Executive Summary

The distinction between audit vs review vs compilation is one that most founders encounter for the first time in the middle of a financing round or board-level conversation, precisely when clarity matters most. Each term describes a different level of financial assurance provided by external accountants, and each communicates something specific to the investors, lenders, and acquirers who request them. Understanding where these engagements differ, what each one demands from a company’s internal operations, and when each applies is not a technical nicety. It is foundational to building financial credibility at every stage of growth. Over three decades of finance leadership with venture-backed companies across cybersecurity, SaaS, logistics, and medical devices, I have seen founders accelerate financing processes by understanding this distinction early, and watched others lose weeks of momentum by treating it as a detail to address later. This article provides the clarity that every finance-aware founder needs.

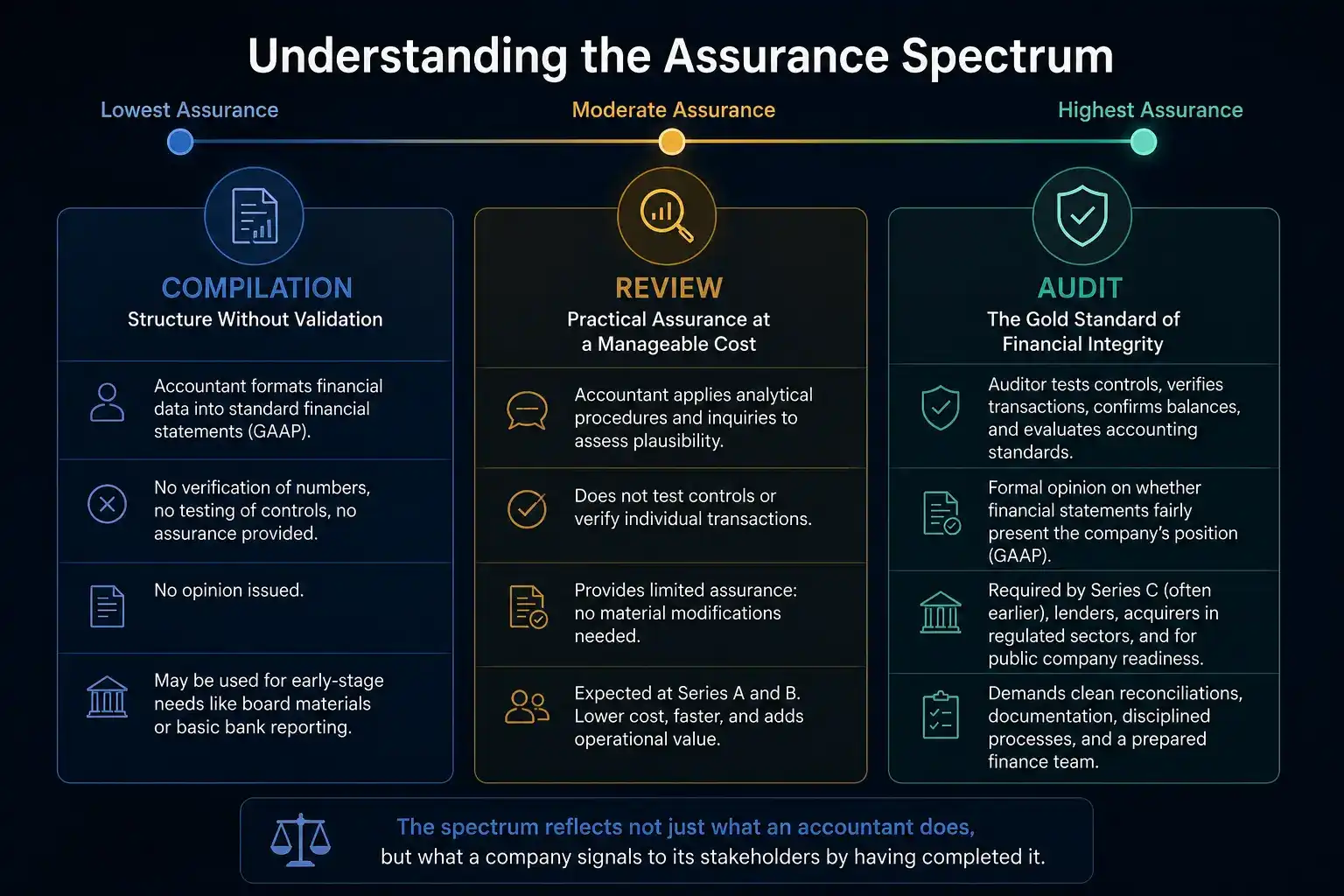

Understanding the Assurance Spectrum

The audit vs review vs compilation spectrum describes three levels of financial statement assurance, each sitting at a different point on a continuum of external scrutiny. At one end, a compilation involves minimal external testing. At the other, an audit requires deep examination of controls, documentation, and accounting treatment. A review occupies the middle ground, offering meaningful but limited assurance without the full rigor of an audit. Each level reflects not just what an accountant does but what a company signals to its stakeholders by having completed it.

Founders who understand this spectrum can plan proactively, engage the right firm at the right time, and avoid the costly delays that arise when a company discovers mid-round that its financial statements do not meet the assurance standard a lead investor requires.

Compilation: Structure Without Validation

A compilation is the lightest engagement available. An accountant takes the company’s internal financial data and formats it into standard financial statements under generally accepted accounting principles. The accountant does not verify the underlying numbers, test internal controls, or assess the reliability of supporting documentation. The resulting report carries no opinion and provides no assurance.

For very early-stage companies preparing board materials or basic bank reporting, a compilation may be sufficient. It brings structure to financial presentation. What it does not bring is credibility with institutional investors, strategic acquirers, or sophisticated lenders. No serious external capital provider will rely on a compilation alone as evidence of financial integrity.

Review: Practical Assurance at a Manageable Cost

A review goes further. The accountant applies analytical procedures and targeted inquiries to assess whether the financial statements appear plausible. They compare current results to prior periods and probe specific balances, but do not verify individual transactions or test internal controls.

The output is a formal report providing limited assurance: the accountant is not aware of any material modifications needed for the statements to conform with the applicable accounting standard.

Reviews have become the expected standard for companies raising institutional rounds at Series A and Series B. They cost less than audits and complete faster, but they require organized books, consistent documentation, and a finance lead who can manage the engagement. In my experience guiding companies through reviews, the process has consistently highlighted areas for operational improvement, producing value well beyond the report itself.

Audit: The Gold Standard of Financial Integrity

An audit is the most comprehensive engagement. The auditor independently tests internal controls, traces transactions to source documentation, confirms account balances with third parties, and evaluates how accounting standards have been applied. The result is a formal opinion on whether the financial statements fairly represent the company’s financial position in accordance with generally accepted accounting principles. This is full assurance, and it carries significant weight.

A compilation audit comparison makes the distinction clear: a compilation organizes what management provides, while an audit independently verifies whether what management provides is accurate. That difference matters enormously in high-stakes contexts.

Audits are typically required by Series C, sometimes earlier depending on the investor profile. Lenders extending credit facilities frequently require them. Acquirers in regulated sectors will almost always expect audited financials before proceeding with diligence. Public company readiness demands them as a baseline.

The demands are proportionally greater. An audit requires clean reconciliations, signed contracts, a well-maintained cap table, disciplined revenue recognition, and a finance team capable of responding to a prepared-by-client list under time pressure. Companies that have built these habits in advance complete audits efficiently. Those that have not face rework, delay, and in some cases lost transactions.

When Each Engagement Applies

The right level of assurance depends on where a company sits in its growth path and what its stakeholders require:

- Seed and pre-Series A: A compilation may suffice for internal reporting and early banking relationships, provided the company maintains disciplined internal records.

- Series A and Series B: A review is the standard expectation for institutional venture investors. A well-organized company can complete one in three to four weeks.

- Series C and beyond: An audit is typically required. Engage the audit firm at least six months before the expected delivery date to allow time for any remediation.

- Credit facilities and strategic partnerships: Requirements vary. Some lenders accept reviews; others require audits. Confirm the standard before the engagement begins.

The Strategic Value of Assurance

What many founders underestimate is that each engagement produces value beyond compliance. An audit vs review comparison is often framed as a cost-benefit question, but the more useful frame is what each engagement reveals about the business.

During one company’s first audit, a misapplied revenue recognition policy came to light that, once corrected, improved gross margin visibility and strengthened the story for the subsequent financing round. In another engagement, a review process surfaced inconsistencies in expense classification that, when addressed, improved forecasting accuracy and gave the board greater confidence in management’s numbers. Assurance engagements at every level create opportunities to strengthen the underlying financial infrastructure, and the companies that extract the most value from them are those that treat the process as a diagnostic rather than a formality.

Choosing the Right Firm

Not every accounting firm is the right fit for every stage. A firm with experience in venture-backed companies understands the documentation standards, timeline pressures, and revenue recognition nuances that early-stage businesses routinely face. The firm that serves a company well at seed may lack the capacity or technical depth for a Series C audit.

When selecting a firm, consider the following:

- Direct experience with venture-backed companies at your stage and sector

- Capacity to meet your timeline during financing-critical periods

- A lead partner who remains actively involved throughout the engagement

- Familiarity with the accounting standards most relevant to your business model

Conclusion

The audit vs review vs compilation distinction is not a technical footnote. It is a strategic signal that communicates a company’s financial maturity to every stakeholder who asks for it. Founders who understand the spectrum early make better decisions about when to invest in each engagement, what to prepare in advance, and how to leverage the process for internal improvement rather than treating it purely as a compliance cost. Over three decades of working with venture-backed companies across every growth stage, the consistent pattern has been the same: the companies that reached financing milestones fastest were those that understood what each engagement demanded and built their financial operations to meet that standard before the requirement arrived.

Disclaimer: This blog is intended for informational purposes only and does not constitute legal, tax, or accounting advice. You should consult your own tax advisor or counsel for advice tailored to your specific situation.

Hindol Datta is a seasoned finance executive with over 25 years of leadership experience across SaaS, cybersecurity, logistics, and digital marketing industries. He has served as CFO and VP of Finance in both public and private companies, leading $120M+ in fundraising and $150M+ in M&A transactions while driving predictive analytics and ERP transformations. Known for blending strategic foresight with operational discipline, he builds high-performing global finance organizations that enable scalable growth and data-driven decision-making.

AI-assisted insights, supplemented by 25 years of finance leadership experience.