Executive Summary

For decades, lease obligations lived in the footnotes of financial statements, quietly understating corporate leverage and obscuring economic reality. Lease accounting under ASC 842 changed that. Issued by the Financial Accounting Standards Board, the standard requires companies to recognize a right-of-use asset and a corresponding lease liability for virtually all leases with terms exceeding twelve months. The implications extend well beyond journal entries. They affect leverage ratios, covenant structures, return metrics, and the financial narrative presented to boards and investors. For CFOs navigating capital-intensive or multi-jurisdiction operating models, ASC 842 demands not only technical compliance but strategic interpretation. This article examines what the standard requires, how its classification framework operates, where implementation risk concentrates, and why finance leaders who engage with it rigorously will find it a genuine instrument of capital clarity rather than a compliance burden.

Why Lease Accounting Needed a Structural Reset

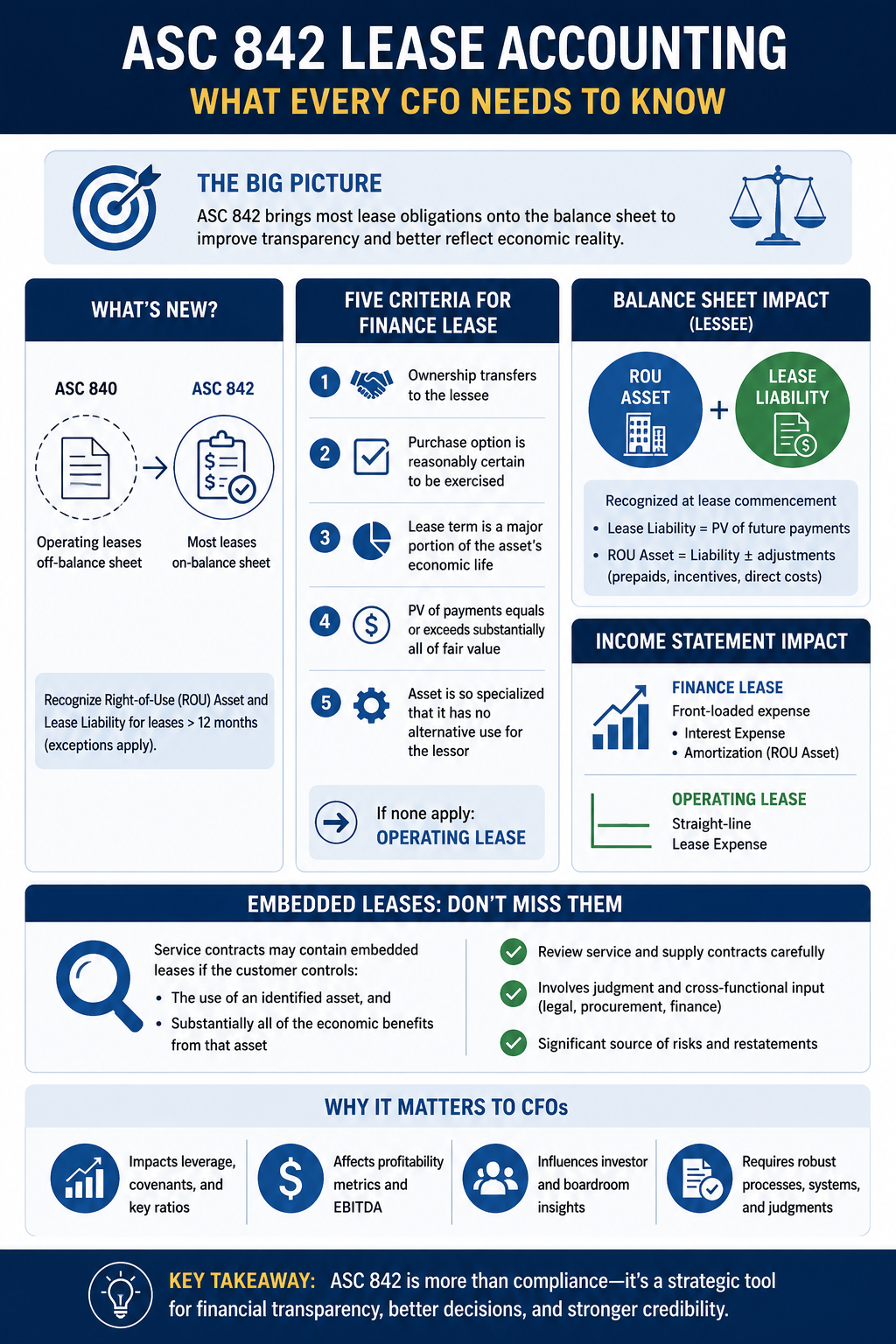

Under the prior standard, ASC 840, only capital leases appeared on the balance sheet. Operating leases, regardless of their scale or duration, were recorded simply as straight-line rent expense on the income statement. A retailer with hundreds of long-term storefronts, a logistics company with dedicated fleet contracts, or a cloud infrastructure firm with data center commitments could all present a comparatively clean balance sheet while carrying obligations that carried the full economic weight of debt. Analysts attempted to compensate using multipliers and discounted cash flow approximations, but the inconsistency was structural and persistent.

ASC 842 closed that gap. Under the new framework, lessees must recognize a right-of-use asset and a corresponding lease liability for all leases with terms longer than twelve months, covering both finance leases and operating leases. The change brought trillions of dollars of previously invisible obligations onto corporate balance sheets across industries ranging from aviation to enterprise software. The shift was not merely cosmetic. It was a fundamental recalibration of how financial statements reflect the cost of controlling and using resources a company does not own.

Having led finance functions across logistics, cybersecurity, SaaS, and digital marketing, I have seen firsthand how this recalibration changes the conversation at every level of the organization, from treasury and legal to the boardroom. Lease accounting is no longer a back-office function. Under ASC 842, it is a strategic discipline.

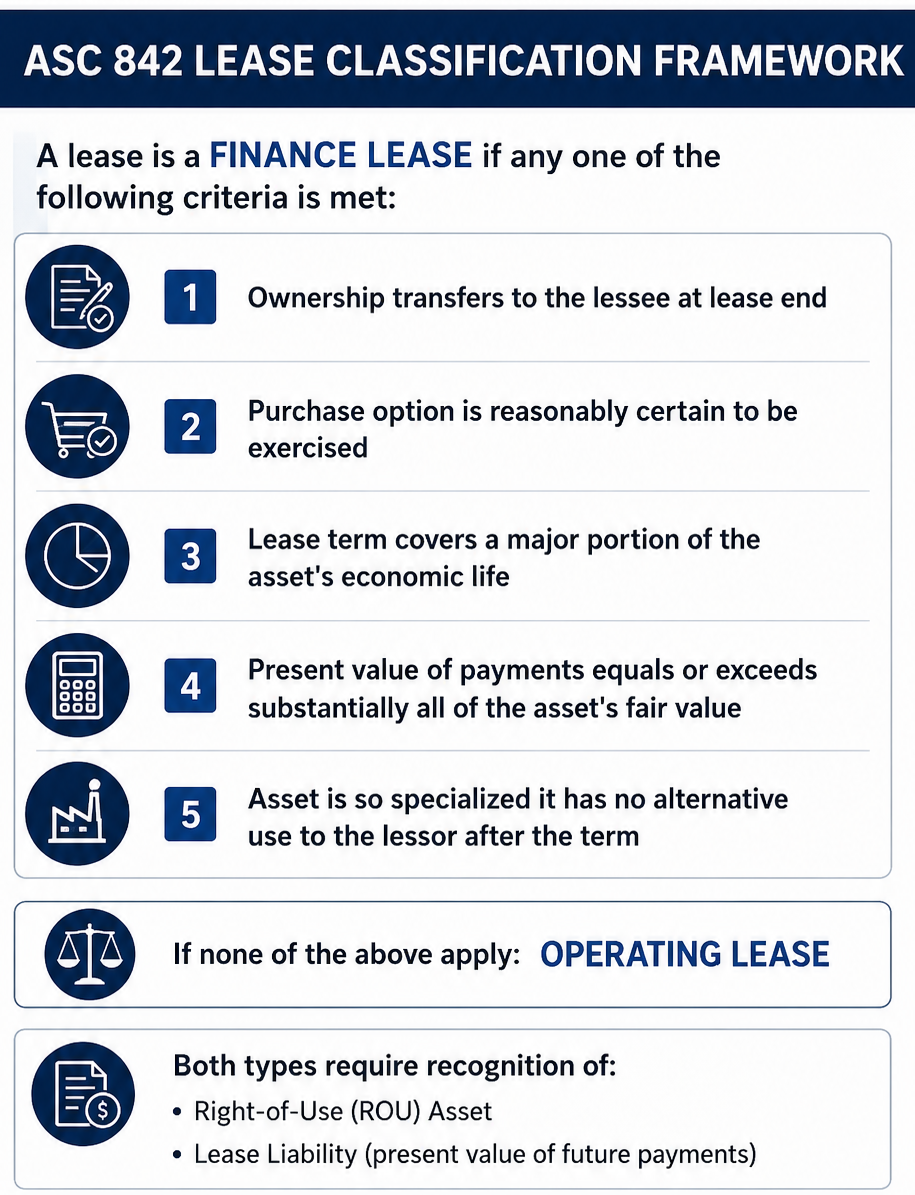

How the Classification Framework Works

The distinction between a finance lease and an operating lease under ASC 842 is determined by five criteria, each grounded in economic substance rather than contractual form.

The financial statement treatment diverges meaningfully between the two classifications. Finance leases produce front-loaded expense recognition, separating interest expense from amortization of the right-of-use asset. Operating leases retain the familiar straight-line expense pattern on the income statement, though the liability and asset now appear on the balance sheet. Both classifications represent the same underlying reality: a company has secured the right to use an asset and carries an obligation to pay for it.

This distinction matters in practice because finance lease expense, composed of depreciation and interest, does not reduce EBITDA, while operating lease expense does. Finance leaders should be aware that classification choices can influence reported operating performance, and auditors scrutinize classification decisions carefully for that reason.

Measuring the Right-of-Use Asset and Lease Liability

At lease commencement, the lessee recognizes a lease liability equal to the present value of all future lease payments over the lease term. The discount rate applied is either the rate implicit in the lease, when it is readily determinable, or the lessee’s incremental borrowing rate. The lessee then measures the right-of-use asset by taking the initial lease liability and adjusting it for any prepaid payments, initial direct costs, and lease incentives received from the lessor.

The choice of discount rate carries more consequence than it may appear. It affects the initial size of both the liability and the asset, subsequent interest expense, and in some cases the classification outcome itself. For private companies without observable market borrowing rates, estimating the incremental borrowing rate requires treasury judgment, reference to recent debt issuances, and benchmarking against comparable credit profiles. Errors at this step can produce material misstatements.

Across engagements in sectors with complex capital structures, I have seen this step treated as mechanical when it is anything but. The incremental borrowing rate exercise is an intersection of finance, treasury, and audit judgment, and it deserves the same rigor applied to any significant accounting estimate.

The Hidden Complexity: Embedded Leases

One of the most underestimated dimensions of ASC 842 lease accounting is the treatment of embedded leases within service contracts. A service agreement creates an embedded lease when it grants the customer the right to control the use of a specific, identifiable asset for a period of time, even if the parties did not structure or label the contract as a lease.

A cloud computing agreement that grants exclusive access to a specific server rack, or a logistics arrangement that allocates dedicated vehicles solely to a single customer, may contain an embedded lease component that the lessee must recognize on the balance sheet. The test turns on whether the customer controls both the use of the identified asset and substantially all of the economic benefit from that use throughout the contract period.

Identifying these obligations requires a cross-functional review of contracts spanning procurement, legal, and finance. It is time-consuming and interpretively demanding. Firms that have not formalized their contract review processes frequently miss embedded obligations until audit cycles surface them, creating restatement risk and reputational cost.

The embedded lease concept reflects ASC 842’s core philosophy in its most direct form: companies must disclose economic control regardless of what a contract chooses to call the arrangement.

Strategic and Operational Consequences

The impact of ASC 842 on a company’s financial presentation extends well beyond the balance sheet. Several dimensions deserve direct attention.

Leverage ratios increase when lease liabilities are recognized. Organizations that previously described themselves as asset-light now carry material balance sheet obligations. This requires proactive communication with lenders, investors, and rating agencies. In some cases, it necessitates covenant renegotiation or the revision of definitions in credit agreements.

Return on assets and return on invested capital may appear compressed, with right-of-use assets added to the denominator of performance calculations even when underlying operations are unchanged. Finance leaders must contextualize these effects in investor communications and valuation discussions.

EBITDA, widely used as a proxy for operating performance, is directly affected by the classification decision. This creates an incentive to favor finance lease classification for optical reasons, though that approach invites scrutiny and is not a reliable strategy for financial positioning.

The transition to ASC 842 also exposed operational gaps in many organizations. Companies that lacked centralized lease inventories discovered contracts in unexpected places: embedded in facilities management agreements, technology procurement deals, and service arrangements with single-use equipment. One multi-jurisdiction organization discovered ten million dollars in previously unrecognized lease liabilities in co-location contracts during its transition review. The accounting adjustment was manageable. The covenant renegotiation that followed was not trivial.

What Implementation Taught Finance Leaders

The most durable lesson from ASC 842 adoption is that compliance and strategy are not separate conversations. Companies that treated the standard as a one-time accounting exercise extracted limited value from the effort. Companies that used it to build a formal lease governance function, centralize contract administration, and establish clear ownership over renewal decisions found that the compliance burden evolved into an operational asset.

Centralized lease management enables better negotiation intelligence, earlier visibility into renewal obligations, and more accurate cash flow forecasting. It also supports the capital allocation discipline that informed CFOs apply across every category of committed expenditure.

Conclusion

ASC 842 lease accounting arrived as a regulatory mandate and has matured into a tool for genuine financial transparency. By bringing right-of-use assets and lease liabilities into the primary financial statements, the standard closes a long-standing gap between the balance sheet and economic reality. For CFOs, the implications are both technical and strategic: measurement discipline matters, classification decisions carry income statement consequences, embedded leases demand cross-functional vigilance, and covenant management requires proactive modeling. Organizations that engage seriously with ASC 842 find that the standard does not merely change how leases are reported. It changes how leases are managed, negotiated, and governed. That shift, from accounting compliance to capital discipline, is precisely the kind of operating improvement that creates lasting financial strength.

Disclaimer: This blog is intended for informational purposes only and does not constitute legal, tax, or accounting advice. You should consult your own tax advisor or counsel for advice tailored to your specific situation.

Hindol Datta is a seasoned finance executive with over 25 years of leadership experience across SaaS, cybersecurity, logistics, and digital marketing industries. He has served as CFO and VP of Finance in both public and private companies, leading $120M+ in fundraising and $150M+ in M&A transactions while driving predictive analytics and ERP transformations. Known for blending strategic foresight with operational discipline, he builds high-performing global finance organizations that enable scalable growth and data-driven decision-making.

AI-assisted insights, supplemented by 25 years of finance leadership experience.