Executive Summary

Founders often picture venture capital as a partnership built around a single shared bet on a company’s success. The reality looks different from the investor’s side of the table. A venture fund operates as a portfolio of options, where most positions are expected to underperform and only a small number must deliver outsized returns to justify the entire fund. This article explains how that portfolio logic shapes decisions that can otherwise seem confusing to founders. It covers why some companies receive aggressive follow-on support while others do not, why investors encourage or discourage certain exits, and how liquidation preferences and fund metrics such as DPI influence investor behavior. It also covers how founders can use this understanding to negotiate more effectively and plan exits with foresight. And it shows how this understanding helps founders build stronger alignment with the investors who back them.

Two Different Views of the Same Company

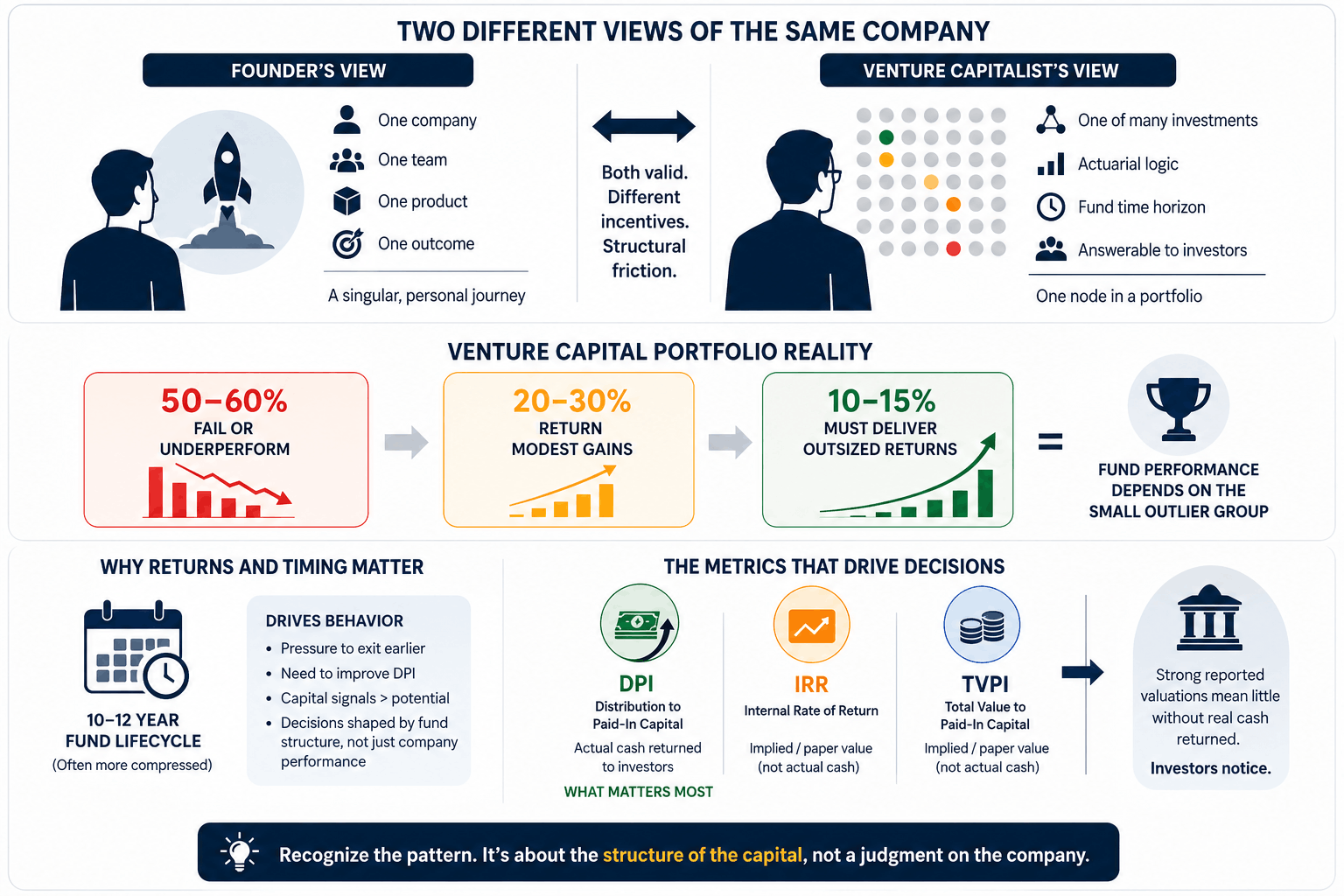

A founder typically experiences a startup as a singular, personal journey. Years of effort go into one product, one team, and one outcome. A venture capitalist experiences that same company very differently, as one node within a much larger portfolio built on actuarial logic rather than narrative. Neither perspective is wrong. The two are simply structured around different incentives. That friction shapes many of the decisions founders find hardest to understand, from valuation pressure to exit timing.

This friction is structural rather than personal. A venture capitalist may push for a sale at the exact moment a founder sees genuine signs of inflection. Or they may offer a new round with unusually strict liquidation preferences. One company might receive support through several pivots while another, performing similarly well on paper, quietly loses that support. These decisions rarely hinge on company performance alone. They also reflect the fund’s structure, its own investors, and the time horizon it must operate within, layers of context that are invisible to most founders.

These same patterns show up well beyond venture capital. Corporate innovation funds, M&A evaluation teams, and supplier negotiation processes often follow a similar shape, where the time horizon and constraints of the capital itself drive decisions more than most outside observers realize. Recognizing this pattern early, rather than assuming every funding decision reflects a judgment about a specific company, helps founders interpret investor behavior with far less frustration.

Why Venture Capital Operates as a Portfolio of Options

Venture capitalists are not, in a strict sense, investing in individual companies. They are investing in a portfolio of options. Most positions return little or nothing, a smaller group returns modest multiples, and only a handful must deliver the outsized gains that carry the entire fund. This is not a cynical view of entrepreneurship. It reflects the statistical reality of early-stage investing, where the distribution of outcomes is extremely uneven.

Why Fund Returners Matter More Than Average Performance

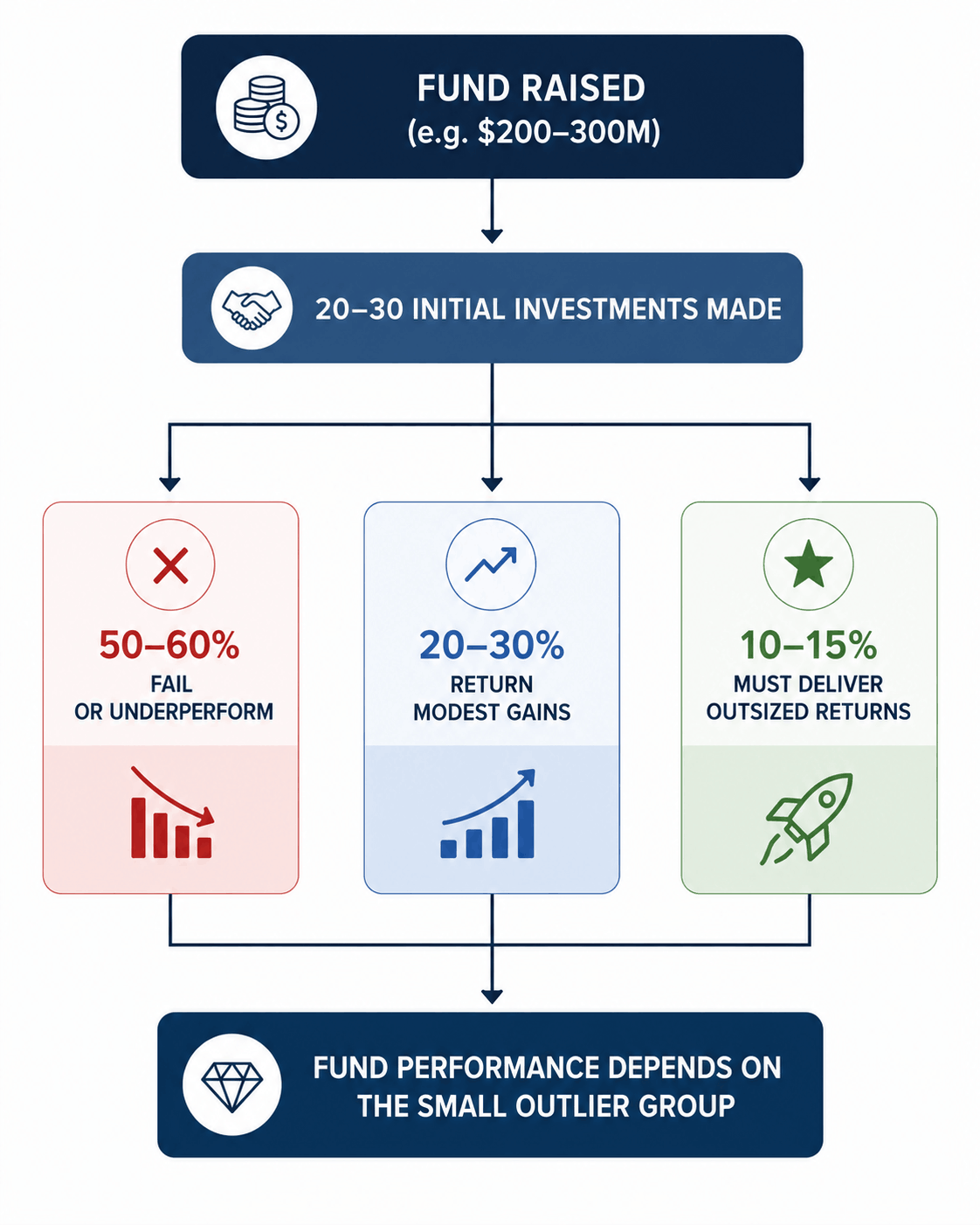

A fund of two hundred to three hundred million dollars typically needs at least one investment capable of returning an amount close to the full fund size on its own. It also needs several others contributing tens of millions more. These return profiles need to materialize within a ten to twelve year fund lifecycle, often compressed further by the expectations of the fund’s own investors. This single constraint explains a great deal of behavior that otherwise looks irrational from the outside.

When a venture capitalist pushes for an exit at what seems like a modest valuation, the motivation may have little to do with belief in the company’s long-term potential. It may instead reflect pressure to generate liquidity before the fund’s investment period closes. Or it may reflect pressure to improve a metric known as Distribution to Paid-In Capital, or DPI, which reflects actual cash returned to investors rather than paper gains. DPI carries particular weight because general partners rely on it when raising their next fund. A firm with strong reported valuations but little realized cash often struggles to win new commitments, regardless of how promising its portfolio looks on paper.

DPI differs from two other metrics founders may encounter, IRR and TVPI. Both of those measure implied or paper value rather than cash actually distributed to investors. A fund can show an impressive TVPI while still struggling to return real capital, and investors who allocate to future funds tend to notice this gap quickly. Because of this, exits are rarely just operational milestones from the fund’s point of view. They function as capital signals, and the pressure to demonstrate strong DPI often shapes investor behavior more than founders realize during early negotiations.

Venture Capital Financing and the Mechanics of the Capital Stack

Venture capital financing rarely arrives as a single, simple investment. Multiple funding rounds typically stack on top of each other, each carrying its own terms. Those terms shape what happens at exit far more than most founders initially expect.

Liquidation preferences sit at the center of this dynamic. These clauses guarantee investors a minimum return before founders or common shareholders see any proceeds from a sale. A standard arrangement is often considered reasonably founder friendly. As additional rounds stack preferences, sometimes with ratchets or participation rights attached, an exit can leave founders and employees with little or nothing. This can happen even when the company sells at a headline valuation that appears successful on the surface. The outcome reflects how the capital stack was structured rather than any failure on the founder’s part.

Few first-time founders model these scenarios in advance. Most focus on building the product, growing revenue, and hitting the next milestone, which is reasonable given where their attention needs to be day to day. Founders who do take the time to understand exit waterfalls and preference structures tend to negotiate more effectively. They also tend to avoid unpleasant surprises later. Experienced founders, particularly those who have built and sold companies before, often think in portfolio terms themselves. They understand that their company is one of many bets a fund is managing, and they negotiate preferences, timing, and follow-on terms with that context in mind.

The Role Limited Partners Play Behind the Scenes

Limited partners, the institutions and family offices that supply capital to venture firms, add another layer to this picture. LPs are not investing in individual companies. They are investing in fund managers who promise discipline, pattern recognition, and the eventual return of capital. A firm that fails to return capital reliably across successive funds risks losing access to future commitments. That risk shapes how general partners behave even within their current fund. This nested structure of incentives, running from company to fund to LP, explains a great deal of behavior that can otherwise look short-termist or disconnected from a founder’s day-to-day reality.

Understanding What Venture Capital Is From a Portfolio Construction Standpoint

To understand what venture capital is at a structural level, it helps to look at how a fund is built from its first check onward. Most early-stage funds plan for twenty to thirty initial investments. Assumptions about check size, ownership targets, and reserve capital for follow-on rounds get set years in advance. A meaningful share of that portfolio, often fifty to sixty percent, is expected to fail outright or return less than the capital invested. Another significant portion returns modest multiples, enough to recover costs without driving real fund performance. A small remaining slice, often ten to fifteen percent, must generate extraordinary returns for the fund to succeed overall.

This explains a pattern that frequently puzzles founders. A steadily growing, profitable company may receive less attention and follow-on capital than a higher-risk startup chasing a much larger market with no current revenue. The decision can feel irrational from inside the steady company. It reflects portfolio math rather than a judgment about the founder’s execution. A company with the potential to return thirty times the original investment carries disproportionate value in a fund built around outliers. This holds true even when a more conservative company appears safer on a standalone basis.

The Pull Toward Unicorn Outcomes

This is also why venture funds gravitate toward unicorn outcomes, companies valued above one billion dollars. A single investment capable of returning several hundred million dollars on a modest initial check can cover the losses across an entire portfolio and still produce strong overall performance. This asymmetry explains the emphasis many investors place on market size and category leadership over near-term profitability. It also explains why some funds quietly discourage an exit that looks attractive to a founder but contributes too little to move the fund’s overall numbers.

This dynamic becomes especially visible during growth rounds. A company may be performing well without being exceptional. Growth remains solid, but capital efficiency is slipping. Competition is intensifying just as a new investor offers to lead a round at a modest valuation step-up. The existing investor must then decide whether to use limited reserve capital to maintain ownership, or redirect that capital toward a different company in the portfolio with greater potential to become a fund returner. The decision can feel deeply personal to a founder who has built genuine momentum. It reflects opportunity cost calculated across the whole portfolio rather than a verdict on any single company’s quality.

How Founders Can Apply This Understanding

Founders who grasp how fund construction shapes investor behavior tend to negotiate from a stronger position. A few practices consistently help.

- Simulate exit scenarios across a low, mid, and high valuation range, including the effect of liquidation preferences and any convertible instruments, before negotiating new terms.

- Understand each investor’s fund age, fund size, and likely DPI pressure, since later-stage and earlier-stage investors often want different things at the same moment.

- Consider a structured secondary sale at a later funding stage, allowing founders to reduce personal financial pressure while signaling continued conviction to the market.

These practices do not change the underlying math of venture capital financing, but they help founders anticipate pressure points rather than react to them after the fact.

Why Structured Secondaries Matter

A structured secondary deserves particular attention because it serves multiple parties at once. Once a company reaches a certain stage, often after a Series B round, founders may sell a small portion of their equity to new or existing investors. This reduces personal financial pressure on the founder and signals continued conviction to the broader market. It can also rebalance control where early dilution was significant. Earlier investors nearing the end of their fund’s life sometimes prefer this path as well. They may choose a partial exit through a secondary sale rather than waiting years for an uncertain initial public offering. Founders who initiate these conversations with a clear understanding of fund cycles tend to be seen as strategic partners rather than as opportunistic sellers.

Navigating Competing Investor Incentives

As a company raises multiple rounds, the cap table itself becomes a place where competing incentives surface. Later-stage investors, often holding board influence, may push for a quicker exit to secure their return, while earlier investors may prefer to hold longer to preserve upside. Founders frequently find themselves negotiating between these positions. Understanding each investor’s fund age, ownership stake, and DPI goals becomes less a courtesy and more a practical necessity for steering the company toward an outcome that works reasonably well for everyone at the table.

A Simple View of Fund Logic

The relationship between portfolio construction, individual company performance, and fund-level outcomes can be summarized as follows.

Exit Planning as a Strategic Discipline

Building a great company and engineering a strong exit are related but distinct pursuits. One is operational, built through hiring, product development, and market timing. The other is structural, shaped by cap table mechanics, investor psychology, and broader liquidity cycles. Founders who treat exit planning as a late-stage afterthought often find themselves negotiating from a weaker position than those who build this thinking into the company from early on.

Market timing adds another layer of complexity, particularly in sectors such as enterprise software or biotechnology, where public market sentiment can shift valuations quickly. Founders who wait too long for an ideal moment may miss a closing window. Those who move too early may face pressure before the business is fully ready. Coordinating business readiness with capital market conditions usually requires ongoing dialogue. This dialogue typically involves experienced finance leadership, bankers, and investors rather than a single internal decision.

The CFO’s Role in Translating Performance for Investors

Experienced finance leaders play a particular role in bridging internal operations with external capital signals. A growth rate that feels strong internally may look weak if the broader sector benchmark sits higher. This directly affects how outside investors apply valuation multiples to the business. Strategic CFOs translate operational performance into language that investors and acquirers can interpret accurately. This helps ensure that a company is not only growing, but is also being positioned clearly for whatever liquidity event eventually follows. This translation work often determines whether strong internal metrics actually convert into a strong external valuation. The conversion from internal performance to external value is rarely automatic.

Team Alignment and Reputation Through the Exit Process

Team expectations deserve attention as well, since startup compensation is often tied closely to equity value. The timing and shape of an eventual exit affects morale, retention, and recruiting long before any transaction occurs. Founders who communicate openly about exit horizons, without overpromising specific outcomes, tend to build stronger alignment across their teams. This also helps reduce resentment if a secondary sale or acquisition offer eventually changes the company’s trajectory.

Reputation plays a lasting role once exit conversations begin in earnest. How a founder handles that process tends to follow them into future ventures and future fundraising relationships. This includes whether they maximize value fairly, communicate with transparency, and protect employees where possible. From the investor’s side, a successful exit represents more than a single liquidity event. It validates the original thesis, reduces portfolio risk, and strengthens the track record a fund relies on when raising its next vehicle. Seen this way, exits are not simply endings for either party. They are measured outcomes weighed against the needs of the entire portfolio. Founders who recognize this tend to navigate the final stretch with far less friction.

Conclusion

Venture capital financing operates on a logic that is structural rather than personal, even though the relationships involved are often genuinely collaborative. A venture fund must generate a small number of outsized returns to justify the risk taken across its entire portfolio. This single fact explains much of what can otherwise look like inconsistent or confusing investor behavior. Liquidation preferences, fund age, and metrics such as DPI all shape decisions. These decisions have little to do with any individual founder’s effort or execution. Founders who understand this map are better equipped to negotiate fair terms and anticipate pressure points around follow-on funding and exit timing. They can also build companies that serve their own interests alongside their investors’ fund requirements. None of this requires abandoning ambition or trust between founders and investors. It simply means approaching the relationship with clarity about how each side is incentivized, which tends to produce stronger outcomes and fewer surprises for everyone involved when the time eventually comes to exit.

Disclaimer: This blog is intended for informational purposes only and does not constitute legal, tax, or accounting advice. You should consult your own tax advisor or counsel for advice tailored to your specific situation.

Hindol Datta is a seasoned finance executive with over 25 years of leadership experience across SaaS, cybersecurity, logistics, and digital marketing industries. He has served as CFO and VP of Finance in both public and private companies, leading $120M+ in fundraising and $150M+ in M&A transactions while driving predictive analytics and ERP transformations. Known for blending strategic foresight with operational discipline, he builds high-performing global finance organizations that enable scalable growth and data-driven decision-making.

AI-assisted insights, supplemented by 25 years of finance leadership experience.