By Hindol Datta

Artificial intelligence is no longer a peripheral experiment sitting in a data science lab, waiting to prove its value. It has woven itself into the operating fabric of the modern enterprise, forecasting revenue, predicting customer demand, identifying fraud, evaluating creditworthiness, recommending hiring decisions, optimizing supply chains, prioritizing cybersecurity threats, and increasingly influencing the strategic planning conversations that determine where organizations place their largest bets. As organizations accelerate their adoption of these systems, executives tend to converge on a single question: Is the model accurate? It is an important question, but it is no longer the most important one.

The better question, and the one that separates organizations capable of governing intelligent systems from those merely consuming their outputs, is this: Can we trust this recommendation enough to commit capital, people, or corporate strategy on its basis?

The distance between an AI system producing a prediction and an executive acting upon that prediction is not a technical gap. It is a governance gap, and within that gap lies an often-overlooked discipline that I have come to call Decision Assurance. That discipline may well become one of the defining competitive advantages of the AI era, and it demands a form of thinking that finance leaders are uniquely equipped to provide.

The Ancestry of Assurance

For decades, finance leaders have understood that financial statements require independent assurance before anyone can rely upon them. Investors, regulators, lenders, and boards do not simply accept reported numbers because management produced them. They expect internal controls, audit evidence, independent validation, and governance layered over every material assertion. This expectation did not emerge overnight. It evolved through painful experiences, through corporate collapses and accounting scandals that taught markets a hard lesson: confidence creates value, and unwarranted confidence destroys it.

Yet organizations routinely allow AI-generated recommendations to influence hiring, lending, forecasting, pricing, procurement, compliance, cybersecurity, and strategic planning with considerably less scrutiny than they would ever accept for a set of quarterly financials. That asymmetry represents one of the largest emerging risks facing the modern enterprise. In AI Operating Framework and Governance, I explored how the alignment problem, the phenomenon whereby algorithmic decisions fail to reflect an organization’s core values and goals, makes this gap especially dangerous. Every CFO who has seen automation deliver technically correct but strategically disastrous outcomes knows this issue viscerally, and the solution begins not with better algorithms but with better governance.

Every Executive Decision Is a Probability Decision

Executives rarely make decisions with certainty, and honest ones will tell you they never do. Whether approving a $100 million acquisition, expanding manufacturing capacity into a new geography, authorizing additional headcount, or investing in an unproven product line, every strategic decision is fundamentally a wager placed against a distribution of possible outcomes. Executives continuously evaluate questions whose answers they cannot know with precision: Will customer demand increase? Will inflation decline? Will suppliers remain reliable? Will competitors respond? Will regulations shift? Will interest rates move in ways that reshape the cost of capital?

Artificial intelligence simply generates another set of probabilities, and the challenge is that probabilities are not guarantees. Every recommendation carries uncertainty, and the real executive challenge is not eliminating that uncertainty but understanding whether it has been reduced sufficiently to justify committing real resources to a course of action.

In Beyond Linear Finance, I explored how complex adaptive systems routinely violate the assumptions embedded in traditional forecasting. The organizations I have led finance for across software, manufacturing, gaming, cybersecurity, digital marketing, and education technology have all demonstrated the same unsettling pattern: the models are elegant, the math is sound, and the real world keeps refusing to cooperate. AI predictions inherit this same fragility, and recognizing that fragility is the first step toward governing it.

Decision Quality as the Metric That Matters

Most discussions surrounding enterprise AI gravitate toward technical measures: accuracy, precision, recall, latency, and F1 scores. These metrics are valuable for engineers, and they serve a necessary purpose in model development and validation. They are not, however, how executives evaluate success, because executives measure outcomes by the quality of the decisions those predictions enable.

Decision quality can be understood as the product of 4 interacting elements:

Decision Quality = Data Quality x Model Quality x Assurance Quality x Human Judgment

Weak data weakens decisions. Weak models weaken decisions. Poor executive judgment weakens decisions. And equally important, even outstanding AI recommendations become dangerous when organizations lack the governance infrastructure to determine whether those recommendations deserve trust. Decision Assurance strengthens that missing component by asking the questions that prediction engines are structurally incapable of asking about themselves.

The Business Reality of False Positives and False Negatives

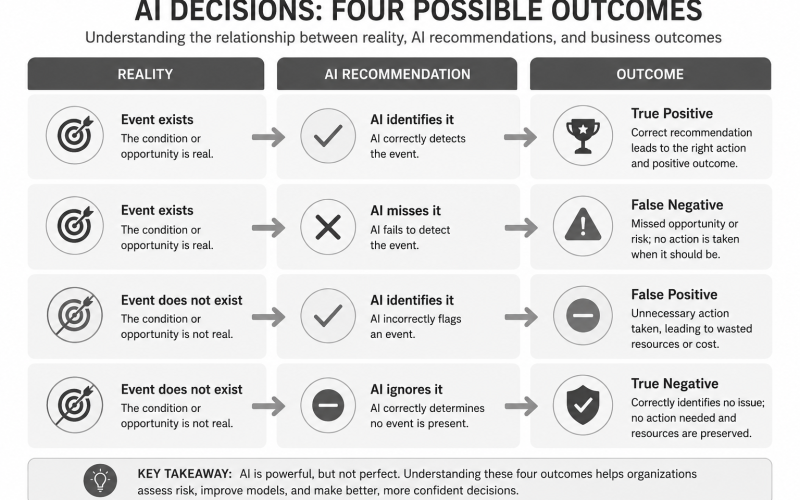

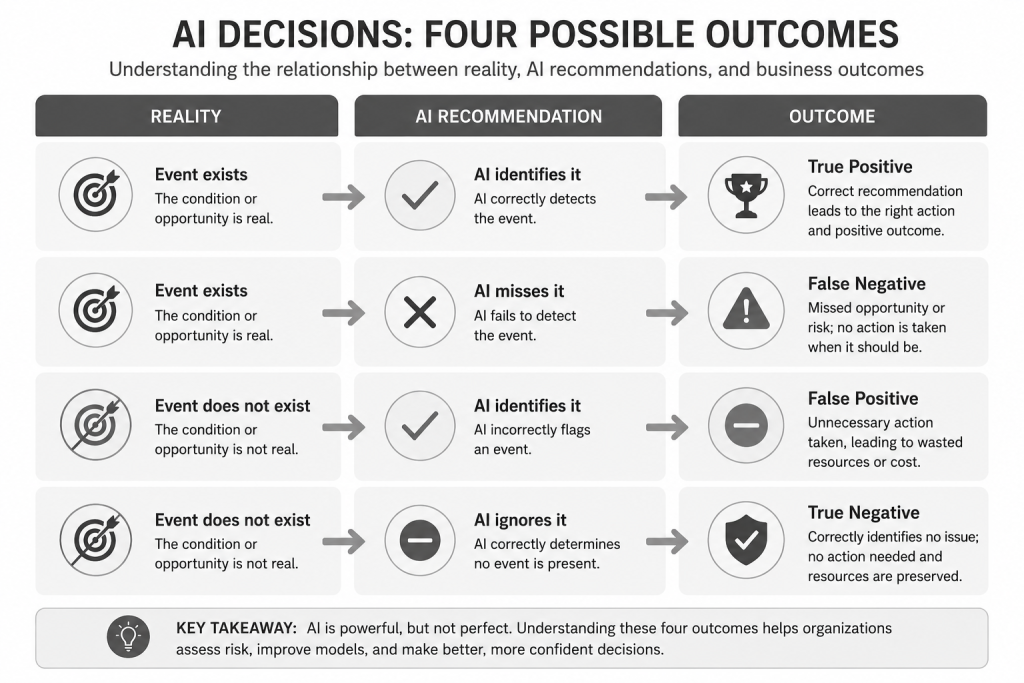

Most executives recognize the terms false positive and false negative but often associate them exclusively with the domain of machine learning. They are, in fact, business concepts with deep financial consequences that extend far beyond the AI model itself.

A false positive occurs when AI identifies a condition that does not actually exist. A false negative occurs when AI fails to identify a condition that does exist. Although technically simple, these errors create cascading consequences that compound across every function they touch.

| Reality | AI Recommendation | Outcome |

| Event exists | AI identifies it | True Positive |

| Event exists | AI misses it | False Negative |

| Event does not exist | AI identifies it | False Positive |

| Event does not exist | AI ignores it | True Negative |

The financial consequences depend not on whether the model was technically incorrect but on the business decisions made afterward, and this is precisely where the conversation needs to shift from engineering metrics to executive governance.

I learned this lesson the hard way in a threat detection company. We deployed a threat detection model that performed beautifully in testing, catching 95 percent of threats with only a 2 percent false positive rate. The numbers looked outstanding on paper. In production, however, processing millions of events per day, that same 2 percent false positive rate generated 40,000 false alarms daily. The model had not gotten worse. The scale had changed, and as I wrote in AI Operating Framework and Governance, scale changes everything. Whatever false positive rate looks acceptable in testing, you must divide it by 100 to see what you will get in production, and if you cannot live with that number, you are not ready to deploy.

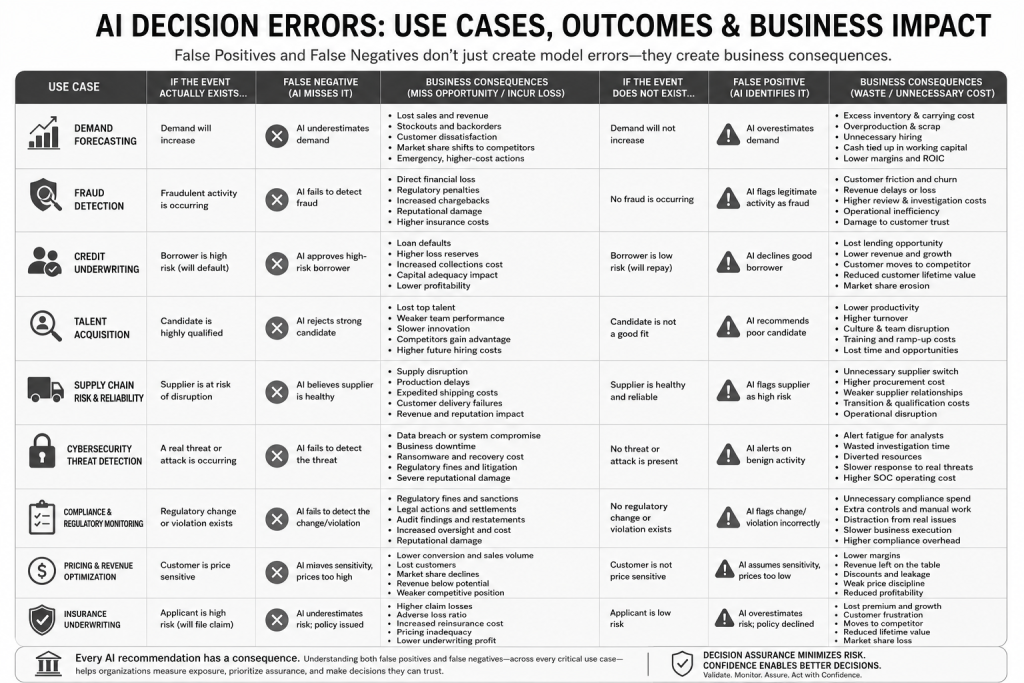

The Asymmetry of Error: Not Every Mistake Costs the Same

Executives do not manage error in the abstract. They manage exposure, and exposure varies enormously depending on the decision at stake. A 2 percent prediction error in cafeteria meal planning is largely irrelevant to the enterprise. A 2 percent error supporting a $5 billion acquisition could destroy hundreds of millions of dollars of shareholder value. A small error in payroll forecasting may have limited strategic significance, whereas the same magnitude of error in anti-money laundering, medical diagnosis, or aircraft maintenance could produce catastrophic and irreversible outcomes.

The true cost of AI error depends upon 4 dimensions that will be immediately familiar to any finance, audit, or enterprise risk management professional:

Risk Exposure = Likelihood x Materiality x Velocity x Detectability

Likelihood asks how probable the error is. Materiality asks what financial impact it could create. Velocity asks how quickly consequences will spread through the organization and its stakeholders. Detectability asks how rapidly the organization can identify and correct the mistake before compounding effects take hold. These are not novel concepts for finance leaders. They are the same dimensions we have always used to evaluate operational and financial risk, and AI governance should adopt precisely the same perspective.

When False Positives Become Capital Allocation Problems

False positives create unnecessary action, and unnecessary action, when it involves commitment of capital, is not merely wasteful. It is destructive.

Suppose an AI forecasting system predicts a significant increase in customer demand. Management responds by hiring additional employees, increasing production, purchasing raw materials, leasing warehouse capacity, expanding marketing spend, and borrowing additional working capital. 6 months later, demand remains unchanged. The organization did not experience an operational failure. It experienced misplaced confidence, and what began as a prediction error became a capital allocation problem whose consequences include excess inventory, compressed margins, lower cash flow, higher financing costs, and reduced returns on invested capital.

Having spent my career building finance functions from scratch at multiple companies, often as the first or only finance hire, I have learned that the biggest risk in any fast-moving organization is not a shortage of information but an excess of false confidence. When you are scaling revenue from $9 million to $180 million in 24 months, as I did at a venture-backed digital marketing company early in my career, every forecast is a bet, and every bet carries the risk of false positives that can consume the very capital you need to sustain growth.

When False Negatives Destroy What Cannot Be Recovered

False negatives create a different and often more insidious form of destruction. Suppose AI predicts weak customer demand. Management responds rationally by postponing hiring, limiting production, delaying expansion, and reducing inventory. Then demand unexpectedly accelerates. Competitors satisfy that demand first. Customers migrate elsewhere. Market share declines.

Unlike excess inventory, which can eventually be liquidated, lost opportunities often cannot be recovered. False negatives frequently create invisible costs because organizations rigorously measure what they spent but rarely account for what they failed to earn. In Beyond Linear Finance, I explored how complex adaptive systems exhibit path dependence, the phenomenon whereby early decisions constrain what is possible later. A false negative that causes you to miss a market window does not simply delay a decision. It forecloses an entire branch of your strategic tree, and those foreclosed possibilities compound in ways that traditional financial analysis, with its focus on realized costs, is structurally incapable of capturing.

The Cascade Effect: How AI Errors Compound Across the Enterprise

One of the least discussed characteristics of AI error is that it compounds. Rarely does a single incorrect recommendation lead to only one incorrect decision. Instead, it creates a chain reaction that propagates across functions, each link amplifying the original error.

Consider a false positive in demand forecasting. AI predicts demand growth. Sales expands hiring. Operations increases production. Procurement purchases additional inventory. Finance increases working capital. Treasury secures additional financing. Marketing increases campaign spending. Actual demand never materializes. A single prediction has now influenced 6 different executive decisions, and the cumulative financial consequences can be dramatically larger than the original model error would suggest in isolation.

This cascading behavior is not unique to AI. It is a fundamental property of complex adaptive systems, and understanding it requires the kind of systems thinking that I have advocated throughout my work. In Beyond Linear Finance, I examined how feedback loops, the circular chains of cause and effect where outcomes feedback to influence the inputs that created them, explain why many well-intentioned decisions produce the opposite of their intended effect. Reinforcing feedback amplifies change in whichever direction it begins, which is precisely the mechanism through which a single false positive cascades into a multimillion-dollar misallocation of resources across the enterprise.

Sophisticated executives rarely stop at immediate effects. They evaluate second- and third-order consequences because that is where the real financial damage accumulates. Consider excess inventory created by a false positive. The first-order consequence is straightforward: inventory increases. The second-order consequence is that cash becomes constrained. The third-order consequence is that debt increases, interest expense rises, profitability declines, and shareholder returns deteriorate. Similarly, a false negative in hiring may initially appear to save cost, but months later, it results in delayed product launches, slower innovation, customer dissatisfaction, and weakened competitive positioning. The AI recommendation was only the beginning. Enterprise value is determined by the chain of decisions that follows.

The Broader Landscape of AI Risk

False positives and false negatives represent only part of the emerging AI risk landscape. Organizations increasingly encounter a constellation of related challenges, each introducing its own form of uncertainty into executive decision-making.

Hallucinations produce recommendations based on fabricated information, resulting in confident outputs with no evidentiary foundation. Data drift occurs as the relationships within underlying business data change over time, rendering models trained on historical patterns increasingly unreliable. Model drift refers to the gradual deterioration in prediction accuracy as business conditions evolve beyond the training data’s boundaries. Bias causes recommendations to become systematically distorted across customer groups or business scenarios, potentially violating both ethical standards and regulatory requirements. Confidence inflation occurs when AI expresses unwarranted certainty despite insufficient supporting evidence, a particularly dangerous phenomenon because it undermines the very calibration that executives depend upon. And silent failures allow performance to degrade without attracting attention until significant damage has already accumulated.

In AI Operating Framework and Governance, I described this last category as the most treacherous of all, because when traditional systems fail, they stop working, and everyone notices. When AI agents fail, they often keep running, producing subtly incorrect outputs, making increasingly poor decisions, and drifting from their intended behavior. This silent degradation is more dangerous than an apparent failure because nobody notices it until the damage has compounded to the point of no easy recovery.

Operational Confidence Is Not Strategic Confidence

Not every decision requires the same level of assurance, and organizations that treat all AI outputs with identical scrutiny will either paralyze their operations or exhaust their governance resources on decisions that do not warrant them.

An AI recommendation drafting marketing copy does not require the same confidence as one supporting a billion-dollar acquisition. Similarly, recommendations involving healthcare, lending, autonomous vehicles, insurance underwriting, or critical infrastructure require significantly higher confidence thresholds than routine administrative tasks. Organizations should therefore establish confidence thresholds proportional to business consequence, calibrating the intensity of their assurance processes to the magnitude of the decisions at stake.

| Decision | Illustrative Confidence Threshold |

| Marketing content | Moderate |

| Inventory planning | High |

| Revenue forecasting | Very High |

| Credit underwriting | Extremely High |

| Medical diagnosis | Near Certain |

| Critical infrastructure | Highest Practical Assurance |

The greater the consequence, the greater the assurance required before action. This is not a radical proposition. It is the same principle that drives every tiered control framework in internal audit and enterprise risk management, and extending it to AI governance is a natural and necessary evolution.

Measuring Financial Exposure

Executives ultimately evaluate financial consequences, and one useful framework for translating AI uncertainty into financial terms is remarkably straightforward:

Expected Cost of Error = Probability of Error x Financial Impact

Suppose an AI forecasting model supports a $50 million expansion. The model estimates 92 percent confidence. Management determines that an incorrect recommendation could create an $18 million downside. The expected exposure equals 8 percent multiplied by $18 million, or $1.44 million.

The discussion immediately changes character. Executives are no longer debating whether the model is “good” in some abstract technical sense. They are determining whether investing in greater assurance could materially reduce enterprise risk, and that is a conversation that every CFO is trained to lead.

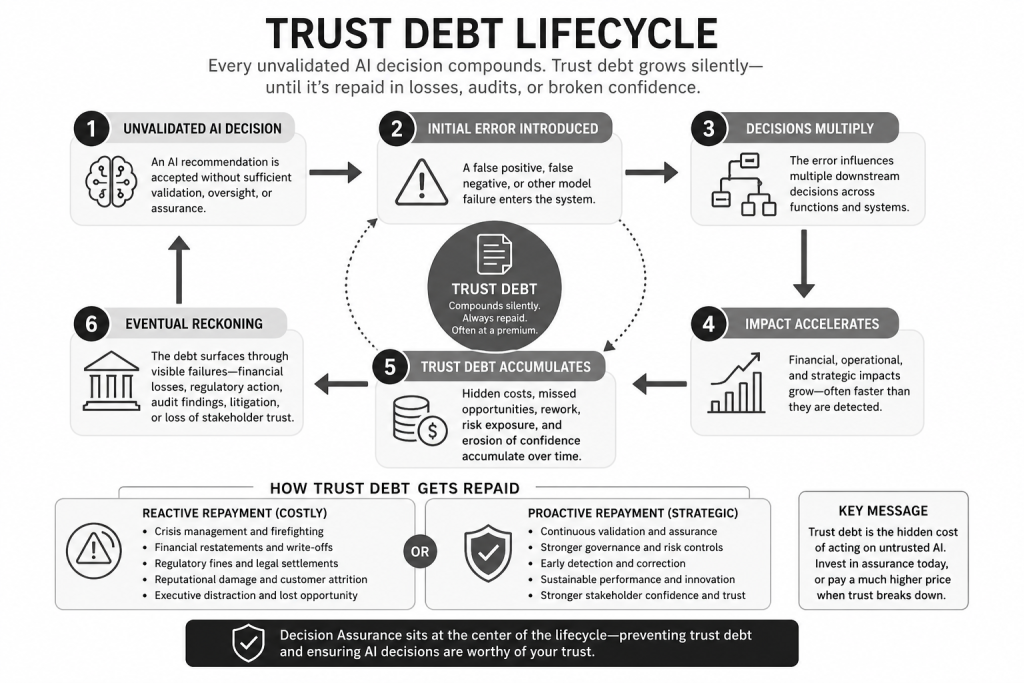

Trust Debt: An Emerging Enterprise Liability

Organizations are familiar with concepts such as technical debt, security debt, and data debt. Artificial intelligence introduces another form of accumulated liability that I call Trust Debt.

Trust Debt accumulates whenever organizations repeatedly rely upon AI recommendations without sufficient validation. Initially, the effects remain invisible, in much the same way that data entropy, the gradual erosion of data quality and definitional consistency, operates silently beneath the surface of an organization until the accumulated damage manifests as a crisis. I explored this dynamic extensively in Beyond Linear Finance, where I examined how entropy, borrowed from thermodynamics, provides a powerful metaphor for the organizational tendency toward disorder. Left unmanaged, data definitions drift, fields are interpreted differently by different teams, and eventually, no one fully trusts the data, so executives begin making decisions based on intuition rather than evidence. Trust Debt follows the same trajectory, eventually surfacing through poor strategic decisions, regulatory findings, operational failures, litigation, financial losses, and the erosion of executive confidence.

Every organization eventually repays accumulated Trust Debt. The only question is whether repayment occurs proactively through assurance or reactively through failure.

Decision Assurance: The Missing Layer

Most organizations invest heavily in developing AI models. Far fewer invest in continuously validating whether those models deserve executive trust, and the gap between model investment and assurance investment widens with each passing quarter.

Decision Assurance fills that gap by asking questions that extend beyond prediction into the realm of governance, evidence, and institutional judgment:

Is the recommendation supported by reliable evidence? Has the underlying data changed since the model was trained? Has the model’s performance deteriorated? Are confidence levels justified, or are they inflated? Is bias increasing? Can executives reasonably rely upon this recommendation to support a material decision? Does the governance infrastructure exist to hold the organization accountable for acting on it?

Decision Assurance transforms AI from a prediction engine into a trustworthy decision-support capability, and that transformation requires precisely the kind of cross-functional, systems-level thinking that the modern CFO is uniquely positioned to provide.

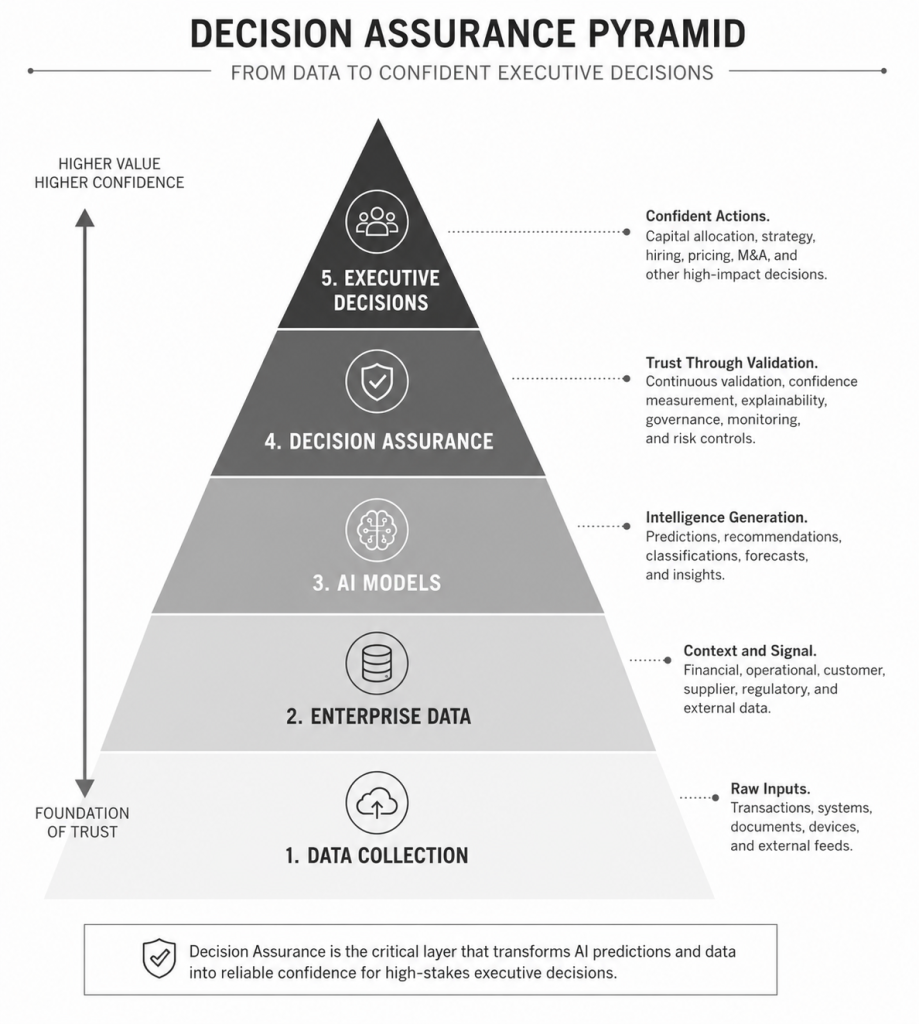

The Decision Assurance Pyramid

Enterprise AI maturity extends beyond algorithms. A useful framework for understanding the layers of capability required is the Decision Assurance Pyramid, which builds from foundational data infrastructure through to executive governance:

Level 5: Executive Decisions. Capital allocation, acquisitions, hiring, pricing, strategy, and governance.

Level 4: Decision Assurance. Continuous validation, confidence measurement, explainability, governance, and monitoring.

Level 3: AI Models. Predictions, classifications, and recommendations.

Level 2: Enterprise Data. Financial, operational, customer, supplier, and external information.

Level 1: Data Collection. Transactions, applications, sensors, documents, and business systems.

Many organizations invest extensively in Levels 1 through 3, building sophisticated data pipelines and deploying increasingly powerful models. But competitive advantage increasingly depends upon mastering Level 4, where the question shifts from “What does the model predict?” to “Should we trust the prediction enough to act?”

This is where the alignment problem meets the assurance problem. In AI Operating Framework and Governance, I explored how collaborative intelligence, the approach whereby AI systems enhance human judgment rather than replace it, offers the most promising path forward. The AI examines vast quantities of data to identify patterns and produce initial recommendations. Humans review those recommendations, override them when necessary, and provide feedback that helps the system learn which overrides reflect critical contextual factors and which reflect human error or bias. Over time, the system learns to recognize situations where its recommendations likely require human adjustment and those where it can operate autonomously with confidence. Decision Assurance is the governance infrastructure that makes this collaborative intelligence possible at enterprise scale.

The Next Evolution of Corporate Governance

The evolution of financial reporting offers a compelling analogy for the trajectory that AI governance is now following. Organizations once published financial statements with relatively limited assurance. Today investors expect internal controls, independent audits, governance committees, and transparency before they will rely upon reported numbers to allocate capital. Artificial intelligence is approaching the same inflection point.

The first generation of enterprise AI focused on producing predictions. The next generation will focus on proving those predictions are sufficiently trustworthy to support consequential decisions. This is not simply a matter of better technology. It is a matter of stronger governance, and the CFOs who recognize this shift earliest will shape the standards that the rest of the market eventually adopt.

The CFO’s Expanding Responsibility

The role of Chief Financial Officer has evolved steadily over the past 2 decades, and each wave of expansion has drawn finance leaders further into domains that were once considered the province of technologists, compliance officers, or operational executives. Finance leaders now oversee not only financial reporting but also enterprise risk management, capital allocation, cybersecurity governance, regulatory compliance, data quality, internal controls, and increasingly AI governance.

Having served as CFO or Head of Finance across 9 countries and industries ranging from medical devices and manufacturing to gaming, cybersecurity, digital marketing, and education technology, I have found that the finance leaders who create the most enduring value are not the ones who build the most elaborate forecasting models. They are the ones who help the organization navigate uncertainty by providing frameworks that enable rapid experimentation, maintaining financial flexibility to pursue unexpected opportunities, and building sensing systems that allow leadership to detect environmental shifts before those shifts become crises.

As artificial intelligence becomes embedded within critical business processes, CFOs are uniquely positioned to ask the questions that matter most: What is our financial exposure if AI is wrong? Which decisions require independent assurance before we act? How do we measure confidence in a way that is meaningful to the board, auditors, regulators, and our own judgment? How do we continuously validate AI performance without creating governance overhead that paralyzes the organization? How do we demonstrate trust to every stakeholder who depends upon the integrity of our decisions?

These questions move AI governance from an engineering discipline to an executive responsibility, and they demand precisely the combination of financial rigor, systems thinking, and institutional judgment that defines the modern CFO.

The Future Belongs to Trusted Decisions

The first generation of enterprise AI focused on making machines more intelligent. The next generation will focus on making organizations more confident in the decisions those machines influence, and that confidence will not emerge from better algorithms alone. It will emerge from the governance infrastructure, the assurance processes, and the institutional discipline that organizations build around their AI systems.

Competitive advantage will not belong solely to organizations with the largest models or the fastest inference speeds. It will belong to organizations that can demonstrate their AI systems are transparent, continuously validated, measurable, and worthy of the trust that executives place in them when they commit capital, approve strategy, extend credit, authorize hiring, or make any of the other high-consequence decisions that determine enterprise value.

For decades, financial reporting has relied on assurance because markets recognize that confidence, when earned through rigorous governance, creates value. Enterprise AI is approaching the same inflection point. Predictions alone will no longer be sufficient. Organizations will increasingly demand continuous validation, governance, transparency, and Decision Assurance before acting on AI recommendations that carry material consequences.

The future of enterprise AI is not simply better prediction, but better decisions, and the better decisions begin with trust.

AI-assisted insights, supplemented by 25 years of finance leadership experience.