Executive Summary

This article summarizes a CFO perspective on diligence across four streams. Legal, financial, operational, and technical review each play a distinct role. Business due diligence works best as a philosophy rather than a checklist. It exists to surface what a buyer does not yet know to ask. It is not simply about confirming what everyone already believes. Legal review tests contract enforceability and IP ownership. Financial review tests revenue quality and earnings normalization. Operational review tests whether internal processes can actually scale. Technical review tests code quality and cybersecurity posture. None of these streams should stay siloed. Findings from one stream should shape pricing and terms in another. A single master risk register keeps that coordination intact. Sellers who prepare their own diligence binder in advance tend to close faster. They also tend to command a stronger price, since transparency signals confidence rather than exposure.

Why Business Due Diligence Is a Philosophy, Not a Checklist

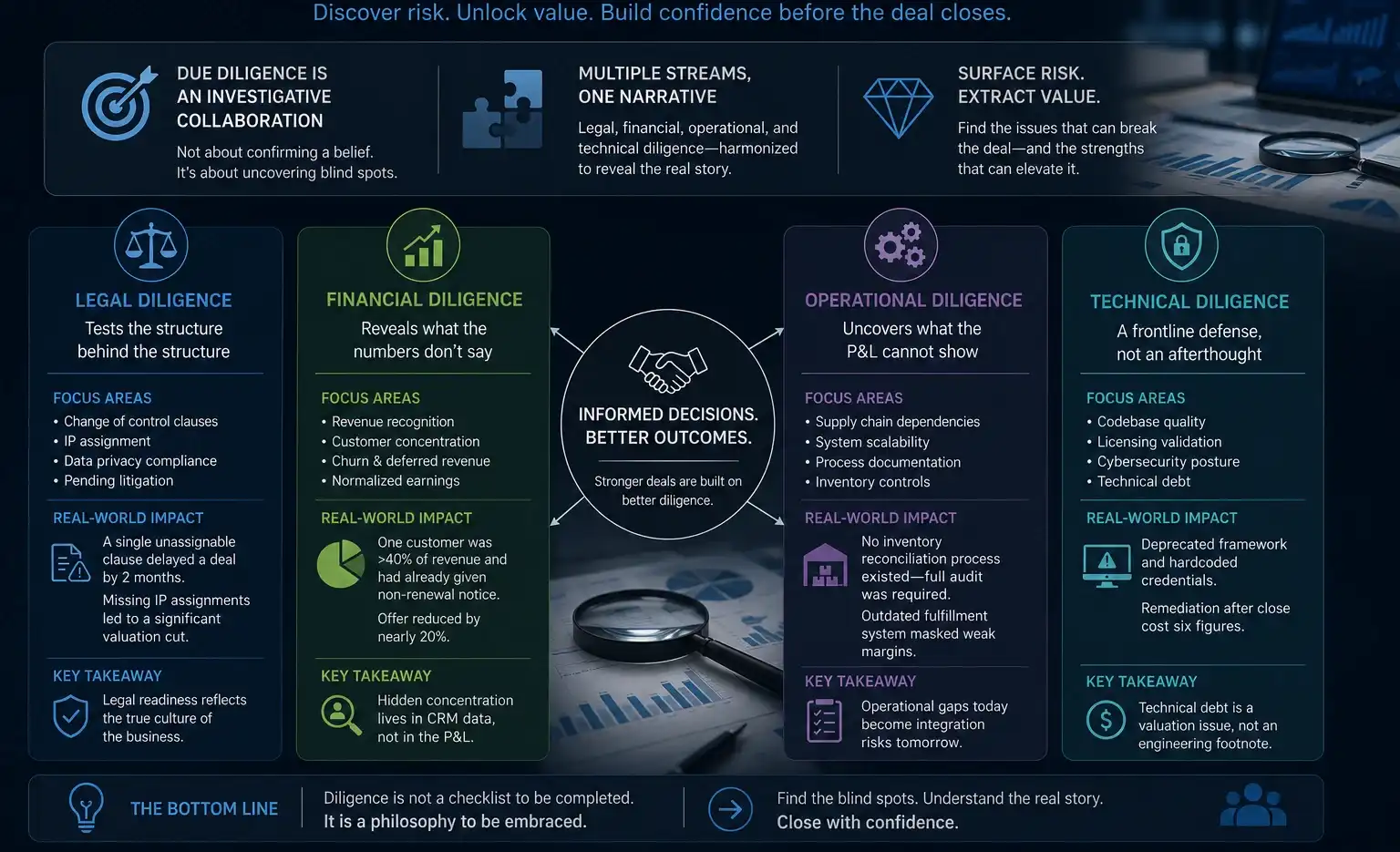

Diligence, done well, is less about confirming a belief. It is more about discovering a blind spot. It works best as an investigative collaboration rather than an adversarial process. Done right, it surfaces latent risk and extracts hidden value before a deal closes. Each stream, legal, financial, operational, and technical, reveals a different facet of a company’s real condition. Harmonized well, these streams build a coherent narrative buyers can trust. Left disjointed, they quietly signal fragility instead, no matter how strong the headline numbers look.

Legal Diligence Tests the Structure Behind the Structure

Legal review goes beyond entity charts and board minutes. It looks closely at change of control provisions and IP assignment gaps. Data privacy compliance and pending litigation both deserve the same scrutiny. One acquisition stalled for two months. The delay traced back to a single unassignable clause inside a key customer contract. A Series B company once faced a significant valuation cut for a similar reason. Missing IP assignments across its engineering team turned out to be structural, not accidental. Legal readiness reflects the broader culture of an organization far more than most teams expect.

Financial Diligence Reveals What the Numbers Do Not Say

Financial review must go beyond audited statements. Revenue recognition policy, churn, and deferred revenue all deserve close attention. Normalized earnings belong on that same list. In one SaaS transaction, a single customer represented over forty percent of trailing revenue. That customer had already given notice of non-renewal before the deal closed. The finding alone reduced the offer by nearly a fifth. Revenue concentration often hides inside CRM records rather than the profit and loss statement itself. That kind of hidden concentration has repeatedly reshaped retention strategy in later deals. It has also shaped the size of earnout holdbacks.

Operational Diligence Uncovers What the P&L Cannot Show

Operations carry real risk to integration success. Supply chain dependencies, system scalability, and process documentation all matter here. One consumer electronics acquisition needed a full inventory audit before it could proceed. Diligence had revealed that no reconciliation process existed at all. A separate direct to consumer brand told a different story. Its margins looked strong on paper. A lagging fulfillment process, traced back to an outdated system, told a different one entirely. Closing conditions were adjusted afterward. The new terms required a modernization roadmap before the deal moved further.

Technical Diligence Is a Frontline Defense, Not an Afterthought

Technical review has become essential in technology and IP heavy sectors. It is no longer optional in these deals. Codebase quality, licensing validation, and cybersecurity posture belong on the same scorecard as financial metrics. One artificial intelligence company relied heavily on a deprecated open source framework. Hardcoded credentials sat inside its own source code as well. Remediation after close still cost six figures. Technical debt, once uncovered this way, becomes a valuation issue. It stops being a footnote buried inside an engineering report.

Coordinating the Streams Instead of Working in Silos

The strongest diligence processes treat every stream as connected. Legal, financial, operational, and technical findings should never sit in isolation. A legal finding on revenue recognition should move straight to finance for validation. An operational gap should prompt a technical review of system readiness in turn. Weekly cross functional calls keep these threads aligned rather than drifting apart on their own.

| Diligence Stream | What It Uncovers | Example Impact |

| Legal | Contract enforceability, IP ownership, litigation exposure | Closing delay after an unassignable clause surfaced |

| Financial | Revenue quality, concentration risk, deferred revenue | Offer reduced after a major customer gave non-renewal notice |

| Operational | Process maturity, supply chain dependency, scalability | Closing condition added requiring a system upgrade |

| Technical | Code quality, licensing, cybersecurity posture | Six figure remediation after deprecated open source use |

A master risk register ties every finding to its financial, legal, or strategic impact. That register gives a board three real options for each item. A board can accept the risk, price it into the deal, or remediate it before close. This kind of structure turns diligence from a pile of separate reports into a single, actionable view of the entire deal. A few habits consistently keep this coordination effective:

- Score every finding on likelihood, materiality, and difficulty of remediation

- Route legal findings through finance before they reach a term sheet

- Treat technical debt as a pricing question rather than an engineering footnote

Diligence Preparation Is an Opportunity for Sellers

Sellers should treat due diligence preparation as a chance to control the narrative. It is an opportunity, not a hurdle to merely survive. A disciplined reverse diligence process works like a self audit. It lets a seller identify and explain anomalies before a buyer ever finds them independently. One founder built a short deck outlining known risks. The deck also covered the mitigation already in place and what remained open. That transparency shifted the entire tone of the negotiation. The deal ultimately closed at a premium because of it.

In another exit, thorough preparation cut over a month from the closing timeline. The buyer trusted the seller’s own data room enough to move quickly. Momentum, once earned this way, tends to protect valuation rather than erode it. Sellers who prepare early, through honest reverse diligence, close faster on average. They also tend to defend a stronger price, since transparency signals readiness rather than risk.

Conclusion

Business due diligence succeeds when it produces predictability rather than perfection. Each stream, legal, financial, operational, and technical, reveals a distinct piece of an organization’s real condition. Handled in isolation, these streams create blind spots. Those blind spots tend to surface at the worst possible moment in a transaction. Coordinated through a shared risk register, they become one coherent narrative instead. A board can act on that narrative with real confidence. Sellers who prepare early, through honest reverse diligence, tend to close faster. They also tend to defend a stronger price, since transparency signals readiness rather than risk. CFOs on either side of the table should treat this process as a strategic lever. It should never be delegated away entirely. What gets disclosed, priced, and indemnified during diligence shapes the outcome of the entire transaction. Approached with rigor and a clear narrative, diligence becomes a mirror. It shows what a company owns, and how clearly it understands its own worth.

Disclaimer: This blog is intended for informational purposes only and does not constitute legal, tax, or accounting advice. You should consult your own tax advisor or counsel for advice tailored to your specific situation.

Hindol Datta is a seasoned finance executive with over 25 years of leadership experience across SaaS, cybersecurity, logistics, and digital marketing industries. He has served as CFO and VP of Finance in both public and private companies, leading $120M+ in fundraising and $150M+ in M&A transactions while driving predictive analytics and ERP transformations. Known for blending strategic foresight with operational discipline, he builds high-performing global finance organizations that enable scalable growth and data-driven decision-making.

AI-assisted insights, supplemented by 25 years of finance leadership experience.