Executive Summary

What is transfer pricing, and why does it matter to a startup with no obvious international tax exposure? The answer arrives faster than most founders expect. One engineering hire abroad, one pilot deployment in a new country, or one foreign subsidiary is often enough to trigger transfer pricing rules. This article explains how transfer pricing works, when it becomes relevant for early-stage companies, and which methods and documentation requirements matter most at each funding stage. It draws on direct experience helping venture-backed startups expand across multiple countries, where undocumented intercompany arrangements repeatedly became points of friction during audits and acquisition diligence. The goal is to help founders and finance leaders treat transfer pricing as a structural discipline built early, rather than a compliance task addressed only once regulators or acquirers ask for it.

Why Transfer Pricing Arrives Sooner Than Founders Expect

In the earliest stages of a startup, international tax strategy rarely feels urgent. Most founders focus on product-market fit, early hires, and closing a first institutional round. Expansion abroad often feels like a future possibility rather than a present obligation. That changes quickly. A single strategic hire in another country, a pilot deployment with an overseas customer, or a small development team abroad is often enough to shift a company’s entity map across borders, and with it comes one of the more opaque areas of global taxation.

Transfer pricing is not primarily about reducing tax. It is about defensibility. Companies that understand this early tend to avoid disputes, double taxation, and slow audits later. Companies that treat it as an afterthought often face financial penalties, but the more lasting cost is reputational, particularly in the eyes of acquirers and regulators evaluating the company’s overall discipline.

What Is Transfer Pricing in Practice

Transfer pricing governs how related entities within the same corporate group transact with each other across borders. It applies whenever goods, services, or intellectual property move between a parent company and a foreign subsidiary or branch. The underlying principle is straightforward. The price charged between related parties should reflect what independent parties would agree to under similar circumstances, a standard generally referred to as the arm’s length principle.

This rule exists for a clear reason. Without it, multinational companies could shift profits into low-tax jurisdictions simply by adjusting internal prices. A parent company might charge a foreign subsidiary an inflated fee for software licensing to reduce taxable income at home, or underpay a foreign engineering office to lower reported earnings there. Transfer pricing tax rules exist to keep these internal transactions priced reasonably, so that each jurisdiction collects a fair share of tax on the value actually created within it. Every major economy enforces some version of these rules today, and company size offers no exemption. The moment a startup operates in more than one country, transfer pricing scrutiny becomes a possibility.

When the Threshold Is Reached

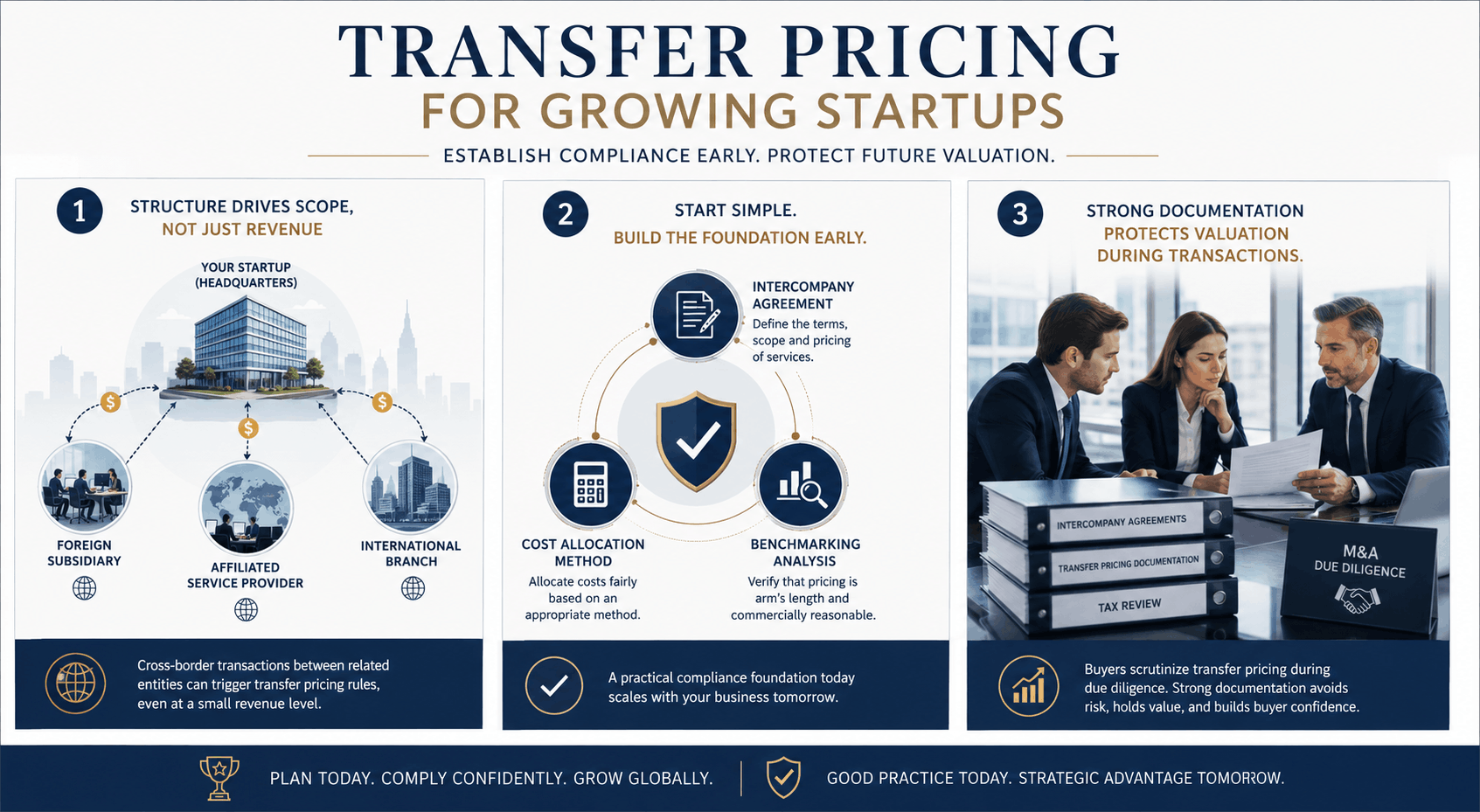

For early-stage companies, the threshold for relevance is lower than most founders assume. It depends on structure rather than revenue. A wholly owned subsidiary, a branch office, or even an affiliated service provider abroad, combined with money moving between entities, is generally enough to bring transfer pricing into scope.

Common situations include a company hiring developers abroad through a foreign subsidiary, selling software through a local sales office in another country, or assigning engineers in a different jurisdiction to maintain core product infrastructure. In each case, value is being created or consumed across borders, and the internal pricing tied to that value needs to be documented and rational. Intellectual property follows the same logic. If a parent company owns the core IP while a foreign subsidiary contributes to its development or sale, the company typically needs to compensate that value through royalties, cost-sharing arrangements, or a similar mechanism. Leaving these flows undocumented can invite audit attention and create unexpected intercompany debt, currency exposure, or VAT liabilities.

Methods Startups Commonly Use

Several accepted methodologies exist for establishing arm’s length prices, though only a few tend to apply to early-stage companies in practice.

- The Comparable Profits Method, the most commonly used approach for startups, evaluates whether an entity’s profit margin aligns with what similar independent companies earn.

- Companies often apply a cost-plus markup to functions such as a development center providing engineering services or a regional office handling marketing, with benchmarks drawn from industry data.

- More advanced methods, including the Transactional Net Margin Method or Profit Split Method, tend to apply only when intellectual property moves or generates value across multiple jurisdictions.

For most startups, early compliance is less about choosing a sophisticated method and more about setting basic service fees, documenting intercompany charges, and putting simple, defensible agreements in place. Consistency matters as much as the method itself. Tax authorities examine behavior alongside numbers, and a mismatch between an intercompany agreement and the company’s actual books tends to raise more questions than the absence of perfect precision. When no agreement exists at all, regulators often assume value is being hidden rather than simply overlooked.

Documentation and the OECD Framework

Most countries now follow OECD transfer pricing guidelines, which establish a three-tier documentation structure consisting of a master file, a local file, and a country-by-country report. The country-by-country threshold is set high enough that it rarely applies to startups, but the master file and local file are increasingly expected even from smaller companies operating across borders.

The master file describes the global group’s structure, business operations, and overall transfer pricing policies. The local file documents the specific intercompany transactions relevant to a particular jurisdiction, including pricing, benchmarking data, and supporting agreements. Even companies unlikely to face an audit in their first few years abroad are generally expected to maintain and update this documentation annually. Producing nothing when asked can lead to penalties, disallowed deductions for intercompany expenses, and accumulated interest.

This documentation gap surfaces most visibly during acquisition diligence. Buyers routinely request intercompany agreements and transfer pricing policies as part of tax due diligence, and incomplete documentation can lead to indemnification requirements, escrow holdbacks, or downward valuation adjustments that founders rarely anticipate until the process is underway.

Building Transfer Pricing Into the Startup Lifecycle

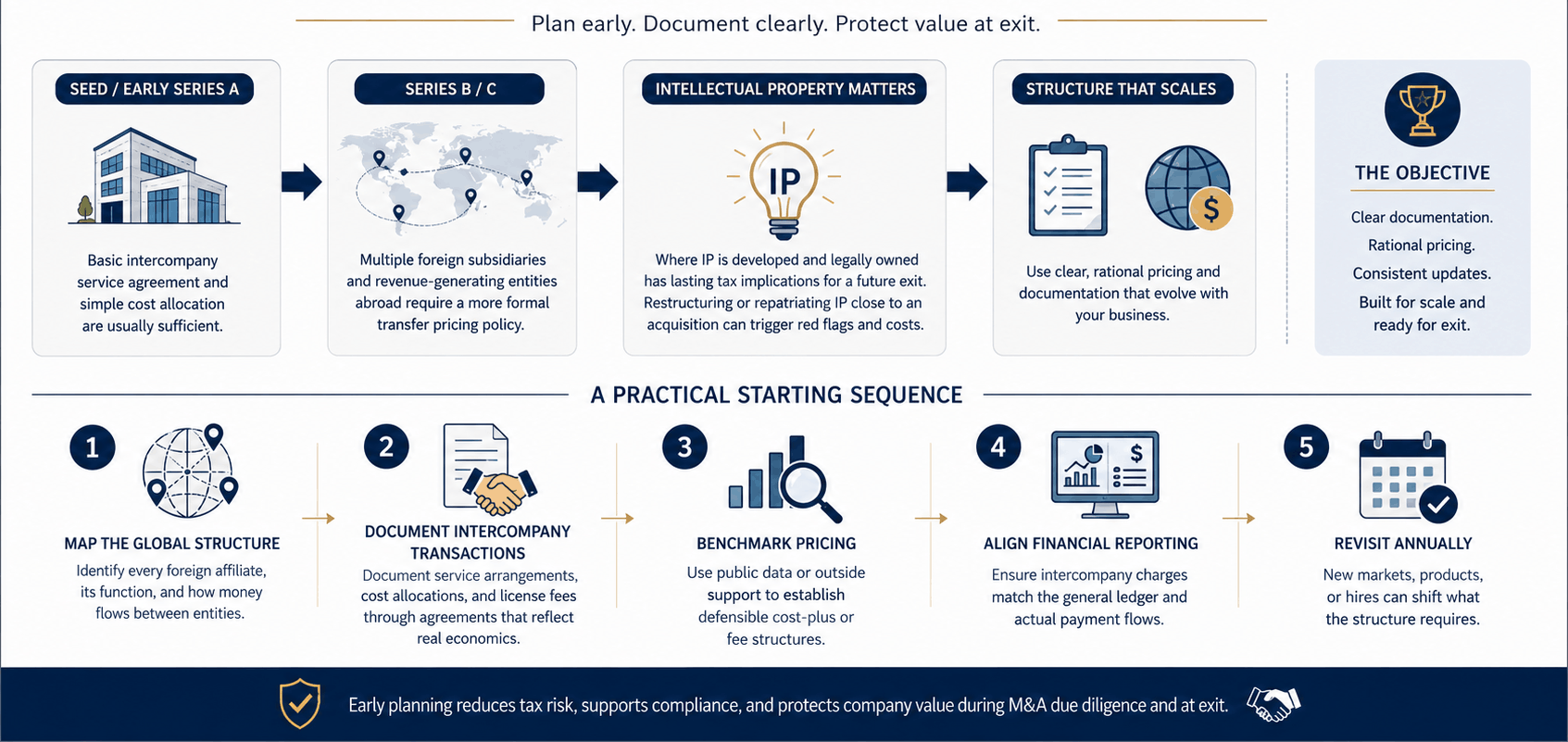

Transfer pricing complexity tends to grow with company scale, but planning works best when it begins early rather than retroactively. At seed or early Series A stages, a basic intercompany service agreement and simple cost allocation are usually sufficient. By the time a company reaches Series B or C, with multiple foreign subsidiaries and revenue-generating entities abroad, a more formal policy generally becomes necessary.

The location of intellectual property deserves particular attention, since where IP is developed and where it is legally owned carries lasting tax implications for a future exit. Restructuring intercompany relationships or repatriating IP close to an acquisition tends to raise red flags and unexpected costs, since the ideal structure is difficult to construct after the fact. Some companies rely on straightforward cost-plus arrangements, while others establish contract research entities abroad operating at a defined margin. The objective is not complexity for its own sake. It is clear documentation, rational pricing, and consistent updates as the business evolves.

A Practical Starting Sequence

Founders building this discipline for the first time tend to benefit from a simple sequence.

- Map the global structure, identifying every foreign affiliate, its function, and how money flows between entities.

- Review existing intercompany transactions and document any service arrangements, cost allocations, or license fees through agreements that reflect real economics.

- Benchmark pricing using public data or outside support to establish defensible cost-plus or fee structures.

- Align financial reporting so intercompany charges match what appears in the general ledger and actual payment flows.

- Revisit the approach annually, since new markets, products, or hires can shift what the structure requires.

Conclusion

Transfer pricing rarely feels urgent until a specific moment forces the issue, whether that moment is a tax audit, acquisition diligence, or IPO preparation, and by then the risk has often been accumulating quietly for years. Startups that treat transfer pricing as a one-time compliance task tend to stay reactive, while those that build it into their financial strategy from an early stage tend to move through audits and diligence with far less friction. A global footprint is no longer something only large enterprises need to plan around. Many startups expand internationally early, sometimes out of necessity and sometimes by deliberate strategy, and either path carries the same underlying responsibility. How a company handles transfer pricing tax obligations often signals whether it is genuinely prepared to grow with discipline, or whether it is simply expanding ahead of its own readiness.

Disclaimer: This blog is intended for informational purposes only and does not constitute legal, tax, or accounting advice. You should consult your own tax advisor or counsel for advice tailored to your specific situation.

Hindol Datta is a seasoned finance executive with over 25 years of leadership experience across SaaS, cybersecurity, logistics, and digital marketing industries. He has served as CFO and VP of Finance in both public and private companies, leading $120M+ in fundraising and $150M+ in M&A transactions while driving predictive analytics and ERP transformations. Known for blending strategic foresight with operational discipline, he builds high-performing global finance organizations that enable scalable growth and data-driven decision-making.

AI-assisted insights, supplemented by 25 years of finance leadership experience.