Executive Summary

Venture debt is frequently described as non-dilutive capital, and in the strictest technical sense, that description holds. No new equity is issued at closing. But the full picture is more nuanced. Embedded within most venture debt agreements is a mechanism that quietly reserves a claim on future equity: the warrant. For founders and CFOs navigating growth-stage financing, understanding venture debt warrants is not a secondary consideration. It is central to evaluating whether the capital is as efficient as it appears. This article examines how lenders structure warrants, how they price them, what they cost in real exit scenarios, and how to negotiate them intelligently. It draws on direct operating experience across SaaS, cybersecurity, gaming, and logistics environments where capital structure decisions carried material consequences. The goal is not to discourage venture debt. It is to ensure that those who use it do so with complete visibility into what they are giving up, and when it matters most.

The Non-Dilutive Myth and the Warrant Reality

Venture debt has earned a reputation as the founder-friendly alternative to equity. Raise capital without giving up ownership. Extend runway without resetting valuation. In principle, the appeal is rational. In practice, the story carries a footnote that does not always receive the attention it deserves. That footnote is the warrant.

Almost every venture debt facility includes a warrant package. It is the mechanism through which lenders participate in the upside of a company they have bet on with fixed-rate capital. Unlike a venture capitalist, a debt lender does not own equity in the company at closing. The interest rate and fees represent their base return. But lenders are sophisticated enough to know that the companies most likely to repay are also the companies most likely to generate significant equity value. Warrants allow them to capture a portion of that value without taking the same risk profile as an equity investor.

For the founder or CFO reviewing a term sheet, this requires careful attention. The interest rate is visible. The origination fee is visible. The warrant, expressed as a percentage of the loan amount, can appear modest on the page. What is less visible is what that warrant becomes when the company exits at a meaningful multiple.

Understanding how this instrument works, how lenders price it, how venture debt warrant coverage varies across different deal types, and how to negotiate it effectively is among the most practically valuable competencies a growth-stage finance leader can develop.

How Venture Debt Warrants Are Structured

The Basic Mechanics

A warrant is a call option. It gives the lender the right, but not the obligation, to purchase a specified number of shares in the company at a fixed price, typically the price per share from the most recent equity financing round. The lender does not have to exercise the warrant. But if the company grows in value, exercising becomes highly attractive.

The warrant is defined by three variables: the coverage percentage, the share price, and the number of implied shares. Each of these determines what the lender ultimately receives.

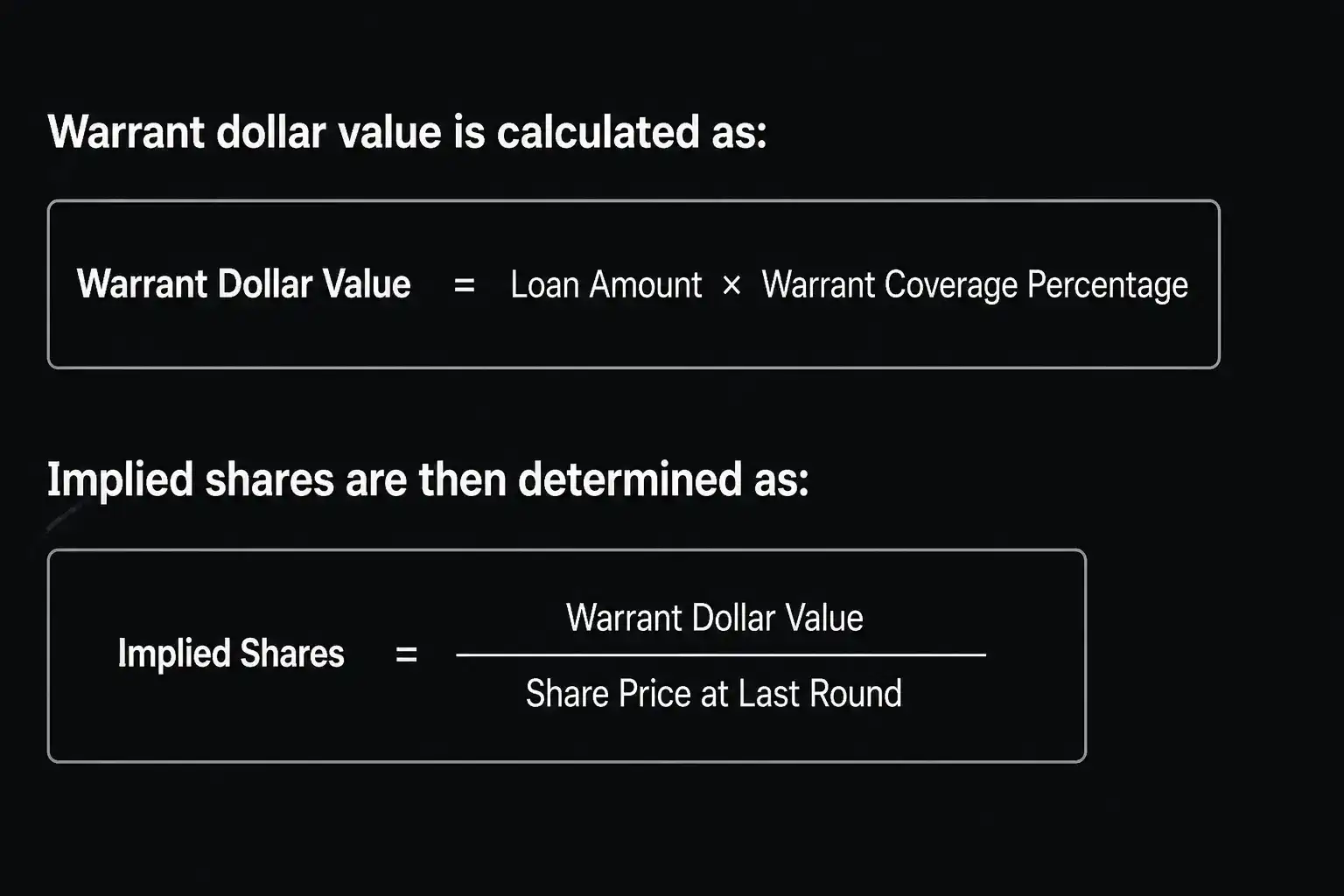

To anchor this in a concrete example: a company raises a Series B at a post-money valuation of one hundred million dollars. The price per share is five dollars. The company takes on four million dollars in venture debt with ten percent warrant coverage.

Warrant Dollar Value = $4,000,000 × 10% = $400,000

Implied Shares = $400,000 / $5.00 = 80,000 shares

At closing, those eighty thousand shares appear modest. But their true cost only becomes clear at exit.

The Exit Multiplier Effect

Suppose the company exits four years later at four hundred million dollars, implying a share price of twenty dollars. The lender, holding eighty thousand shares, now has a warrant worth:

Warrant Value at Exit = 80,000 × $20.00 = $1,600,000

The lender earned one million six hundred thousand dollars in equity value from a four-hundred-thousand-dollar warrant, in addition to the interest and fees already collected. The founder gave up that value without realizing it at the time of signing.

This is the exit multiplier effect, and it is the central reason venture debt warrant coverage demands rigorous modeling before any term sheet is accepted.

Venture Debt Warrant Coverage Across Deal Types

Warrant coverage is not uniform. It varies by stage, lender, loan size, and negotiating leverage. Understanding the range across deal types allows CFOs to benchmark what they are being offered against market norms.

| Deal Type | Typical Warrant Coverage | Interest Rate Range | Key Characteristic |

| Series A term loan | 10%–15% | 9%–12% | Higher coverage offsets early-stage risk |

| Series B term loan | 8%–12% | 8%–11% | Moderate coverage, milestone-based draws |

| Series C / growth debt | 5%–10% | 7%–10% | Lower coverage reflects stronger credit profile |

| Equipment financing | 0%–5% | 6%–9% | Asset-backed, minimal equity component |

| Revenue-based facility | 0% | Variable | No warrants; repayment tied to revenue percentage |

| A/R revolving line | 0%–3% | 7%–10% | Receivables-secured, low equity exposure |

The pattern is consistent: the earlier the stage and the higher the perceived risk, the greater the warrant coverage demanded by the lender. As the company matures and the credit profile strengthens, negotiating power shifts. A Series C company with fifteen million dollars in ARR and ninety percent logo retention is in a meaningfully different position than a Series A company with two million dollars in annual recurring revenue and a short operating history.

Having overseen more than one hundred million dollars in acquisitions during my tenure at a gaming enterprise, and having led capital raises exceeding one hundred and twenty million dollars across multiple sectors, one pattern holds consistently: the companies that negotiate the best warrant terms are those that arrive at the conversation with clean financials, strong investor backing, and a clearly articulated repayment path.

The True Cost of Warrants: A Scenario Model

Building the Full Cost Picture

CFOs evaluating venture debt must model the total cost of capital, not just the stated interest rate. The true cost includes interest payments, origination and backend fees, and the equity value surrendered through warrants. Only when all three are visible can a genuine comparison with equity financing be made.

Consider a Series B company deciding between raising three million dollars in equity at a one-hundred-million-dollar post-money valuation, or taking three million dollars in venture debt with ten percent interest, a two percent origination fee, a four percent backend fee, and ten percent warrant coverage.

The equity scenario cost the founder three percent ownership worth three million dollars at a one-hundred-million-dollar valuation. In a two-hundred-million-dollar exit, that three percent represents six million dollars. In a four-hundred-million-dollar exit, it represents twelve million dollars.

The debt scenario costs less in a successful exit than the equity alternative, provided the company performs well enough to service the debt. But the key variable is the exit multiple. The higher the exit, the more the warrant costs in absolute terms, even as it remains less dilutive than equity.

This is the fundamental trade-off. Venture debt warrants cost less than equity in percentage terms, but their dollar value rises with success. Founders who expect significant exits must model warrant costs at multiple exit scenarios before accepting coverage terms.

Negotiating Warrant Terms: Where Leverage Lives

What Is Negotiable

Most founders treat the warrant coverage percentage as a fixed input on the term sheet. It is not. It is a starting position. Lenders structure warrant coverage to achieve a target blended internal rate of return across their portfolio. If a founder can offer something else that improves that return profile, coverage is negotiable. The most effective negotiation levers are:

- Higher interest rate in exchange for lower warrant coverage. A lender indifferent between ten percent interest with ten percent warrants and eleven percent interest with five percent warrants can be approached on that basis. For a founder expecting a large exit, paying more in interest to reduce the equity give-up is often the better trade.

- Shorter loan term in exchange for lower coverage. A three-year loan with lower warrant coverage may serve a founder better than a four-year loan with standard coverage, particularly if the company expects to refinance or exit within thirty-six months.

- Capping the warrant at a valuation ceiling. Some deals include a cap on the per-share price at which warrants can be exercised, limiting the lender’s upside in very high-exit scenarios.

- Net settlement provisions. Rather than requiring the lender to pay cash to exercise warrants, a net settlement allows the lender to receive the net value in shares. This simplifies the mechanics but does not reduce the dilution.

- Removing warrants entirely in exchange for a backend fee. Some lenders will accept an end-of-term fee, typically three to five percent of the loan principal, in lieu of warrant coverage. For companies projecting modest exits, this may be the more economical choice. For companies expecting large exits, eliminating the warrant and paying the backend fee is almost always advantageous.

Modeling the Trade-Off Before You Negotiate

No warrant term should be accepted without a scenario model showing what it costs at the expected exit, the downside exit, and the stretch exit. During my time scaling a digital marketing firm from nine million to one hundred and eighty million dollars in revenue, the discipline of modeling capital costs at multiple growth scenarios before committing to any instrument shaped every financing decision. The same discipline applies here. A seemingly modest coverage percentage at a one-hundred-million-dollar valuation looks materially different at a four-hundred-million-dollar exit. Build the model first. Then negotiate.

Benchmarking Your Offer

Before negotiating, a CFO should benchmark the term sheet against market norms for their stage and sector. The table below provides reference ranges:

| Negotiation Lever | Founder-Favorable | Market Standard | Lender-Favorable |

| Warrant coverage | 5% or below | 8%–10% | 12%–15% |

| Exercise price | Last round price | Last round price | Discounted price |

| Warrant term | 5 years | 7–10 years | 10 years |

| Net settlement | Available | Negotiable | Cash exercise only |

| Backend fee in lieu | Yes, 2%–3% | 3%–4% | Not offered |

Arriving at a negotiation with this framework in hand, combined with a clean financial model and strong investor backing, creates the conditions for a materially better outcome.

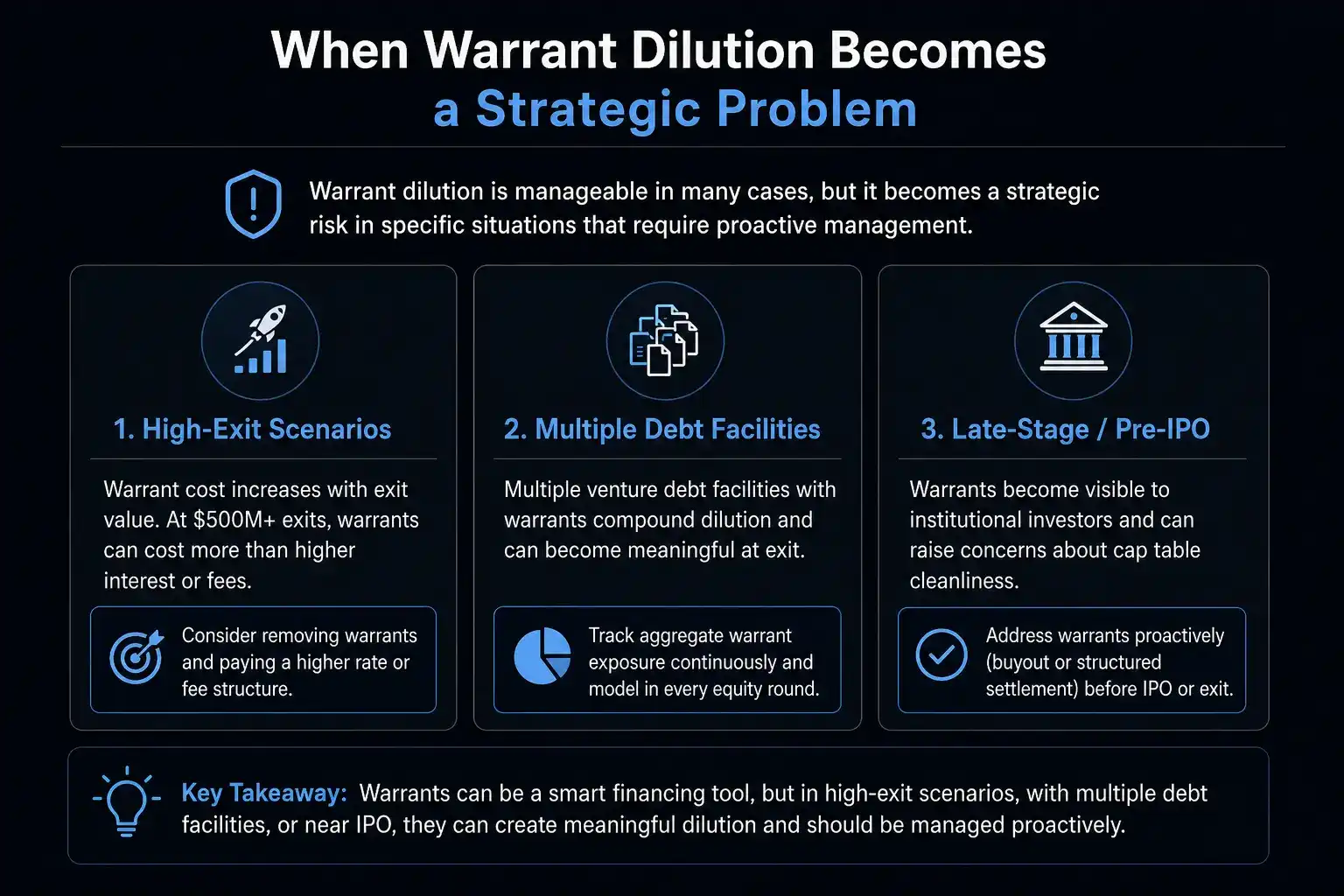

When Warrant Dilution Becomes a Strategic Problem

Not every venture debt arrangement creates problematic warrant dilution. In many cases, the equity given up through warrants is immaterial relative to the dilution avoided by not raising equity. But there are specific scenarios where warrant dilution deserves particular scrutiny.

High-Exit Scenarios

The warrant cost rises with exit value. A founder who expects to build a company worth five hundred million dollars or more is giving up substantially more through warrants than a founder who expects a one-hundred-million-dollar outcome. In high-exit scenarios, removing warrants entirely and paying a higher interest rate or backend fee is almost always the superior economic choice.

Multiple Debt Facilities

Some companies take on venture debt at multiple stages, each with its own warrant package. The cumulative dilution from three separate facilities, each with ten percent coverage on loans of varying sizes, can become meaningful at exit. A CFO managing a company through several debt raises should track aggregate warrant exposure on a running basis and include it in cap table modeling for each new equity round.

Late-Stage Pre-IPO Environments

At the growth and pre-IPO stage, warrant dilution becomes visible to institutional investors reviewing the cap table. Lender warrants sitting alongside preferred equity can raise questions about the cleanliness of the capitalization structure. Companies preparing for an IPO or a significant acquisition should model the impact of outstanding warrants on fully diluted share counts and address them proactively, either through buyout or structured settlement, before entering those processes.

Integrating Warrant Analysis into Capital Strategy

The most effective use of venture debt warrants as a capital strategy tool requires treating them not as an afterthought to the term sheet, but as a variable in the broader capital plan. That means:

- Modeling warrant costs at multiple exit scenarios before accepting any coverage percentage

- Including aggregate warrant exposure in cap table presentations to existing and prospective equity investors

- Tracking warrant expiry dates and monitoring whether buyout or settlement makes economic sense as the company matures

- Revisiting warrant terms at each refinancing opportunity, particularly when a stronger credit profile justifies renegotiation

Having led finance at a mission-driven education institution through a forty-eight million dollar capital raise, and having managed debt and equity capital structures across gaming, logistics, and cybersecurity organizations, the consistent lesson is that the cost of capital is never fully visible on the face of the term sheet. The warrant is the most common source of that hidden cost in venture debt. Understanding it with precision, modeling it with discipline, and negotiating it with confidence is what separates finance leaders who use debt strategically from those who simply use it.

Conclusion

Venture debt warrants are neither predatory nor inherently problematic. They are a rational mechanism through which lenders participate in the upside of companies they support with fixed-rate capital. But their cost is non-linear, rising with the company’s success in ways that are easy to underestimate at signing and impossible to ignore at exit. The CFO or founder who evaluates venture debt solely on its interest rate is working with an incomplete picture. The complete picture includes the warrant coverage percentage, the implied share count, the exercise price, the warrant term, and the projected value of those shares across a range of exit scenarios. When that picture is fully assembled, the decision to accept, negotiate, or decline a warrant package becomes a strategic choice rather than a procedural one. Debt, used with that level of clarity, becomes precisely what it promises to be: a tool for extending runway, preserving equity, and accelerating the path to value without surrendering more of that value than necessary.

Disclaimer: This blog is intended for informational purposes only and does not constitute legal, tax, or accounting advice. You should consult your own tax advisor or counsel for advice tailored to your specific situation.

Hindol Datta is a seasoned finance executive with over 25 years of leadership experience across SaaS, cybersecurity, logistics, and digital marketing industries. He has served as CFO and VP of Finance in both public and private companies, leading $120M+ in fundraising and $150M+ in M&A transactions while driving predictive analytics and ERP transformations. Known for blending strategic foresight with operational discipline, he builds high-performing global finance organizations that enable scalable growth and data-driven decision-making.

AI-assisted insights, supplemented by 25 years of finance leadership experience.