Executive Summary

Revenue recognition often gets treated as an administrative task, but ASC 606’s performance obligation rules turn it into an operational discipline. The standard replaced fragmented legacy guidance with a single five-step model that ties revenue timing to actual value transfer rather than billing or cash. This summary walks through how to judge whether revenue belongs at a point in time or over time, how different contract types change that judgment, and where CFOs, controllers, and auditors tend to get tripped up. It closes with a short compliance checklist and a set of common questions leadership teams ask when building this discipline into everyday systems, not just year-end close.

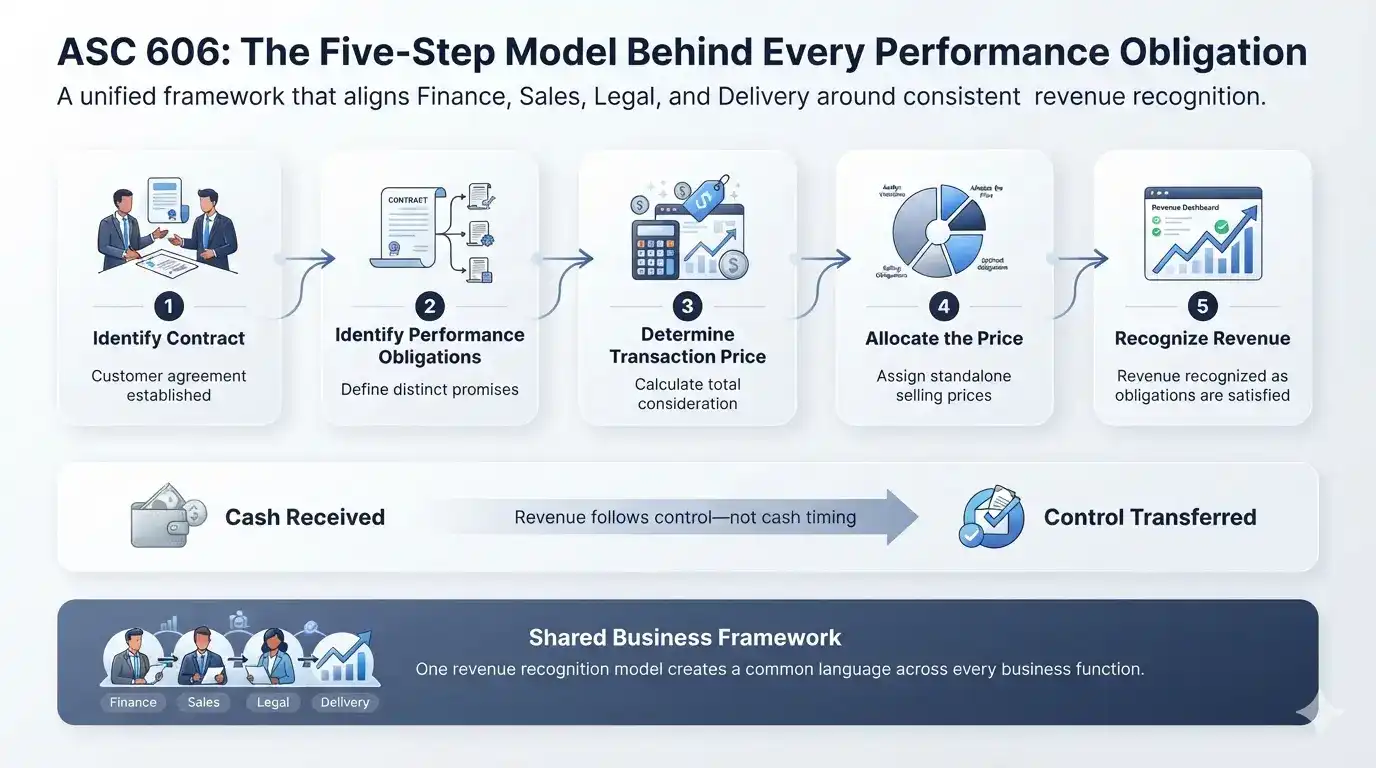

The Five-Step Model Behind Every Performance Obligation

This structure gives every function a common language. It shifts attention away from when cash arrives and toward when control of a good or service actually transfers.

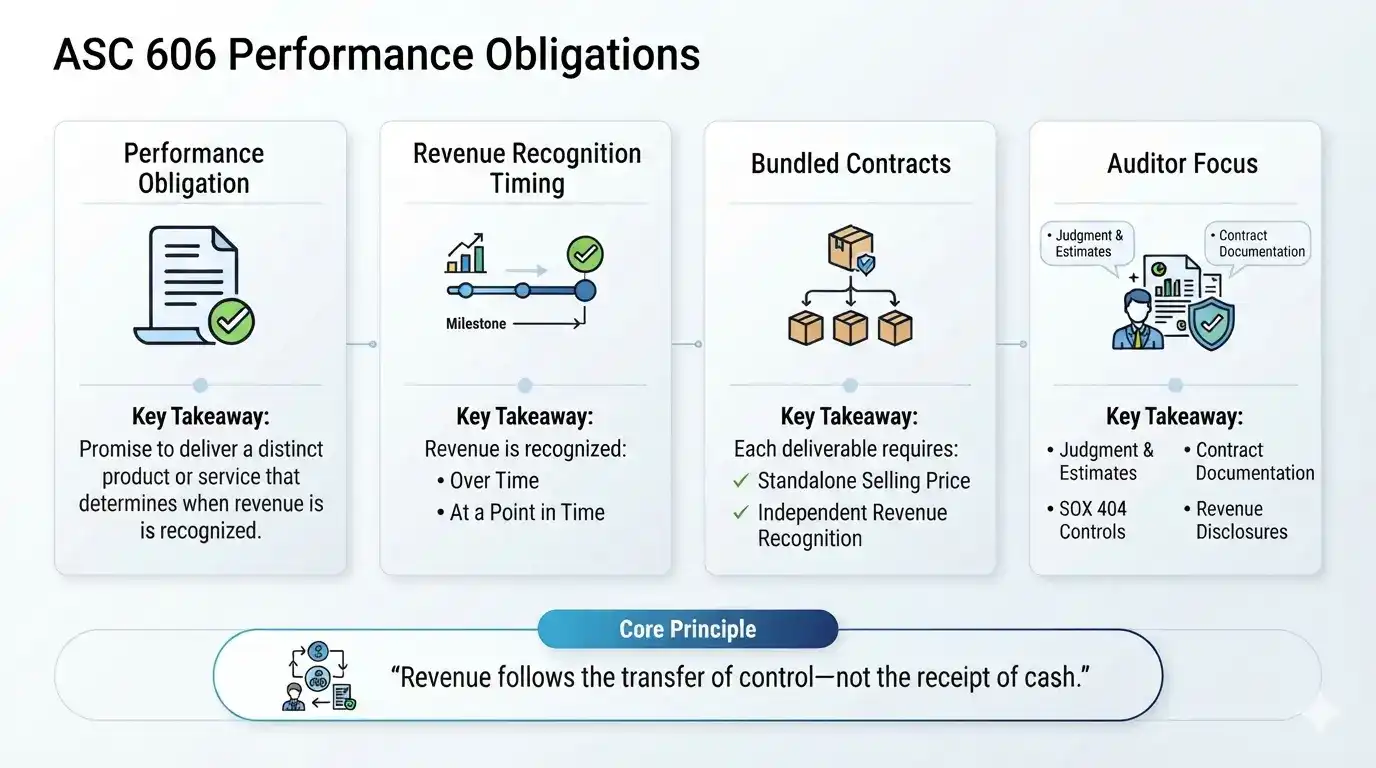

Point in Time or Over Time: The Core Judgment

Three criteria decide whether revenue is recognized over time. The customer must consume the benefit as the entity performs. The entity’s work must create or control an asset the customer controls as it forms. Or the work must create no alternative-use asset while the entity holds an enforceable right to payment. Subscription and consulting services usually qualify for over-time recognition. A software license, once delivered and usable, typically qualifies for point-in-time recognition instead.

How Contract Type Shapes Performance Obligation Accounting

Different contract structures change how this judgment plays out in practice.

| Contract Type | Recognition Trigger | Key Risk |

| Time-and-Materials | Hours logged or materials delivered | Timesheet and billing accuracy |

| Fixed-Fee | Milestones or completion | Poorly defined milestones |

| Percentage of Completion | Cost incurred versus total estimated cost | Estimate reliability |

| Bundled Goods and Services | Each distinct deliverable separately | Misallocated standalone pricing |

| License with Royalty | Usage occurs | Early recognition based on estimates |

Bundled contracts, such as a SaaS agreement with setup and training, need special care. Each component must be treated as its own obligation. Software access might recognize at the start, while training revenue spreads over the implementation period. Usage-based royalties tied to intellectual property follow a separate exception, recognizing revenue only as usage occurs rather than upfront.

Where CFOs and Auditors Get Tripped Up

A handful of areas cause most restatements and audit findings:

- Variable consideration, including discounts and rebates, needs constraint based on historical data rather than optimistic estimates.

- Contract modifications can quietly create new obligations that require separate accounting treatment.

- Principal versus agent determination decides whether revenue records gross or net, and getting it wrong distorts topline growth.

- Material rights, such as options for future discounts, can create obligations that were never explicitly priced.

- Channel stuffing inflates bookings while delaying real recognition, which auditors and boards both watch closely.

Auditors focus heavily on judgment and estimates, contract documentation, and internal controls tied to SOX 404. Disclosure quality, including revenue disaggregation and contract balance changes, receives similar scrutiny.

A Compliance Checklist for Performance Obligation Accounting

A practical rollout usually includes contract review controls that block quoting without a revenue treatment tag. It also includes documented performance obligation mapping and standalone selling price logic embedded directly into CPQ or ERP systems. Training for sales, deal desk, and delivery teams matters just as much as the technical accounting. Most misstatements start upstream of finance. System integration across CRM, billing, and ERP keeps the data model unified and reduces reliance on manual spreadsheets.

Conclusion

Performance obligation asc 606 accounting works best when it is treated as a system, not a year-end exercise. The five-step model gives every function the same vocabulary. The recurring judgment calls around timing, contract type, and bundling determine whether revenue reporting holds up under audit. CFOs who build performance obligation accounting into contract review, system integration, and training tend to avoid costly restatements. This standard rewards teams that document their logic clearly enough for an outside reviewer to follow it without guesswork.

Disclaimer: This blog is intended for informational purposes only and does not constitute legal, tax, or accounting advice. You should consult your own tax advisor or counsel for advice tailored to your specific situation.

Hindol Datta is a seasoned finance executive with over 25 years of leadership experience across SaaS, cybersecurity, logistics, and digital marketing industries. He has served as CFO and VP of Finance in both public and private companies, leading $120M+ in fundraising and $150M+ in M&A transactions while driving predictive analytics and ERP transformations. Known for blending strategic foresight with operational discipline, he builds high-performing global finance organizations that enable scalable growth and data-driven decision-making.

AI-assisted insights, supplemented by 25 years of finance leadership experience.