Executive Summary

How to prepare for an audit is a question most founders ask too late. Across three decades of finance leadership with venture-backed companies from Series A through Series D, spanning cybersecurity, SaaS, logistics, and medical devices, I have seen a consistent pattern: the companies that suffer through audits are not those with imperfect numbers. They are those with absent systems, incomplete documentation, and no established cadence for financial discipline. An audit is not a punishment. It is a structured reflection of how a company manages its financial reality. Founders and CFOs who internalize this early build organizations that close audits in weeks rather than months, preserve investor confidence during diligence, and approach each subsequent audit with operational ease. This guide outlines the core disciplines that make startup audit readiness less of a reaction and more of a repeatable practice.

Why Audits Arrive Sooner Than Founders Expect

Many founders assume that audits belong to late-stage companies, and the question of how to prepare for an audit rarely surfaces until an investor or acquirer forces the issue. That assumption is increasingly costly. Institutional investors now require audited financials as early as Series B, and some require reviewed statements at the close of a Series A. Strategic partners initiating large transactions often request financial assurance before proceeding. Acquirers in regulated verticals, particularly SaaS and fintech, will expect clean, auditable books as a baseline condition, not a negotiating point.

The cost of unpreparedness extends beyond the accounting fees. When documentation is scattered and systems are inconsistent, auditors spend more time requesting evidence and less time completing their review. Founders have watched term sheets disappear during that delay. Investor confidence has eroded. Credibility, once lost in a diligence process, is difficult to recover.

Audit readiness is a form of institutional trust. The earlier a founding team treats it as an ongoing discipline rather than a periodic event, the stronger that trust becomes.

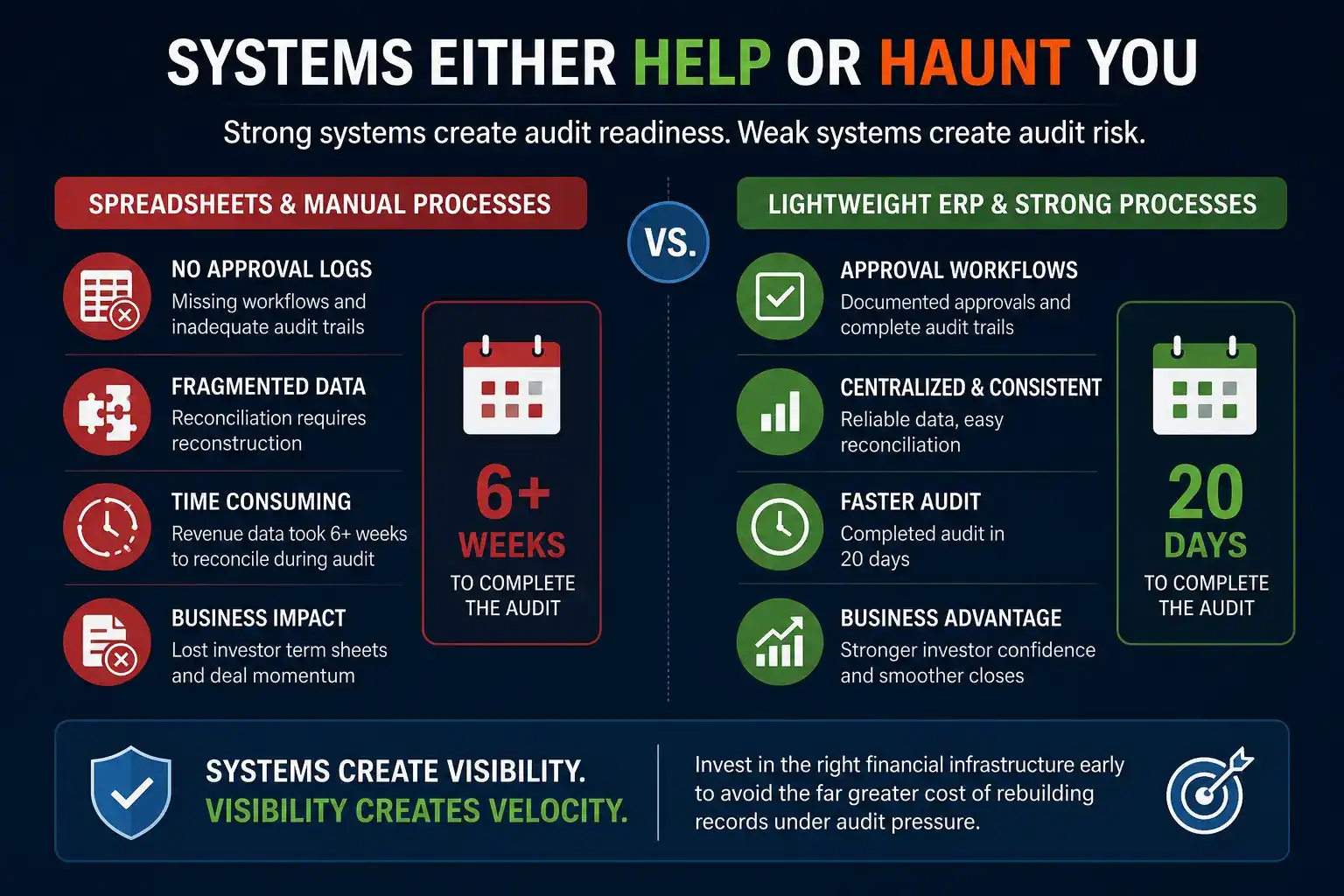

Systems Either Help or Haunt You

Most audit difficulties trace back not to accounting complexity but to system absence. When startups manage revenue, expenses, equity, or deferred revenue through spreadsheets, they create environments where approval logs disappear, audit trails fragment, and reconciliation demands reconstruction rather than retrieval.

During one engagement I led with a company approaching a Series C, the absence of a formal ERP system meant that a single year of revenue data took more than six weeks to reconcile during fieldwork. Two investor term sheets disappeared in that window. A comparable company that had implemented a lightweight ERP at Series A completed its audit in twenty days. The difference was not sophistication. It was structure.

Systems are not about administrative control. They are about visibility. And in an auditing a business context, visibility is what produces velocity.

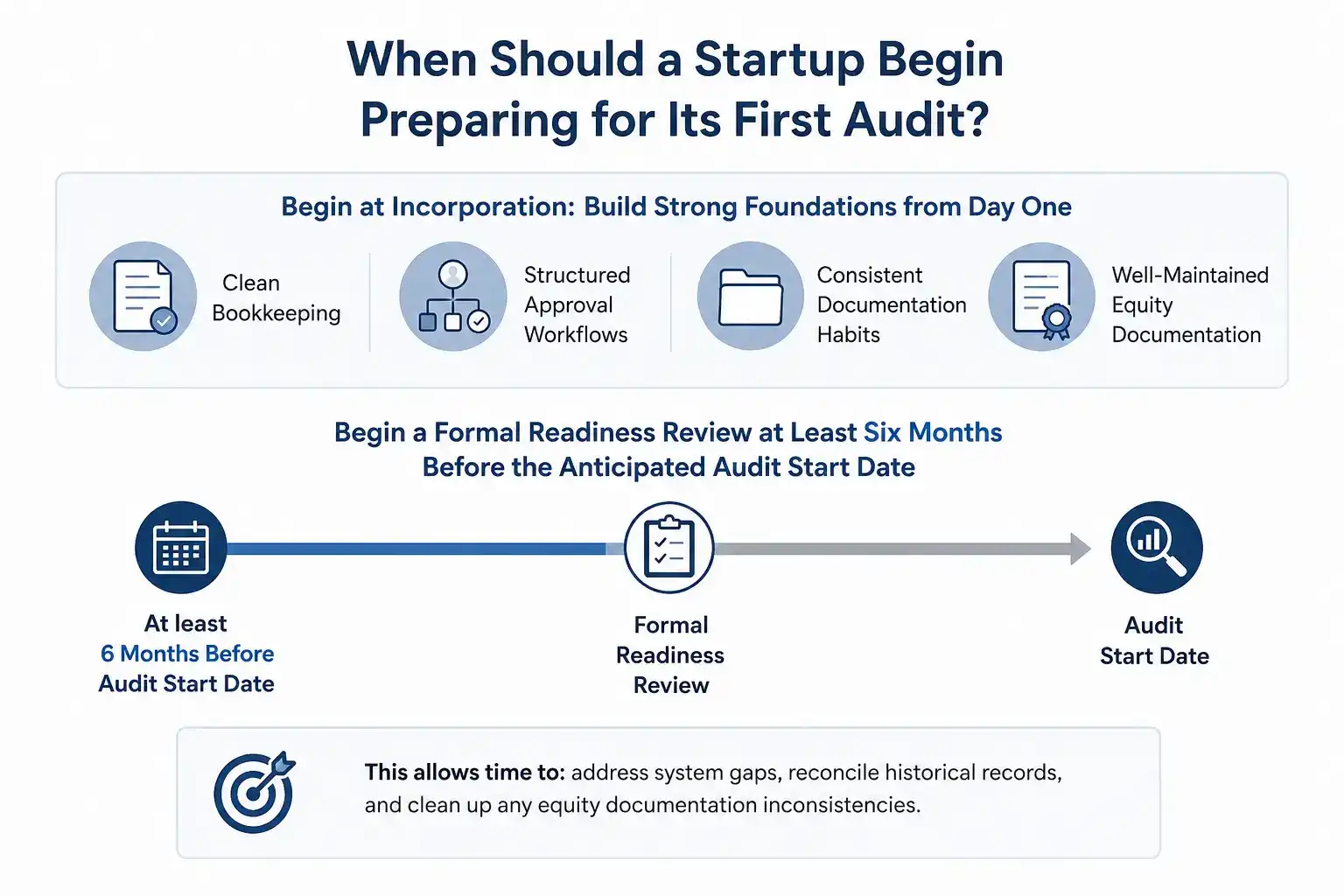

Choosing the Right Financial Infrastructure Early

The right system does not need to be expensive. What it needs to do is maintain a clean chart of accounts, retain approval workflows, produce consistent period-end reports, and support revenue recognition under the applicable accounting standard. A company that makes this investment before its first institutional raise avoids the far greater cost of rebuilding records under audit pressure.

The Audit Readiness Checklist

The table below outlines the core areas auditors examine in a startup audit, the documentation they expect to find, and the recommended preparation frequency.

| Audit Area | What Auditors Expect | Preparation Frequency |

| Revenue recognition | Executed contracts, delivery evidence, ASC 606 policy | Monthly |

| Expense documentation | Approved invoices, receipts, GL coding consistency | Monthly |

| Equity and cap table | Board-approved grants, signed agreements, 409A valuations | Per issuance, annual review |

| Bank reconciliations | Reconciled statements matching GL balances | Monthly |

| Deferred revenue | Rollforward schedule with supporting contracts | Quarterly |

| Related party transactions | Disclosed agreements, arm’s length documentation | As incurred |

| Legal and compliance | Entity status, material contracts, insurance certificates | Annual |

Building a review cadence around these areas, before any audit is formally announced, removes the scramble entirely. When the prepared-by-client list arrives, a well-prepared finance team responds within days rather than weeks.

Documentation as a Daily Discipline

One of the most practical mental shifts a finance leader can model for the broader team is to document every material transaction as if an unfamiliar reviewer will examine it. That mindset changes how contracts are saved, how approvals are recorded, and how exceptions are communicated.

When a bonus goes out, the board or compensation committee approval must be on file. A closed contract requires the final signed version in a structured drive. Supporting evidence for recognized revenue must align with the stated recognition policy. Auditors do not audit intentions. They audit paper trails. The stronger the trail, the faster the audit moves.

A quarterly internal review that simulates a basic document request is one of the most cost-effective preparation tools available to a startup finance team. It surfaces gaps in real time, when they are still easy to close. Many of the most common audit delays I have observed over three decades of finance leadership were caused not by complex accounting issues but by a simple failure to save the right file in the right place at the right time That failure is entirely preventable with the right internal habits in place well before any external review begins.

Equity Records: The Most Underestimated Audit Flashpoint

Equity documentation consistently creates the most avoidable audit delays. Option grants without board approval, mismatches between the cap table and the equity ledger, 409A valuations that do not align with grant dates, and informal equity promises that were never formalized in writing can each add weeks to a fieldwork timeline.

The most audit-ready startups handle equity with the same rigor they apply to revenue. They use dedicated cap table management tools, ensure every grant is matched to a board resolution, and involve legal counsel at each issuance. This may feel formal for an early-stage company. But in a startup audit, that formality becomes a direct source of speed.

If records are inconsistent, the time to begin cleanup is now, not when the auditors request the first schedule.

Working With Auditors as Strategic Partners

Auditors are not adversaries. The companies that move through audits most efficiently are those whose leadership teams engage early, explain the business model clearly, and communicate material changes before fieldwork begins.

Walking an audit lead through a new product line, a geographic expansion, or a recent financing event provides context that shapes the entire review. The more an audit team understands the business, the more efficiently they can focus their work. The less they understand, the more conservative and time-intensive the process becomes.

I have seen audit timelines extend by weeks simply because a company’s revenue model changed between periods and no one communicated that change at the outset of fieldwork. Auditors who encounter surprises during fieldwork become cautious. Auditors who receive proactive context become efficient. The difference in calendar time can determine whether a financing round closes on schedule or stalls while investors wait for the final report. Transparency with auditors is not a risk. It is a strategy.

Conclusion

How to prepare for an audit is ultimately a question about how seriously a founding team takes its own financial discipline. Audits do not create problems. They reveal them. The companies that emerge from audits with momentum intact are those that have treated financial rigor as a strategic input rather than a compliance obligation. This means investing in the right systems early, maintaining documentation as a daily practice, keeping equity records precise, and engaging with auditors as informed partners rather than necessary inconveniences. Across every sector and stage I have worked in, from early-stage medical device companies to SaaS businesses scaling through institutional rounds, the best outcomes shared a single common thread: the team never left preparation to the last quarter. They built it into the rhythm of the business from the beginning.

Disclaimer: This blog is intended for informational purposes only and does not constitute legal, tax, or accounting advice. You should consult your own tax advisor or counsel for advice tailored to your specific situation.

Hindol Datta is a seasoned finance executive with over 25 years of leadership experience across SaaS, cybersecurity, logistics, and digital marketing industries. He has served as CFO and VP of Finance in both public and private companies, leading $120M+ in fundraising and $150M+ in M&A transactions while driving predictive analytics and ERP transformations. Known for blending strategic foresight with operational discipline, he builds high-performing global finance organizations that enable scalable growth and data-driven decision-making.

AI-assisted insights, supplemented by 25 years of finance leadership experience.