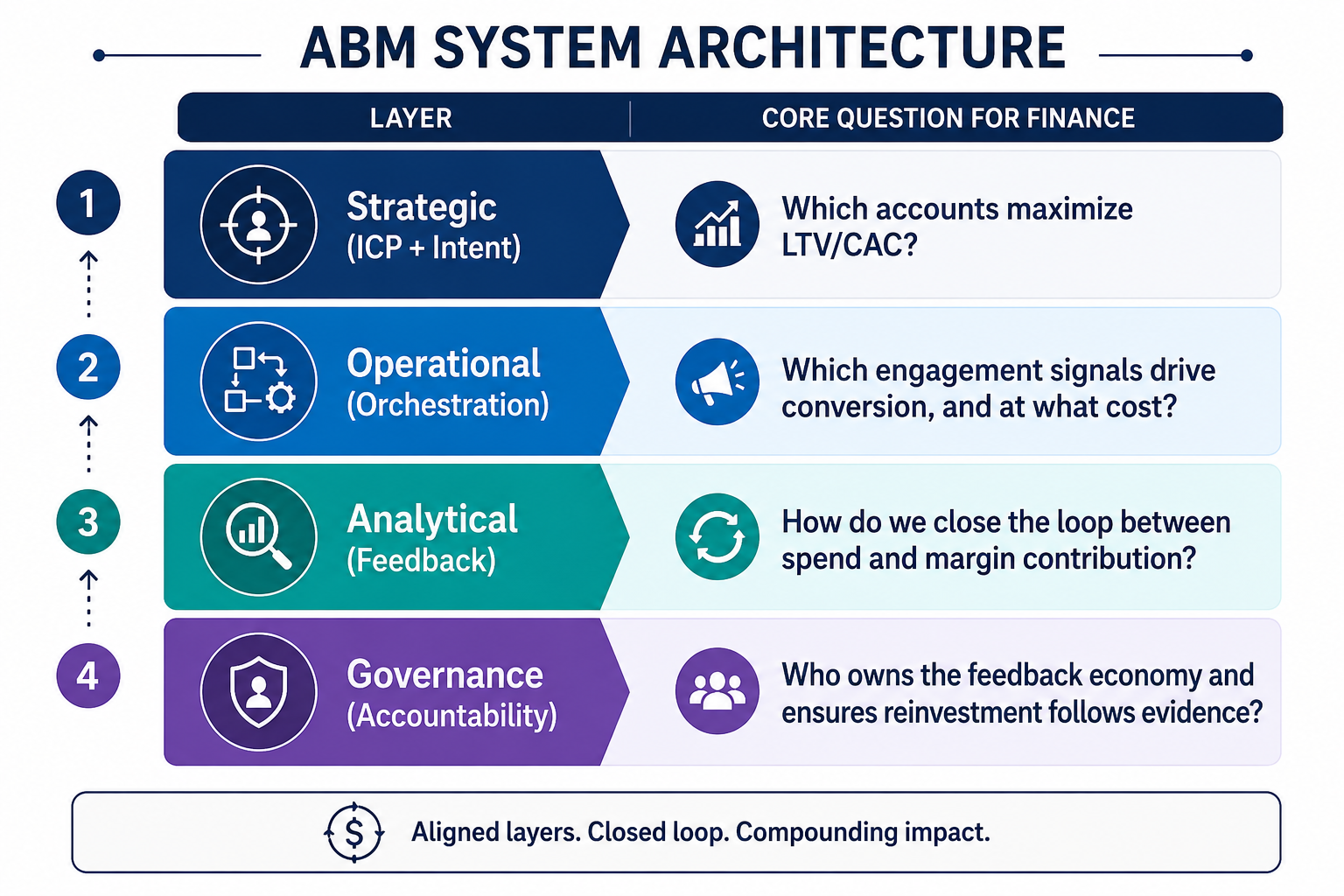

The Architecture of a Sound ABM System

The Strategic Layer: ICP Defined by Unit Economics

Every ABM program begins with the Ideal Customer Profile. Most organizations define it through Sales intuition or marketing segmentation. The CFO’s contribution is to anchor ICP selection in financial reality: what is the lifetime value of this account cohort? What is the cost of delaying conversion by one quarter? Which verticals deliver the strongest margin on renewal?

When Finance injects this discipline into ICP design, ABM stops being a list of desirable logos and becomes a capital allocation thesis. The accounts that receive disproportionate attention are those that justify it economically, not just commercially.

The Operational Layer: Signal Over Noise

Below strategy lies orchestration. Marketing and Sales execute personalized engagement journeys across content, outreach, events, and digital touchpoints. The CFO’s role at this layer is to ask which touches move the needle and which ones simply move the budget.

By integrating CRM data, marketing automation outputs, and product usage telemetry, finance can shift the conversation from storytelling to attribution. The goal is not to measure every activity but to identify the activities that correlate with accelerated pipeline movement and act as triggers for reinvestment.

The Analytical Layer: Feedback as a Financial Function

At the base of the architecture sits analytics, but not the kind that tallies impressions and click-through rates. The analytical layer that matters to Finance examines pipeline acceleration by account tier, conversion rates by campaign cohort, and the margin profiles of closed accounts. This is where ABM earns its credibility as a business system rather than a marketing program.

Four Feedback Loops That Connect ABM to Financial Outcomes

The most successful ABM programs do not thrive because of creative execution alone. They thrive because the system learns. Building that learning into the organization requires four interlocking feedback loops, each anchored to a core financial objective.

Pipeline Quality and Forecast Accuracy

ABM’s narrow account focus gives Finance a high-resolution lens on forecast quality. Rather than evaluate pipeline by volume of leads, a mature ABM model examines how far, how fast, and how fit accounts are relative to forecast expectations.

In one implementation across a high-growth SaaS organization, feeding loss-reason analytics back into campaign design and sales enablement improved forecast accuracy by eighteen percent within a few quarters. That improvement did not come from better CRM hygiene alone. It came from continuously refining the probability space that ABM’s focused scope makes visible.

Content Engagement and Sales Velocity

Marketing has always been able to measure engagement. What matters to Finance is whether engagement accelerates conversion. By measuring time from content interaction to opportunity creation, segmented by account tier and industry, organizations can identify which assets genuinely compress the sales cycle and which ones generate activity without commercial momentum.

In one example, a single customer success narrative reduced average time-to-opportunity by twenty-seven percent for Tier 1 accounts in one vertical while showing no measurable effect in another. That insight changed both campaign spend and Sales prioritization. Finance adjusted weighted pipeline forecasts accordingly. Content became a capital allocation decision.

Product Usage and Renewal Probability

ABM is not only an acquisition framework. When ABM segmentation logic is layered with post-sale product telemetry, it becomes a retention instrument. Accounts that engaged deeply in pre-sale ABM campaigns but showed delayed feature activation after closing carried a significantly higher churn probability.

By surfacing this behavioral divergence early, one organization reduced mid-tier churn by nearly fifteen percent. From the CFO’s perspective, that translated directly into lower revenue leakage, more accurate LTV modeling, and stronger renewal forecasting. The feedback loop between pre-sale engagement and post-sale behavior is one of the highest-value connections a finance-led ABM system can build.

Campaign ROI and Budget Reallocation

The final loop is the most direct: connecting campaign investment to margin contribution. This requires calculating fully loaded customer acquisition cost by ABM tier and vertical, including content production, sales development time, technology spend, and follow-up effort, and then overlaying margin contribution from closed accounts.

In one cycle, Tier 2 accounts in a specific vertical delivered the highest campaign ROI despite lower initial contract values, because their sales cycles were shorter, conversion rates were higher, and churn was lower. That finding led to reallocating twenty-two percent of ABM spend toward that segment. Without the feedback loop, the budget would have followed the larger logo, not the better economics.

Scaling ABM: Structure, Incentives, and Governance

The early stages of ABM often feel artisanal. A small team handpicks accounts, builds custom cadences, and stitches together results manually. When the first deals close with elevated contract values and shorter cycles, the model feels like a breakthrough. The challenge arrives at scale.

Role Clarity and Pod Structure

The first principle of scalable ABM is role clarity. Without it, ABM becomes everyone’s responsibility and no one’s accountability. Durable ABM programs create dedicated cross-functional pods, each owning a defined cohort of accounts, operating with shared revenue targets, and maintaining direct visibility into the financial performance of their accounts.

In one enterprise deployment targeting financial services accounts, a dedicated pod using Finance-validated account scoring models, Marketing-created personalized content, and Sales-orchestrated engagement produced a forty percent lift in deal velocity compared to the general account pool within two quarters. The tactics mattered. But the structure made the tactics sustainable.

Incentive Alignment Across Functions

No structure overcomes misaligned incentives. If Marketing is rewarded for impressions while Sales is measured on close rates and Finance tracks CAC in isolation, ABM will generate internal friction faster than external pipeline.

Shared incentive scorecards that combine departmental metrics with collective KPIs, including opportunity creation by ABM tier, sales cycle compression, and net dollar retention, create the conditions for genuine cross-functional ownership. When a segment shows strong engagement but weak conversion, shared accountability surfaces the diagnosis faster and removes the instinct to assign blame.

The CFO’s mandate is to ensure that incentive design reflects economic cause and effect. Marketing efforts that lift Sales productivity should share in the yield. RevOps improvements that accelerate time to cash should be measured on margin velocity, not just systems performance.

Governance Without Bureaucracy

Scaling ABM requires governance, not bureaucracy. A monthly cross-functional council that reviews pipeline velocity, message alignment, CAC curves, and renewal forecasts by ABM cluster, with Finance providing analytical backbone, creates the rhythm of continuous refinement without the weight of committee overhead.

The goal is to ensure that capital flows follow evidence, that experiments are bounded by expected return, and that learnings compound across quarters rather than disappear into retrospective decks that no one revisits.

ABM as a Strategic Planning and Capital Markets Asset

The longest-term payoff from ABM maturity is not operational efficiency. It is strategic foresight. When ABM behavior is modeled over multiple quarters, it produces a rolling yield curve that forecasts future bookings with lower variance than stage-based pipeline models alone. Account movement from awareness through closed-won to renewal becomes a planning instrument, informing headcount decisions, regional expansion, and working capital requirements.

This shift, from static pipeline targets to dynamic investment corridors based on account conversion patterns, repositions Finance from rear-view reporting to forward-leaning decision design.

ABM data also shapes the capital markets narrative. Investors increasingly ask whether a company can scale its go-to-market motion without linear increases in operating expenditure. ABM provides the cohort economics to answer that question with specificity: retention by segment, expansion by vertical, acquisition cost by campaign vintage.

In one investor presentation, ABM-derived data demonstrated that a particular enterprise segment, though slower to convert, delivered a sixty percent higher lifetime value over twenty-four months with substantially lower support costs. That slide was not a marketing achievement. It was a capital story, and it defined the CFO’s contribution to the growth narrative in a way that spreadsheet-only analysis could not.

How should a CFO begin integrating ABM into financial planning and forecasting?

The most effective starting point is to attach financial accountability to existing ABM activity rather than redesign the program from scratch. Begin by calculating fully loaded customer acquisition cost and lifetime value by account tier and industry vertical. Identify which segments are generating the strongest margin contribution relative to cost of pursuit. Then embed those findings into forecast models as probability-weighted inputs tied to account engagement intensity. This creates an immediate feedback loop between Marketing activity and Finance output, and it builds the organizational muscle for treating ABM as a planning instrument rather than a campaign budget line.

Conclusion

What is ABM, at its most expansive? It is a focused growth strategy that gives Finance the connective tissue to align product ambition, customer behavior, and capital deployment into a single coherent system. Its value is not realized through targeting sophistication or creative excellence alone. It is realized when feedback loops are built, incentives are aligned, governance is rhythmic, and learning compounds across cycles. For CFOs who have spent careers translating between commercial ambition and financial discipline, ABM offers a rare instrument: a go-to-market framework that speaks naturally in the language of returns. Organizations that treat it as a marketing tactic will extract incremental gains. Those that treat it as a financial operating system will build a durable advantage, one that improves with every campaign, every renewal, and every quarter of disciplined observation.

Disclaimer: This blog is intended for informational purposes only and does not constitute legal, tax, or accounting advice. You should consult your own tax advisor or counsel for advice tailored to your specific situation.

Hindol Datta is a seasoned finance executive with over 25 years of leadership experience across SaaS, cybersecurity, logistics, and digital marketing industries. He has served as CFO and VP of Finance in both public and private companies, leading $120M+ in fundraising and $150M+ in M&A transactions while driving predictive analytics and ERP transformations. Known for blending strategic foresight with operational discipline, he builds high-performing global finance organizations that enable scalable growth and data-driven decision-making.

AI-assisted insights, supplemented by 25 years of finance leadership experience.