Executive Summary

Private equity cash flow management is among the most demanding disciplines in modern finance leadership. When a leveraged buyout closes, the spreadsheet optimism of the deal room gives way to the unrelenting arithmetic of debt service, covenant compliance, and working capital pressure. The business does not change overnight, but the consequences of every operating decision multiply. For the CFO stepping into a post-LBO environment, the job is not to challenge the capital structure. It is to make it work. This article draws on direct operating experience inside a leveraged wholesale distribution business to examine how debt reshapes company rhythm, how covenant pressure demands a new kind of financial discipline, and how leadership teams can build the systems and culture required to survive, stabilize, and ultimately grow. The lessons are applicable across any sector where leverage is a feature of the ownership model, not an anomaly.

When the Deal Closes and Reality Begins

There is a moment every operator inside a private equity-owned business eventually encounters. It arrives not in the boardroom during closing, but quietly, in the middle of a late-night cash flow review, when the gap between model assumptions and operating reality becomes impossible to ignore. Debt, in that moment, stops being a capital structure concept and becomes a daily constraint. I have lived that moment. It is formative in ways that no finance textbook fully prepares you for.

The logic of leverage is intellectually sound. Acquire a business using a combination of equity and debt, improve its operations, and generate returns on a relatively small equity base. If the company produces sufficient cash flow to service its obligations while continuing to grow, the outcome benefits all parties. The difficulty arises not in the theory but in the translation. Every investment thesis rests on a version of the business that is cleaner, more predictable, and more responsive than the one that actually operates.

Early in my career, I stepped into a finance leadership role at a regional wholesale distribution company shortly after its acquisition in a leveraged buyout. The business had respectable EBITDA, a loyal customer base, and reasonable margins. The deal had been structured with senior debt, a mezzanine tranche, and a revolving credit facility. The model projected EBITDA improvement within six quarters through SG&A reductions and top-line growth from regional expansion. The bankers were satisfied. The sponsor was confident. The investment committee had approved.

What the model had not fully accounted for was the working capital cycle. The business was seasonal. Collections were irregular. Inventory turnover lagged projections. Customer behavior had shifted toward smaller, more frequent orders, compressing operating leverage and increasing logistics pressure. The debt service schedule, however, was fixed. And that fixedness changed everything.

When Leverage Changes the Operating Rhythm

Debt does not simply alter the balance sheet. It alters the rhythm of a company. Forecasting tightens. Every growth initiative must pass two tests simultaneously: is it accretive, and is it cash-flow neutral in the near term? Those two conditions frequently conflict. And when they conflict, strategic intent begins to drift under the weight of liquidity management.

From the first week, the pressure was evident. The private equity sponsor required monthly reporting with tight variance analysis. Lenders required quarterly covenant compliance audits. A single missed threshold could trigger a technical default or force a difficult waiver conversation. Ordinary operating realities, a customer delaying payment, a shipment held at port, a vendor changing terms, carried consequences that multiplied under the weight of leverage.

My first task was not to optimize capital. It was to understand where it was leaking. That meant building weekly cash dashboards, mapping inflows against accounts receivable aging, and reconciling invoice cycles with vendor payment windows. It meant explaining to line managers why the leadership team had frozen approved projects, why the business had paused hiring plans, and why vendor negotiations now required executive attention. To them, the business was doing what it always had done. But the capital structure had redrawn the boundaries of what was permissible.

This is the fundamental dissonance of the post-LBO environment. The operating team inherits a business that looks familiar but operates inside a new set of constraints. The CFO’s role is to hold both realities simultaneously: the mission-driven narrative that sustains the workforce, and the financial architecture that governs every material decision.

Covenant Management as a Operating Discipline

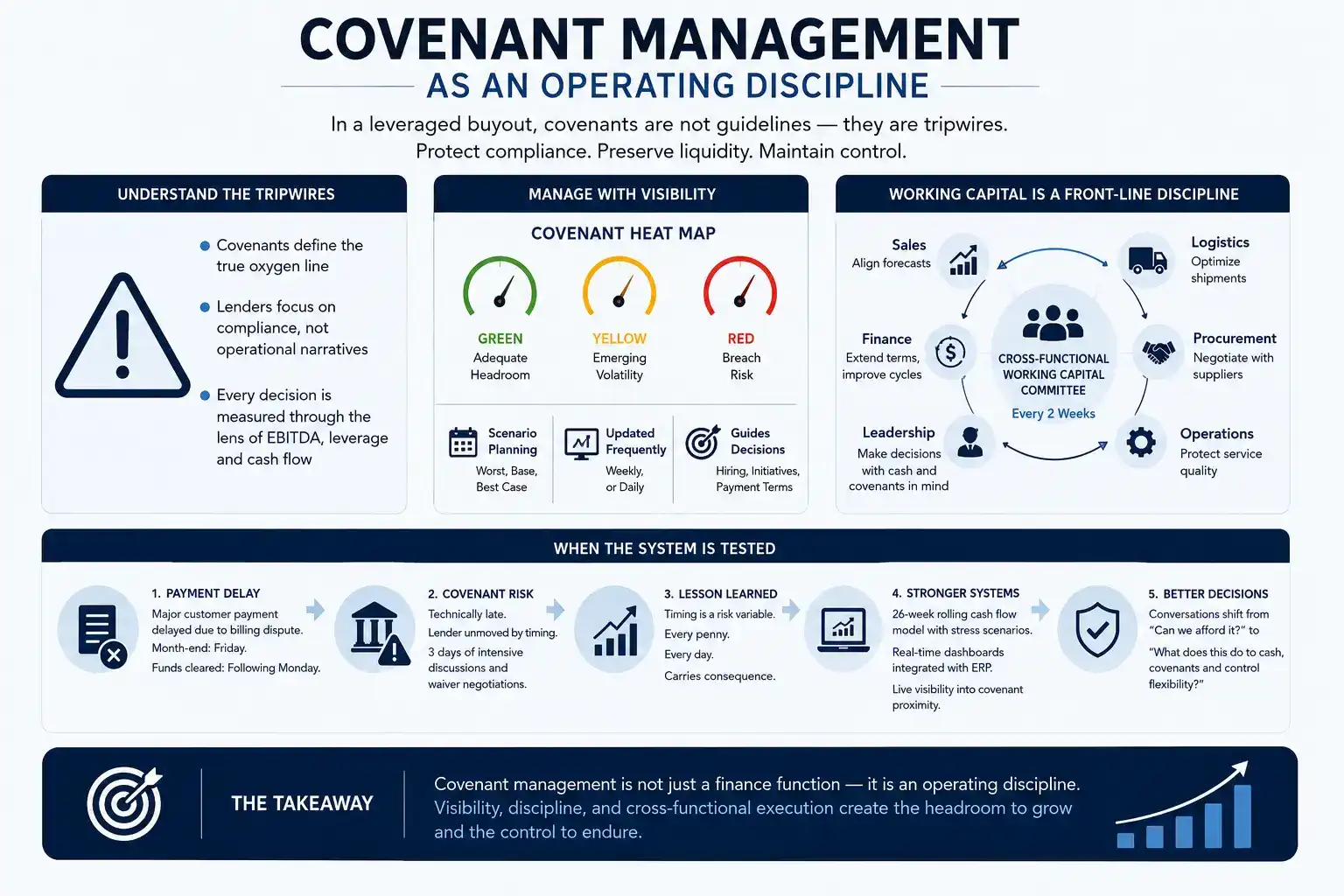

Understanding the Tripwires

In a leveraged environment, the margin for error is not strategic. It is contractual. Most finance professionals think in terms of budget variances and burn rate when assessing company health. Under a leveraged buyout, the true oxygen line is defined by covenants. These financial benchmarks are not guidelines. They are tripwires. Breach a leverage ratio or fall below a fixed charge coverage threshold, and a routine operating review transforms into a liquidity crisis conversation.

At the wholesale distribution company, covenants were tested quarterly, and each review carried the weight of a regulatory audit. The lender group was not interested in product innovation or workforce sentiment. They were focused on compliance. Every capital expenditure was evaluated not only for return on investment but for its impact on EBITDA calculations and leverage thresholds. The financial system became the primary lens through which all operating decisions were assessed.

The first structural response was to build what I came to call a covenant heat map. Every quarter, we modeled worst-case, base-case, and best-case scenarios across revenue, margins, and working capital flows. Each scenario fed into our debt service model and covenant dashboard. Color-coded alerts flagged pressure points: green for adequate headroom, yellow for emerging volatility, red for breach risk. These dashboards were updated weekly and, during periods of collection slowdowns or logistics cost spikes, daily. They became tools for operational negotiation, informing hiring decisions, initiative prioritization, and payment term strategies.

The Working Capital Imperative

Working capital management, in this context, was not a finance function. It was a front-line discipline. We restructured procurement approvals, shifted inventory purchasing closer to demand signals, and negotiated partial shipments with key suppliers. A supplier scorecard was introduced that ranked vendors not only by unit cost but by cash impact, payment flexibility, and reliability under compressed timelines.

A cross-functional working capital committee met every two weeks. The mandate was straightforward: unlock cash without compromising service quality. Sales aligned order forecasts. Logistics optimized shipping batches. Finance drove term extensions with key suppliers. Each function had a defined role in the liquidity equation.

One of the most impactful changes was a shift in invoicing timing. Moving from end-of-month billing to rolling terms reduced average days sales outstanding by nearly eight days. That change, unremarkable on a slide deck, created meaningful headroom in the revolving credit facility during a tight payroll month. These were not the synergies in the investment thesis. But they were the operational breakthroughs that changed the tempo of survival.

The following table illustrates how working capital levers translated into cash impact across the key operational areas we managed:

| Working Capital Lever | Action Taken | Cash Impact |

| Invoicing cycle | Shifted to rolling terms from month-end | Reduced DSO by ~8 days |

| Inventory purchasing | Aligned orders to demand signals | Reduced carrying costs |

| Supplier terms | Negotiated extensions with key vendors | Improved payables cycle |

| Customer incentives | Rewarded early payment | Accelerated collections |

| Procurement approvals | Restructured authorization thresholds | Reduced unauthorized spend |

| Shipping optimization | Consolidated logistics batches | Lowered per-unit freight cost |

When the System Is Tested

Despite these disciplines, there were quarters when covenant compliance came within a narrow margin. One instance remains particularly instructive. A significant customer delayed a seven-figure payment due to a billing dispute. Month-end fell on a Friday. The wire did not clear until the following Monday. Technically, the funds had left the customer’s account. Operationally, they had not arrived in ours. The lender was unmoved by the timing distinction. Three days of intensive conversations with legal and treasury followed, culminating in a waiver discussion and a complete rebuild of near-term projections under forensic scrutiny.

The emotional cost of those days was considerable. The operational lesson was sharper still. In leveraged finance, timing is not a detail. It is a risk variable. Every penny, and every day, carries consequence.

That quarter accelerated reforms that had been discussed but not yet implemented. We extended our cash flow model from a thirteen-week to a rolling twenty-six-week horizon with embedded stress scenarios. Real-time variance dashboards were integrated with the ERP system, giving the leadership team live visibility into cash position in context, not as an abstract line item but as a live indicator of covenant proximity. The nature of operating conversations changed. The question was no longer whether the company could afford a decision. It became what that decision would do to cash, covenants, and control flexibility.

Building Systems and Culture for the Long Term

From Firefighting to Planning

By the third year under the leveraged structure, the company had changed in its internal architecture in ways that were not visible on an organizational chart. Cash forecasts had replaced wish lists. Vendor meetings opened with receivables schedules. Capital allocation was a structured conversation with a defined framework, not an emotional negotiation driven by urgency.

Central to this evolution was the development of a free cash flow waterfall model. This tool traced EBITDA through interest expense, debt repayment, maintenance capital expenditure, and working capital movements to arrive at true free cash flow, the cash that remained after all obligations had been met. This was not a board deck metric. It was a biweekly executive review instrument. Every material decision, a new hire, a technology investment, a sales incentive program, was mapped against its impact on the waterfall before approval. If the free cash flow impact was negative without a clear and time-bound path to recovery, the decision was deferred.

This discipline did not slow the business. It made the business deliberate. There is a meaningful difference. Slow implies hesitation. Deliberate implies clarity. The team began to understand that deferral was not defeat. It was sequencing.

Leadership, Transparency, and Cultural Alignment

A pivotal structural decision during this period was a change in operating leadership. The founder, who had built the business through relationship-driven, intuition-based management, was not equipped for the covenant-governed, data-intensive demands of the post-LBO environment. The board made the difficult choice to bring in a new chief executive who had navigated a similar leveraged buyout cycle. I remained as CFO and served as the connective tissue between the institutional memory of the original business and the operational demands of the new structure.

The incoming chief executive brought a guiding philosophy that proved transformative: transparency breeds alignment. A monthly company-wide forum was introduced where business performance was reviewed openly, cash-positive decisions were recognized, and mid-level managers were educated on the mechanics of leverage and covenant compliance. A shared dashboard, visible to all directors, displayed not only revenue and gross margin but cash conversion cycles, accounts receivable aging, and debt service coverage ratios.

The effect was twofold. It forced discipline across every level of the organization. And it empowered teams to innovate within clearly defined guardrails. Logistics began negotiating batch discounts with carriers. Sales began tracking not only volume but collection velocity. The culture shifted from execution toward ownership. People began to understand that their decisions had a cash consequence, and that consequence mattered at the covenant level.

Having led a nonprofit through a forty-eight million dollar capital raise, I had learned that financial transparency, when communicated with clarity and purpose, does not create anxiety. It creates accountability. That lesson translated directly into the leveraged operating environment. People who understand the financial stakes of their decisions make better decisions.

Rebuilding the Relationship with the Lender

Early in the post-acquisition period, the relationship with the lending group was a source of significant organizational stress. The lenders were perceived as enforcers rather than partners. Every covenant review felt adversarial. Every waiver request carried reputational weight.

Over time, through consistent performance and proactive communication, that dynamic evolved. We began sharing internal dashboards with the lending group a week before formal reviews. Key variances were pre-briefed with context and corrective action plans. We used formal meetings to problem-solve rather than present. The lending group, once a source of tension, became a structured partner in the business. Not an easy partner, and not a patient one. But a predictable one. And in leveraged environments, predictability is a form of safety.

This mirrors an experience from my time leading finance at a cybersecurity company, where the discipline of proactive, data-rich board communication was central to sustaining investor confidence through periods of operational complexity. The principle is consistent across contexts: stakeholders who receive information before they ask for it extend more trust than those who receive it under pressure.

Strategic Trade-offs Under Leverage

Managing a leveraged business does not mean refusing growth. It means sequencing it. During the stabilization period, we passed on a potential acquisition because the incremental leverage required would have compressed covenant headroom to an unacceptable level. We postponed a technology overhaul that carried a long payback period despite its operational merit. These were not decisions made without analysis or regret. They were made within a framework that prioritized the survivability of the enterprise over the ambition of the moment.

The CFO in a leveraged environment must function as both gatekeeper and translator. Gatekeeper in the sense of protecting the financial architecture from decisions that create short-term enthusiasm but long-term liquidity risk. Translator in the sense of helping operators understand that the capital structure is not an obstacle to the mission. It is the condition under which the mission must be pursued.

As I have reflected across my career spanning gaming, logistics, SaaS, cybersecurity, and digital marketing, the companies that navigate leverage most effectively are not those with the most favorable debt terms. They are those with the most financially literate operating cultures. When teams below the CFO level understand how their decisions affect free cash flow and covenant proximity, the entire organization becomes a risk management function.

Conclusion

Private equity cash flow management is, at its core, a leadership discipline as much as a financial one. The debt placed on a business at acquisition does not simply change the balance sheet. It changes the tempo of decision-making, the stakes of operational choices, and the demands placed on every function that touches cash. The CFO who navigates this environment well is not the one who resists the constraints of leverage but the one who builds systems, culture, and relationships capable of operating within them. Free cash flow becomes the north star. Covenant compliance becomes the floor. And transparency, both internal and external, becomes the most valuable currency in the organization. Leverage, when managed with discipline and clarity, is not a trap. It is a teacher. And the lessons it imparts, about sequencing, precision, and the true cost of opacity, are among the most enduring in a finance leader’s career.

Disclaimer: This blog is intended for informational purposes only and does not constitute legal, tax, or accounting advice. You should consult your own tax advisor or counsel for advice tailored to your specific situation.

Hindol Datta is a seasoned finance executive with over 25 years of leadership experience across SaaS, cybersecurity, logistics, and digital marketing industries. He has served as CFO and VP of Finance in both public and private companies, leading $120M+ in fundraising and $150M+ in M&A transactions while driving predictive analytics and ERP transformations. Known for blending strategic foresight with operational discipline, he builds high-performing global finance organizations that enable scalable growth and data-driven decision-making.

AI-assisted insights, supplemented by 25 years of finance leadership experience.