Executive Summary

A cap table records who owns a company. But it says nothing about what that ownership will actually deliver after tax. Many founders build meticulous ownership records while leaving the tax consequences of that same equity unexamined. The gap between the two often surfaces at the worst possible moment. That moment often arrives during a financing round, an acquisition, or an employee’s first liquidity event. This article draws on three decades of operational finance leadership. That leadership spans cybersecurity, SaaS, gaming, logistics, digital marketing, medical devices, and nonprofit sectors. It examines three recurring pitfalls.

The first is phantom income in pass-through entities. The second is options mispricing under Section 409A. The third is the false assumption that Qualified Small Business Stock exemptions apply automatically. Each pitfall shows why ownership and tax exposure must be reviewed together, not separately. Founders who treat the tax table as a strategic mirror to the cap table build companies. Those companies are genuinely investor ready.

Why the Cap Table Is Only Half the Story

Most founders can recite their ownership percentages from memory. They track dilution across financing rounds. They model option pools with precision. And they know exactly how a new investor will affect existing shareholders. A cap table, in this sense, becomes the founder’s most trusted document. It is the single source of truth for who owns what. It also shows how much they stand to gain. Yet ownership and economic reality are not the same thing. Few founders apply the same discipline to understanding their equity’s true worth. That worth becomes clear only once taxes are accounted for.

Across nearly three decades, I have served as an operational finance executive in venture-backed companies. Those companies span cybersecurity, software as a service, gaming, logistics, digital marketing, medical devices, and nonprofit education. I have come to see a consistent pattern. The businesses that scale cleanly raise capital efficiently. They also exit without last-minute surprises. These are the businesses where ownership records and tax exposure are reviewed together. They treat it as a single, connected discipline rather than two separate functions. When they fall out of step, the consequences tend to surface quietly. They surface in a K-1 statement, an audit letter, or a due diligence request. This happens long after the decisions that caused them were made.

This article examines three areas where that misalignment most often takes root. The first is phantom income in pass-through structures. The second is options that are priced without the rigor Section 409A requires. The third is the widespread assumption that the Qualified Small Business Stock exemption applies automatically. Each carries the potential to erode trust, distort incentives, and create liabilities that compound in silence.

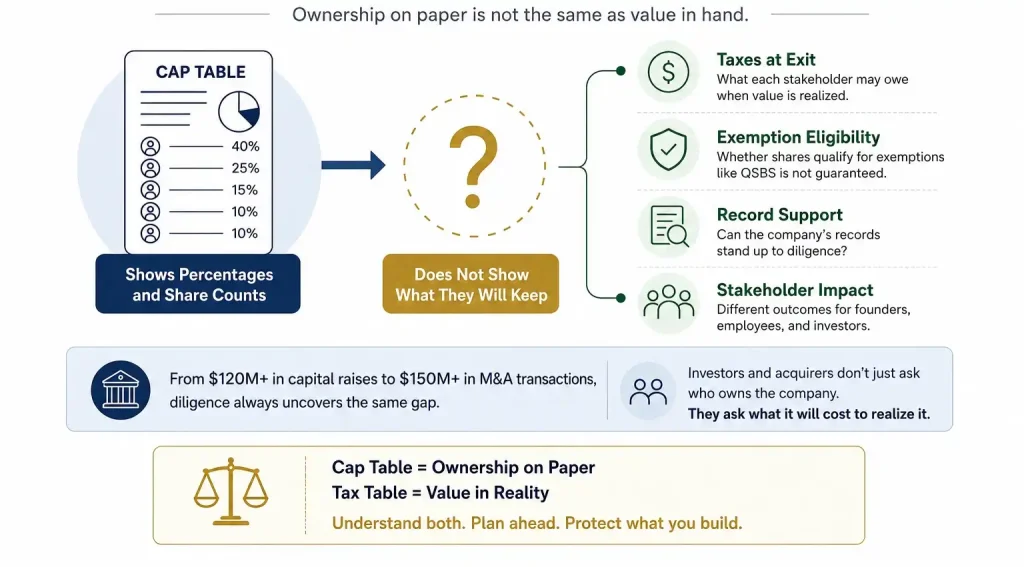

The Cap Table Tells You Who Owns What, Not What They Will Keep

Equity is often described as currency, and in an early-stage company it functions exactly that way. It recruits talent, aligns incentives, and rewards the people who take the earliest risk. But currency has a cost basis, and that cost basis is where many founders lose the thread. A capitalization table shows percentages and share counts. It does not show what an employee will owe the moment a taxable event occurs, nor does it show whether a founder’s shares will ultimately qualify for the exemptions everyone assumes they will receive.

In my experience working alongside founders during capital raises exceeding one hundred and twenty million dollars in aggregate and merger and acquisition transactions exceeding one hundred and fifty million dollars, the diligence process almost always exposes this gap. Investors and acquirers do not simply ask who owns the company. They ask what it will cost each stakeholder to realize that ownership, and whether the company’s records can support the answer.

Phantom Income: When Equity Creates a Tax Bill Before It Creates Wealth

Founders and employees tend to assume that equity only produces a tax consequence at exit. In pass-through entities such as LLCs and partnerships, that assumption is often false. Phantom income arises when a company allocates taxable profit to equity holders who have no corresponding ability to convert that allocation into cash. A K-1 can show income of two hundred thousand dollars to someone who took no salary and received no distribution, and the tax authority still expects payment.

How Phantom Income Emerges in Pass-Through Structures

This is one of the reasons venture investors generally steer companies toward C-Corp structures rather than pass-through entities. Incorporation mitigates the risk. But phantom income can still appear in subtler forms. It can appear through deferred compensation arrangements, early restricted stock unit issuances, or revenue-sharing agreements. These arrangements trigger recognition events without producing cash. A tax table is an internal record of potential exposure tied to each class of equity. It needs to be reviewed alongside the cap table. This helps founders understand what they are truly promising employees.

A Lesson From the Field

Early in my career advising a pass-through entity that had extended profit interests to senior engineers, the business began generating meaningful cash flow and those engineers received tax bills in the five figures on allocations they could not convert into liquidity. Two of them left the company shortly after. The equity had been generous on paper. In practice, it had created resentment rather than retention, and the company had not intended any of it.

Options Mispricing: A Quiet Threat to Trust and Compliance

Options remain the most common incentive tool in venture-backed companies, and they carry their own set of risks when priced incorrectly. The exercise price must reflect the fair market value of the underlying shares on the date of grant, typically established through a 409A appraisal. In a fast-growing company, a valuation that is only a few months old can already be stale, and delays in granting options can result in awards that are priced too low or too high.

The Role of 409A Valuations

Underpriced options can be treated as deferred compensation, subject to penalties under Section 409A. Overpriced options quietly erode employee morale, since the economic value they were meant to deliver shrinks before anyone notices. Poor recordkeeping around grant dates, board approvals, and vesting schedules compounds both problems, and few founders realize how closely acquirers examine this detail until diligence is already underway.

What Happens When Grants Fall Out of Compliance

Having reviewed cap tables where option grants were informally backdated, sometimes for administrative convenience and sometimes to align with a new hire’s start date, I have seen how quickly this becomes a liability. Without contemporaneous valuations or proper board approval, these grants fall outside compliance, and acquirers flag them during diligence. The remedy typically involves restating documents, refreshing valuations, and issuing gross-up payments to employees who would otherwise absorb an unexpected tax bill. A cap table that does not reflect accurate grant timing is not really a record of ownership. It is a work of fiction that a tax table will eventually correct.

The QSBS Illusion: An Exemption That Must Be Earned, Not Assumed

Few provisions in the tax code generate as much founder confidence as Section 1202, the Qualified Small Business Stock exemption. Under the right conditions, QSBS allows holders of eligible stock to exclude up to ten million dollars, or ten times their basis, in capital gains upon sale. It is one of the most powerful tools available to early-stage founders and investors, and it is also one of the most commonly assumed rather than confirmed.

The Eligibility Criteria Founders Often Overlook

Eligibility depends on several conditions that must all hold true, including the following.

- The company must be a domestic C-Corp engaged in a qualified trade or business.

- The stock must represent original issuance rather than a secondary purchase.

- The holder must retain the shares for a minimum of five years.

- The company’s gross assets must have remained under fifty million dollars at the time of issuance.

Certain service businesses, financial institutions, and licensing-heavy models can disqualify a company entirely, and instruments such as convertible notes, SAFEs, or option exercises require careful analysis to confirm they satisfy the original issuance requirement.

Why QSBS Status Is Dynamic, Not Fixed

I once advised a founder who, after seven years of building the business, sold the company for forty two million dollars, fully expecting the proceeds to qualify for the QSBS exclusion. On closer review, the company’s activities had gradually shifted into disqualified territory through a strategic pivot made years earlier. The tax impact was significant, amounting to millions of dollars in capital gains that had not been anticipated. The founder had not been misinformed. The company had simply changed, and no one had checked whether the exemption had changed along with it.

QSBS eligibility should be monitored as a condition that evolves with the business, not a box that gets checked once at formation. Founders should document issuance dates, retain valuation reports, and track any shift in business activity that could affect qualification, particularly in the years leading up to a planned exit.

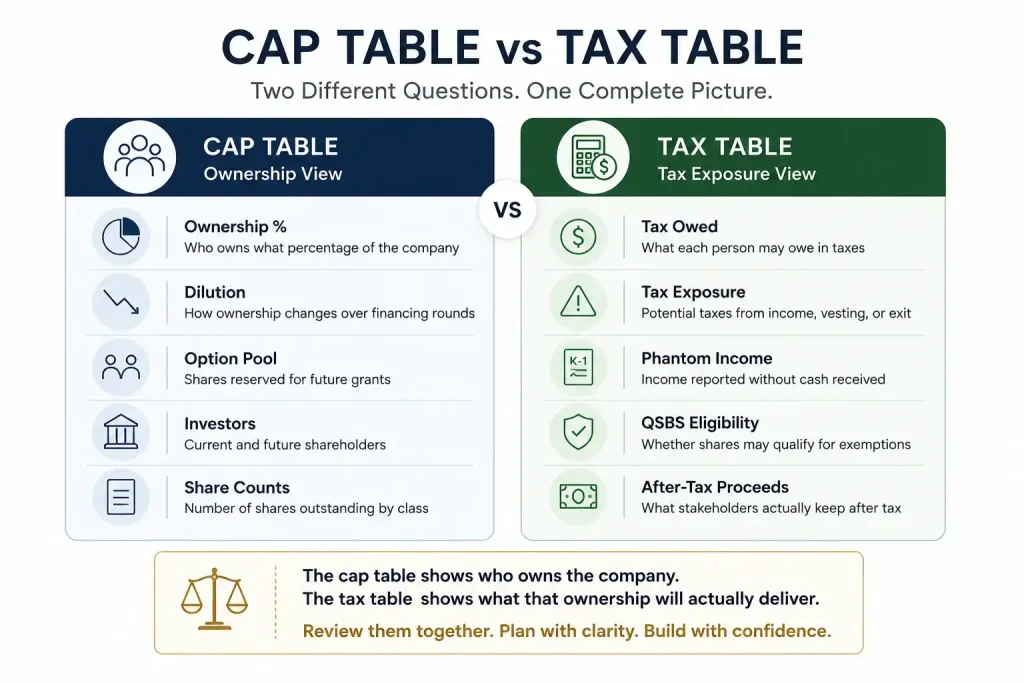

Building a Cap Table Startup Founders Can Trust

A well-maintained cap table is only half the picture. The other half is whether the equity it represents will deliver after-tax value to the people who hold it. When reviewing capitalization records during diligence, the question I return to is simple: what is the tax cost of realizing this ownership. If no one at the table can answer that question with confidence, the equity is not yet real in any meaningful sense.

Practices That Keep Ownership and Tax Realities Aligned

Founders who avoid these pitfalls tend to share a few habits in common.

- Reviewing 409A valuations on a regular cadence, particularly during periods of rapid growth or before major grant cycles.

- Educating employees on the tax implications of their equity well before a liquidity event arrives.

- Involving tax counsel early in major corporate actions, including financings, pivots, and acquisitions.

- Treating the tax table as a living document that is updated alongside every cap table change, not reconstructed after the fact.

These practices are not complicated, but they require the same discipline founders already apply to fundraising and product strategy. In my work leading finance transformations across sectors as varied as gaming, logistics, and medical devices, the companies that built this discipline early were consistently the ones that closed transactions faster and retained employee trust through the process.

Conclusion

A cap table is the story a company tells about ownership. A tax table is the fine print that determines whether that story holds up. Founders who treat the two as separate exercises discover the gap between them at the worst possible time, during a financing round, an acquisition, or an employee’s first taxable event. Founders who treat them as a single discipline build something more durable. Across three decades leading finance functions through capital raises, mergers, and rapid scaling across cybersecurity, gaming, and nonprofit education, this pattern has held. Clean ownership records paired with clear tax exposure let a company move quickly when opportunity arrives, whether a new investor, an acquirer, or an employee converting equity into real value. The tax table is not a compliance afterthought. It is a strategic mirror to the cap table, and founders who understand this early keep the pen in their own hand.

Disclaimer: This blog is intended for informational purposes only and does not constitute legal, tax, or accounting advice. You should consult your own tax advisor or counsel for advice tailored to your specific situation.

Hindol Datta is a seasoned finance executive with over 25 years of leadership experience across SaaS, cybersecurity, logistics, and digital marketing industries. He has served as CFO and VP of Finance in both public and private companies, leading $120M+ in fundraising and $150M+ in M&A transactions while driving predictive analytics and ERP transformations. Known for blending strategic foresight with operational discipline, he builds high-performing global finance organizations that enable scalable growth and data-driven decision-making.

AI-assisted insights, supplemented by 25 years of finance leadership experience.