Executive Summary

Venture capitalists face few decisions harder than choosing whether to keep funding a struggling portfolio company or to let it go. This article examines how the best investors separate conviction from sunk cost, narrative from data, and hope from probability. It explores the quantitative signals that guide these calls, including runway, churn, and burn multiples, along with intangible factors that often matter more, such as founder coachability and team resilience. The article also looks at how leading firms institutionalize triage through structured frameworks, red team reviews, and pre-mortems, reducing the influence of loss aversion and narrative inertia, and considers the human side of these decisions, from managing founder relationships with dignity to maintaining trust with limited partners. The conclusion is simple. The willingness to let go, done with clarity and respect, is often what separates firms that survive from those that thrive.

The Moment Conviction Meets Capital

Every venture investment begins with a measure of romance. The team looks exceptional, the product feels timely, and the market appears large enough to justify almost any outcome. As cycles unfold, that early certainty fades. Growth slows, the next funding round becomes harder to close, and boardroom conversations shift from strategy to survival. At that point, venture capitalists face a question that is part financial and part personal: continue supporting the company, or redirect attention and capital elsewhere.

This is rarely a clean binary. Few companies are obviously beyond saving, and few are obviously thriving without complication. Most sit in a middle band, somewhere between stalled and salvageable, and this middle band consumes a disproportionate share of investor attention. The tools used to evaluate these companies combine hard data with softer signals that resist easy measurement. The hard data includes runway, churn, customer acquisition costs relative to lifetime value, and burn multiples. The softer signals include a founder’s coachability, the loyalty of early customers, and how quickly a team adapts after a setback.

This challenge is not unique to formal venture funds. Anyone responsible for capital across a portfolio of initiatives, whether inside a corporate finance function or a strategic business unit, eventually faces a similar dilemma. A division that once held real promise loses its market position. An internal initiative overextends just as conditions shift. In each case, the core task is the same. It involves assessing signal from noise under genuine uncertainty, in a way that holds up under later scrutiny rather than simply feeling right in the moment.

Sunk Cost Versus Option Value

One of the more persistent traps in this process is the tension between sunk cost and option value. A prior investment, especially one made at a high valuation or championed internally, creates psychological lock-in. No one wants to be the partner who gives up on a deal others believed in. Yet every additional dollar invested in a struggling company is not recovering what has already been spent. It is purchasing a new probability of a different outcome. The stronger frameworks isolate this by running scenario analysis. They ask what credible paths exist toward an up round, an acquisition, or breakeven, and how realistic those paths are based on experience rather than founder optimism.

Committee-based decision making can complicate this further. Consensus is often prized in venture firms, but consensus has a cost. It frequently produces partial support, where a company receives a smaller round and a trimmed team, but the thesis stays technically intact. No one fully commits to either a real bet or a clean exit. Compromise, not analysis, keeps many companies alive, slowly draining capital and attention that could go toward higher-conviction opportunities.

Building Structure Around a Subjective Decision

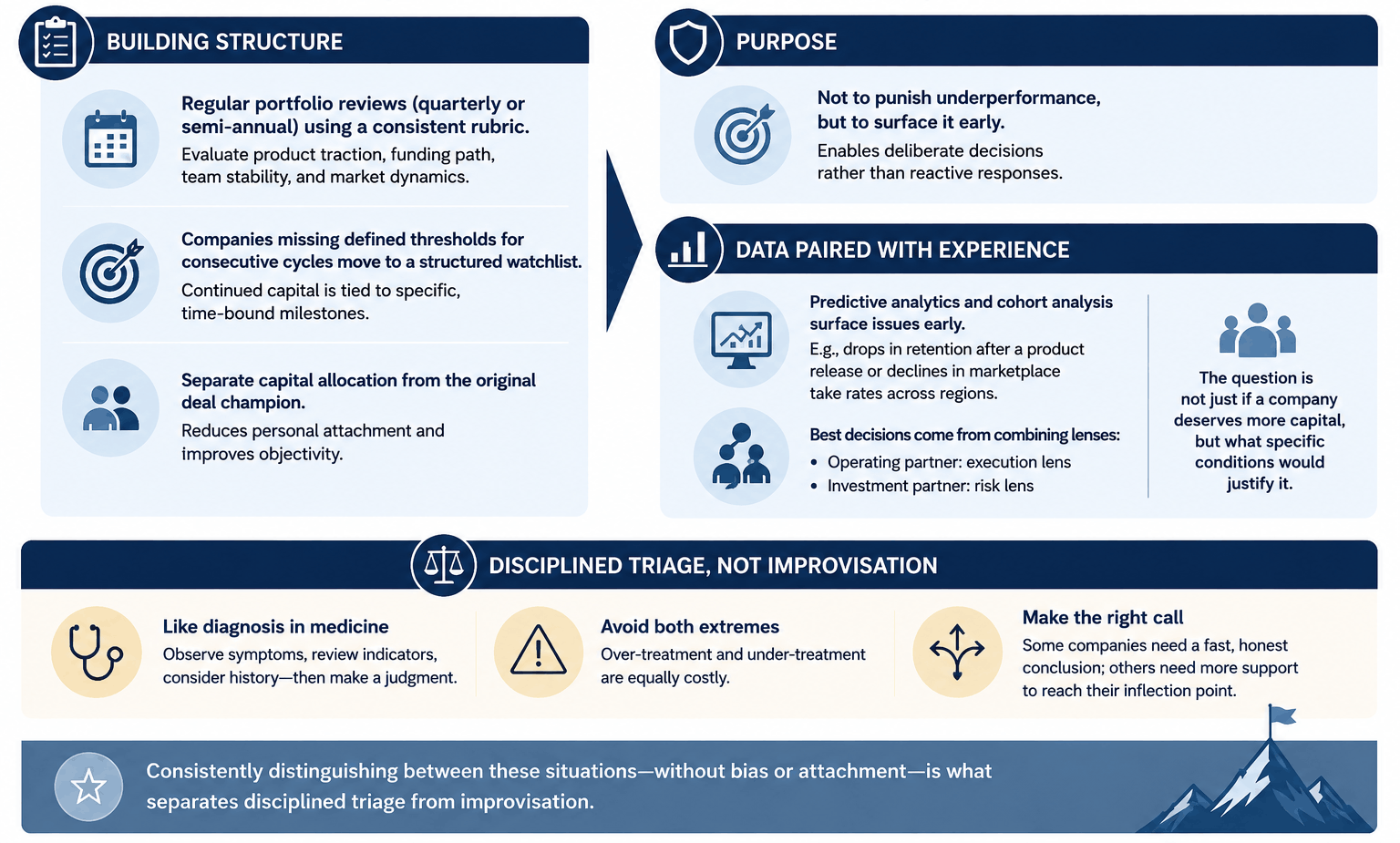

Recognizing this risk, some firms have moved toward more disciplined frameworks rather than relying purely on partner instinct.

- A quarterly or semi-annual portfolio review evaluates each company against a consistent rubric covering product traction, funding path, team stability, and market dynamics.

- Companies that miss defined thresholds for consecutive cycles move into a structured watchlist, where specific, time-bound milestones govern continued capital rather than open-ended support.

- Separating capital allocation decisions from the original deal champion reduces the influence of personal attachment on whether a company continues to receive funding.

These mechanisms exist less to punish underperformance and more to surface it early enough that venture capitalists can respond deliberately rather than reactively. The goal is not to remove judgment from the process. It is to remove unexamined bias from that judgment.

Pairing Data With Experience

Predictive analytics and cohort analysis increasingly support this work. A drop in retention among customers signed after a particular product release can surface concerns early. The same is true of a decline in marketplace take rates across multiple regions, often before either trend becomes obvious in quarterly reporting. Data alone does not resolve the decision, however. It works best when paired with judgment. An operating partner brings an execution lens, an investment partner brings a risk lens, and together the question becomes not only whether a company deserves more capital, but what specific conditions would justify it.

This process resembles diagnosis in medicine more than it resembles arithmetic. Symptoms are observed, indicators are reviewed, and history is taken into account, but the final judgment still belongs to a person weighing all of it together. Over-treatment can be just as costly as under-treatment in this context. A fast, honest conclusion better serves some companies, freeing up capital and talent for redeployment, while others genuinely need additional support because their inflection point sits just one iteration away. Distinguishing between these two situations, consistently and without favoritism toward whichever company tells the better story, is what separates disciplined triage from improvisation.

The Psychology Behind the Hardest Calls

Even with strong frameworks in place, the most difficult moments in venture remain psychological rather than analytical. By the time a write-down decision arrives, the warning signs have usually been visible for some time. What makes the moment hard is not a lack of information. It is the emotional weight of admitting that a thesis once believed in in earnest did not hold.

Three biases tend to dominate this moment. Loss aversion makes the pain of marking down an investment feel larger than the relief of redirecting that capital elsewhere, which often disguises itself as patience rather than avoidance. The sunk cost fallacy encourages investors to stay the course based on what they have already spent rather than what future capital is likely to return. Narrative inertia may be the most subtle of the three. Investors become attached to the story they helped build and shared with colleagues and limited partners, which makes walking away feel personal rather than strategic.

Decision Hygiene as a Counterweight

To manage these biases, some firms use structured techniques borrowed from broader decision science.

- A red team review brings in colleagues with no prior involvement in the deal to assess the company independently, breaking the feedback loop between the original champion and continued funding.

- A pre-mortem asks the team to imagine the company failing despite renewed investment and to identify the most likely causes, which helps distinguish temporary setbacks from deeper structural problems.

Firms that build psychological safety into these conversations tend to make better decisions over time. Where acknowledging a mistake carries high internal cost, follow-on capital tends to flow toward narrative rather than evidence. Where firms reward intellectual honesty, underperformance becomes a source of institutional learning rather than a personal failure to avoid.

Accountability to Limited Partners and the Portfolio as a Whole

These decisions do not occur in isolation. Limited partners are the institutional investors and family offices that fund a venture firm’s mandate. They accept the power-law nature of returns, but they still expect consistency, transparency, and discipline in how a firm handles underperformance. When general partners cannot clearly explain why a company continues to receive support despite repeated misses, trust erodes. That erosion eventually affects the firm’s ability to raise future capital.

This dynamic introduces the idea of portfolio velocity. It is the principle that a well-managed portfolio must continuously learn, adapt, and reallocate attention. Capital and partner time tied up in low-promise companies carry a cost beyond the balance sheet. Every hour spent chasing a final pivot for a fading company takes time away from one with genuine breakout potential. Fund maturity adds another layer to this calculation. The appetite for supporting laggards tends to narrow as a fund’s exit window shortens, regardless of whether a company’s underlying prospects have changed.

External perception adds a further layer of complexity to these decisions. Whether a respected firm continues to back a company shapes its standing with downstream investors, prospective acquirers, and potential hires. A new term sheet signals confidence. A quiet absence from a funding round signals the opposite. These signals can become self-reinforcing. This is part of why some firms steer a struggling company toward what is sometimes called a soft landing. It is an acquisition that may fall short of venture-scale returns. But it recovers some capital, preserves goodwill, and lets a team’s work find a new home rather than disappearing entirely.

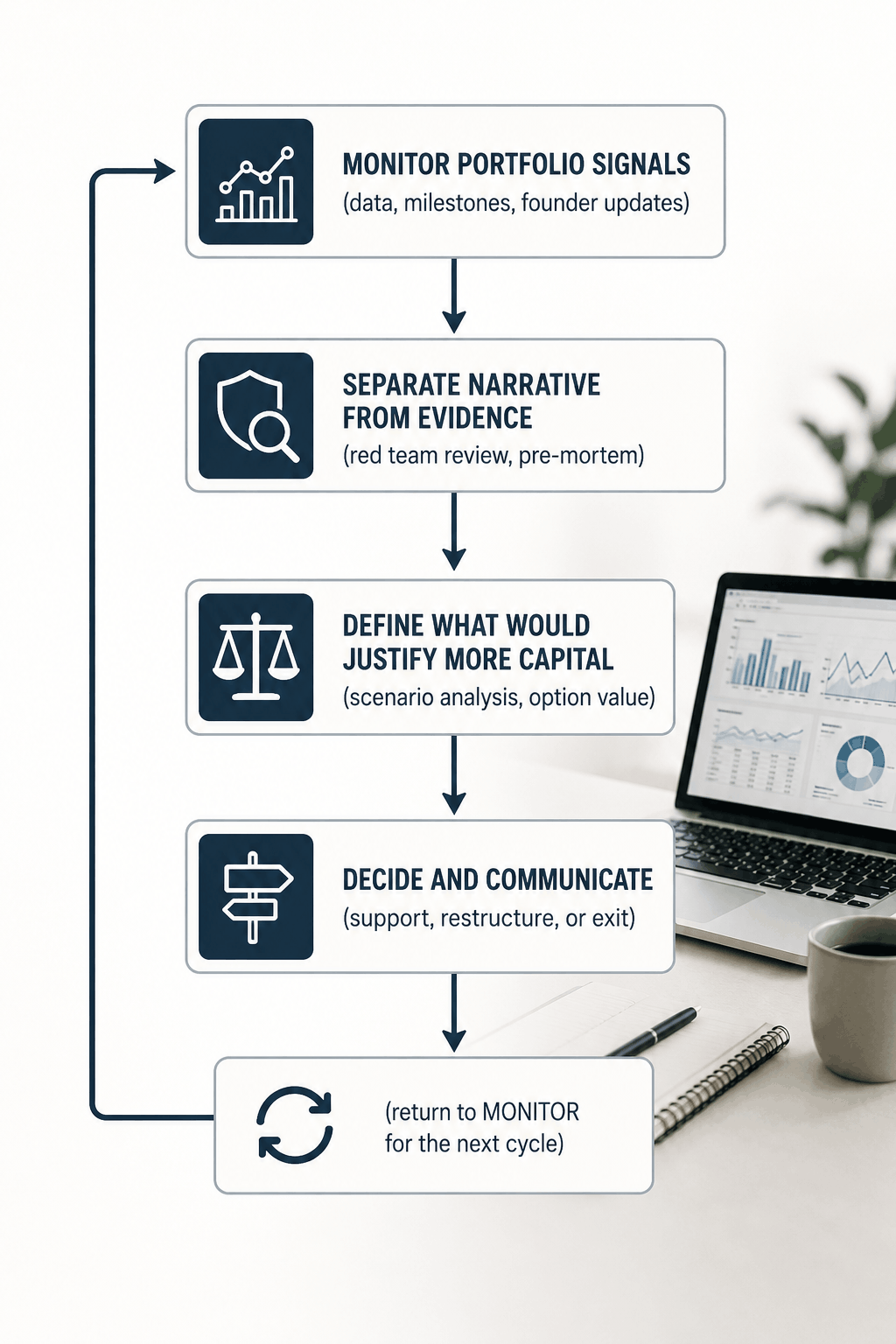

A Simple Framework for Triage Decisions

These examples reveal a pattern that works best as a continuous cycle rather than a single decision point.

Letting Go Without Losing Trust

How a firm exits an underperforming investment matters as much as the decision itself. Founders are people, not assets, and a decision to stop funding a company carries personal as well as financial weight. The investors who handle this well are transparent without being unkind. They help founders wind down with dignity and support efforts to redeploy talent. In some cases, they guide a company toward an acquisition that may not produce venture-scale returns. That path preserves goodwill, recovers some capital, and allows a team’s work to continue elsewhere.

This matters beyond any single decision. Reputation compounds in venture capital faster than capital itself. A firm that props up failing companies indefinitely may appear undisciplined, while a firm that exits abruptly and without support may seem transactional. The respected position sits between these extremes, marked by clear thinking, honest communication, and care for the people involved even when the financial outcome falls short.

Conclusion

The willingness to let go is ultimately a test of judgment rather than financial modeling. Venture capitalists who handle underperformance well tend to share certain habits. They separate sunk cost from option value, build structured reviews that reduce personal bias, and treat data as one input among several, not a final verdict. Founders also deserve honesty and respect even when capital is withdrawn. And they know limited partners deserve consistency in how the firm makes and explains these decisions. None of this removes the difficulty of the moment. A company that once held genuine promise rarely fails without leaving some sense of unfinished possibility behind. What separates strong investors from the rest is not the absence of that discomfort. It is the discipline to act on evidence rather than sentiment, and the clarity to communicate that decision honestly. In an industry built on asymmetric outcomes, walking away from a fading bet deliberately and with integrity often does as much for long-term performance as recognizing a winner in the first place.

Disclaimer: This blog is intended for informational purposes only and does not constitute legal, tax, or accounting advice. You should consult your own tax advisor or counsel for advice tailored to your specific situation.

Hindol Datta is a seasoned finance executive with over 25 years of leadership experience across SaaS, cybersecurity, logistics, and digital marketing industries. He has served as CFO and VP of Finance in both public and private companies, leading $120M+ in fundraising and $150M+ in M&A transactions while driving predictive analytics and ERP transformations. Known for blending strategic foresight with operational discipline, he builds high-performing global finance organizations that enable scalable growth and data-driven decision-making.

AI-assisted insights, supplemented by 25 years of finance leadership experience.