Executive Summary

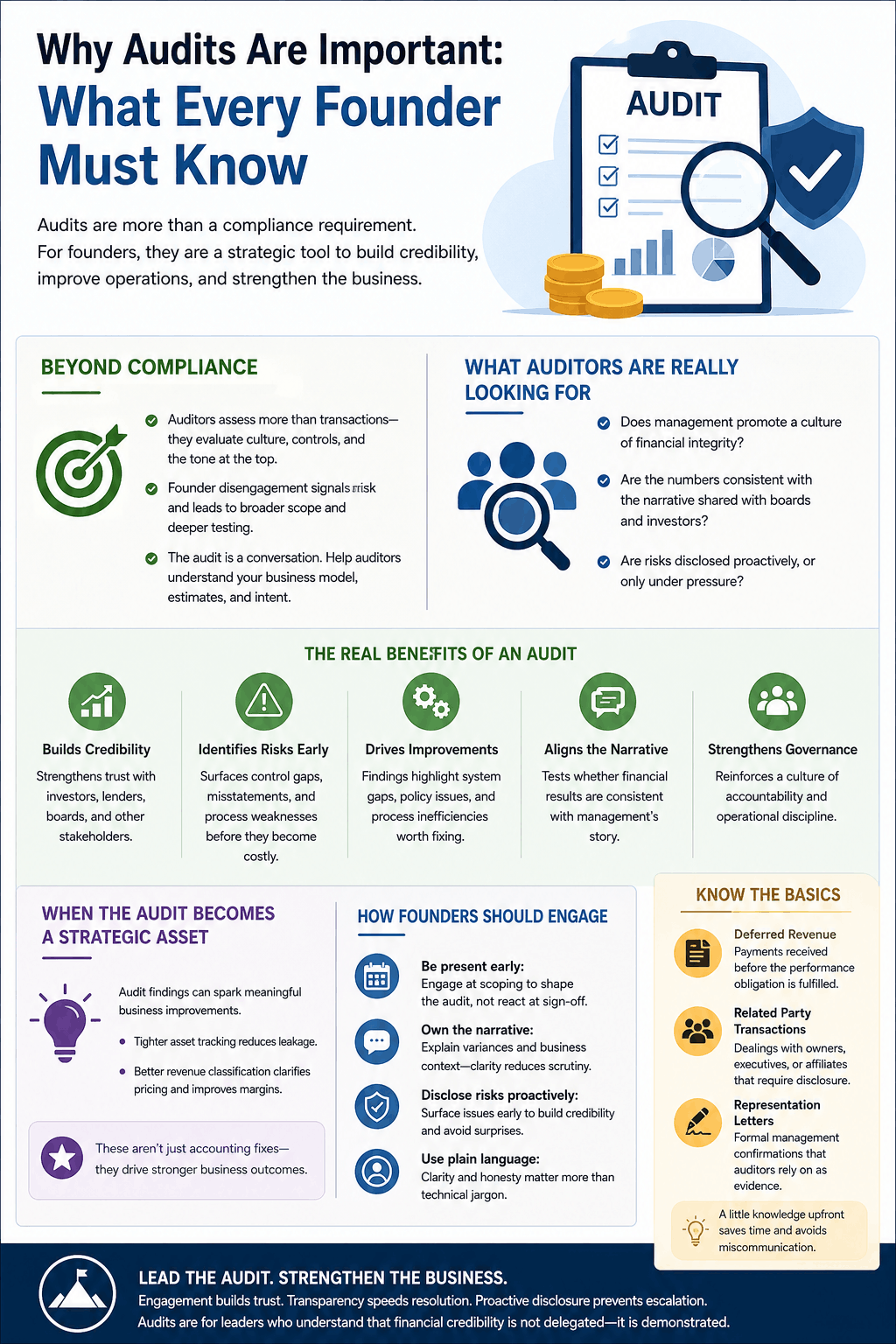

Audits are not merely a compliance obligation. For founders and executive leaders, they are one of the most direct windows into the financial health, control environment, and cultural integrity of an organization. A founder who understands why audits are important, and who engages with the process thoughtfully, does more than satisfy an investor requirement. That founder shapes the audit narrative, accelerates resolution, and builds lasting credibility with auditors, boards, and capital markets. This article draws on thirty years of operational CFO experience across Silicon Valley to explain what audits reveal, what the benefits of an audit extend beyond the income statement, and how founders can lead rather than delegate their way through the process.

Why Audits Are Important Beyond Compliance

Most founders associate the audit with document requests, reconciliation lists, and revenue recognition debates. That association is not wrong, but it is incomplete. Auditors evaluate more than transactions. They assess the tone at the top: whether leadership promotes accountability, whether controls are designed with integrity, and whether the organization presents a fair view of its financial position.

When a founder stays invisible during the audit, that absence sends a signal. Auditors notice disengagement. In response, they tend to broaden scope, deepen testing, and adopt more conservative positions, particularly in companies with rapid growth, complex revenue structures, or recent fundraising rounds. Founder engagement, by contrast, accelerates trust and speeds resolution.

The audit is also a conversation, not a compliance exam. Auditors want to understand the business model, the logic behind key estimates, and the intent behind contract structures. A founder who can explain consumption-based billing, multi-year prepaid arrangements, or bundled product offerings gives auditors the context that accounting schedules alone cannot provide.

What Auditors Are Really Looking For

When auditors enter an engagement, they bring three questions that sit beneath every document request:

- Does management promote a culture of financial integrity, or does finance operate in isolation?

- Are the numbers consistent with the narrative leadership communicates to boards and investors?

- Are risks disclosed proactively, or do they surface only under pressure?

A founder who answers these questions through behavior, not just documentation, changes the character of the audit entirely.

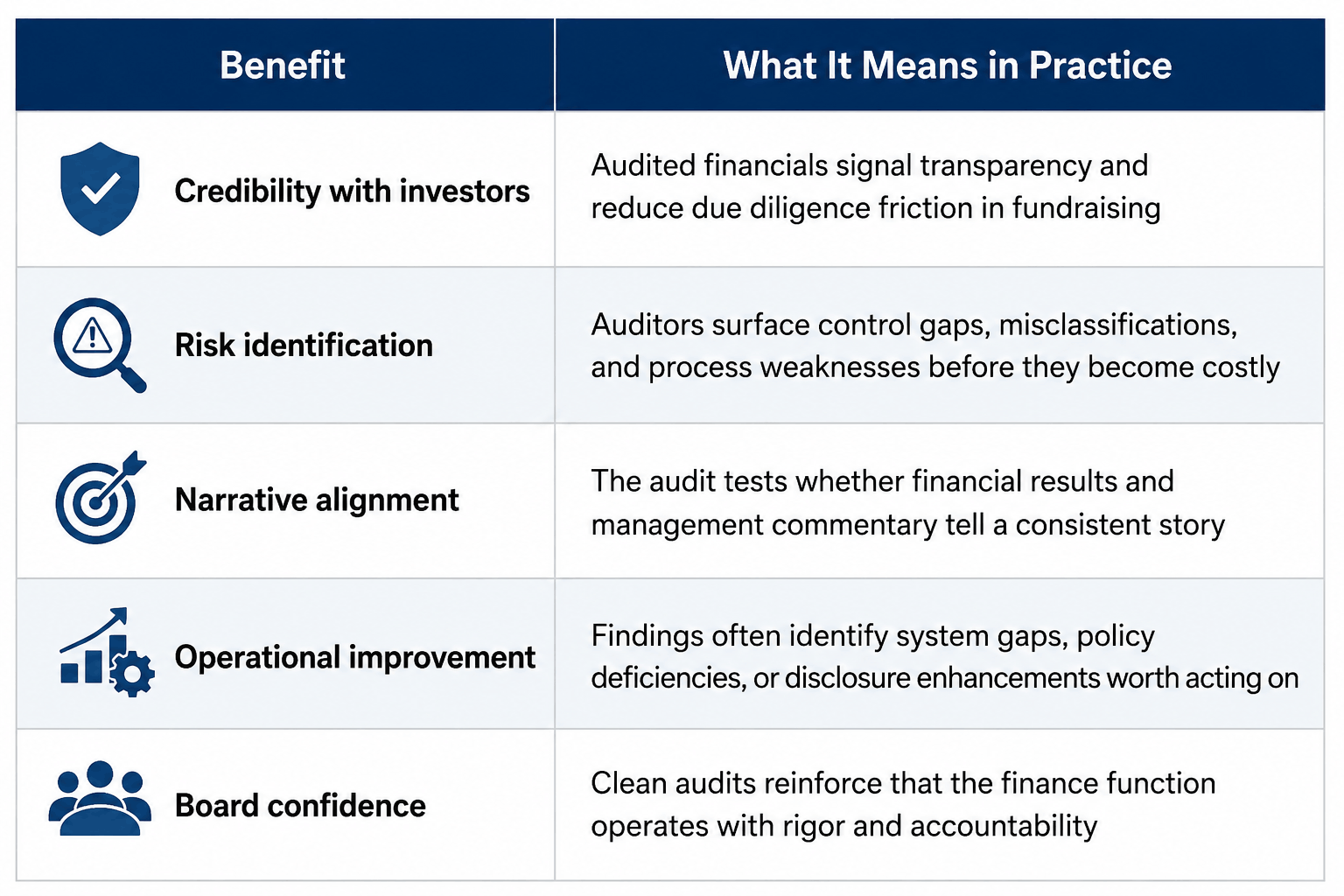

The Real Benefits of an Audit

The benefits of an audit are frequently understated in founder conversations. They extend well beyond the signed opinion letter.

In my experience overseeing finance functions across cybersecurity, SaaS, logistics, and nonprofit organizations, including during a forty-eight million dollar capital raise at a mission-driven education institution, the audit consistently delivered its most durable value not in the opinion itself but in what it revealed about the organization’s operational discipline.

When the Audit Becomes a Strategic Asset

Founders who treat the audit as a one-time annual obligation miss a recurring opportunity. The process, when approached with genuine engagement, can surface improvements with lasting commercial value.

In one portfolio company, an audit finding on fixed asset tracking prompted the founder to implement a cloud-based management system that reduced expense leakage across the business. In another, guidance on revenue classification led to a reworking of pricing tiers that improved gross margin clarity. These are not accounting corrections. They are strategic improvements that began with a conversation.

How Founders Should Engage With the Audit Process

Engagement does not require accounting expertise. It requires ownership. A founder who participates in kickoff calls, scoping discussions, and management interviews demonstrates accountability in the precise way auditors are trained to recognize.

There are a few practical principles worth following:

- Be present early. Founders who engage at the scoping stage shape how the audit is framed. Those who appear only at sign-off inherit the framing someone else set.

- Own the narrative behind large variances. If burn increased, explain why. If revenue slowed, articulate the strategic context. Auditors who understand the story probe less.

- Disclose risks proactively. Auditors expect to find issues. A founder who surfaces a resolved option grant dispute in a footnote earns credibility. One who conceals it creates exposure.

- Use plain language. Auditors do not require founders to speak in technical terms. They require precision in thinking. Describing facts clearly and stating intentions honestly accomplishes more than memorized terminology.

Know the Basics

A founder does not need to reconcile revenue deferrals, but a working familiarity with a few core concepts prevents costly miscommunication:

- Deferred revenue refers to payments received before the performance obligation is fulfilled.

- Related party transactions are dealings between the company and its owners, executives, or affiliated entities that require specific disclosure.

- Representation letters are formal management confirmations that auditors rely on as part of their evidence base.

An hour spent with the CFO or controller reviewing these concepts before the audit begins saves days of clarification later.

Conclusion

The founder who treats the audit as a leadership exercise rather than an accounting exercise changes what the process produces. Engagement builds trust. Transparency accelerates resolution. Proactive disclosure prevents escalation. And the findings, when acted upon, improve the organization that will face the next audit in better condition than it entered the last. Audits are not just for accountants. They are for leaders who understand that financial credibility is not delegated. It is demonstrated.

Disclaimer: This blog is intended for informational purposes only and does not constitute legal, tax, or accounting advice. You should consult your own tax advisor or counsel for advice tailored to your specific situation.

Hindol Datta is a seasoned finance executive with over 25 years of leadership experience across SaaS, cybersecurity, logistics, and digital marketing industries. He has served as CFO and VP of Finance in both public and private companies, leading $120M+ in fundraising and $150M+ in M&A transactions while driving predictive analytics and ERP transformations. Known for blending strategic foresight with operational discipline, he builds high-performing global finance organizations that enable scalable growth and data-driven decision-making.

AI-assisted insights, supplemented by 25 years of finance leadership experience.