Executive Summary

A bridge round is one of the most revealing moments in a company’s capital journey. It forces founders and leadership teams to confront the gap between strategy and execution with unusual clarity. When structured with discipline, bridge round funding extends a company’s runway toward a defined, measurable inflection point. When pursued reactively, it becomes a costly delay dressed as a decision. This article examines what a bridge round truly is, why the cost extends well beyond dilution, and how executives can build and execute a bridge with the rigor the moment demands. Drawing on more than two decades of capital markets experience across cybersecurity, SaaS, logistics, digital marketing, and gaming, the insights here are grounded in the practical mechanics of companies that navigated bridges effectively and those that did not. The central argument is simple: a bridge is not a rescue. It is a design decision, and it deserves to be treated as one.

What a Bridge Round Actually Is

In the most precise sense, a bridge round is a financing event designed to extend a company’s runway between two larger, more formal fundraises. It is not a standalone capital strategy. It is a connector, intended to carry the company from its current position to a defined milestone that will support the next institutional round. The form it takes varies: a convertible note, a SAFE, or a small priced equity round. The purpose, however, is consistent. It buys time.

What distinguishes a well-conceived bridge from a poorly executed one is whether the leadership team knows specifically what that time is intended to buy. Bridge rounds that are raised without this clarity tend to recycle the same fundamental problems under a new layer of capital. More runway without better direction is not a solution. It is postponement.

This distinction matters enormously from an investor’s perspective. Venture capital operates on portfolio logic. Every dollar deployed to an existing company is a dollar not deployed elsewhere. When a bridge is presented to an investor, they are not simply evaluating the company in isolation. They are assessing whether this allocation, at this moment, is the most productive use of their remaining reserve capacity. A founder who understands this will come to the conversation prepared to justify not just the ask, but the opportunity cost.

The Real Cost of a Bridge Round

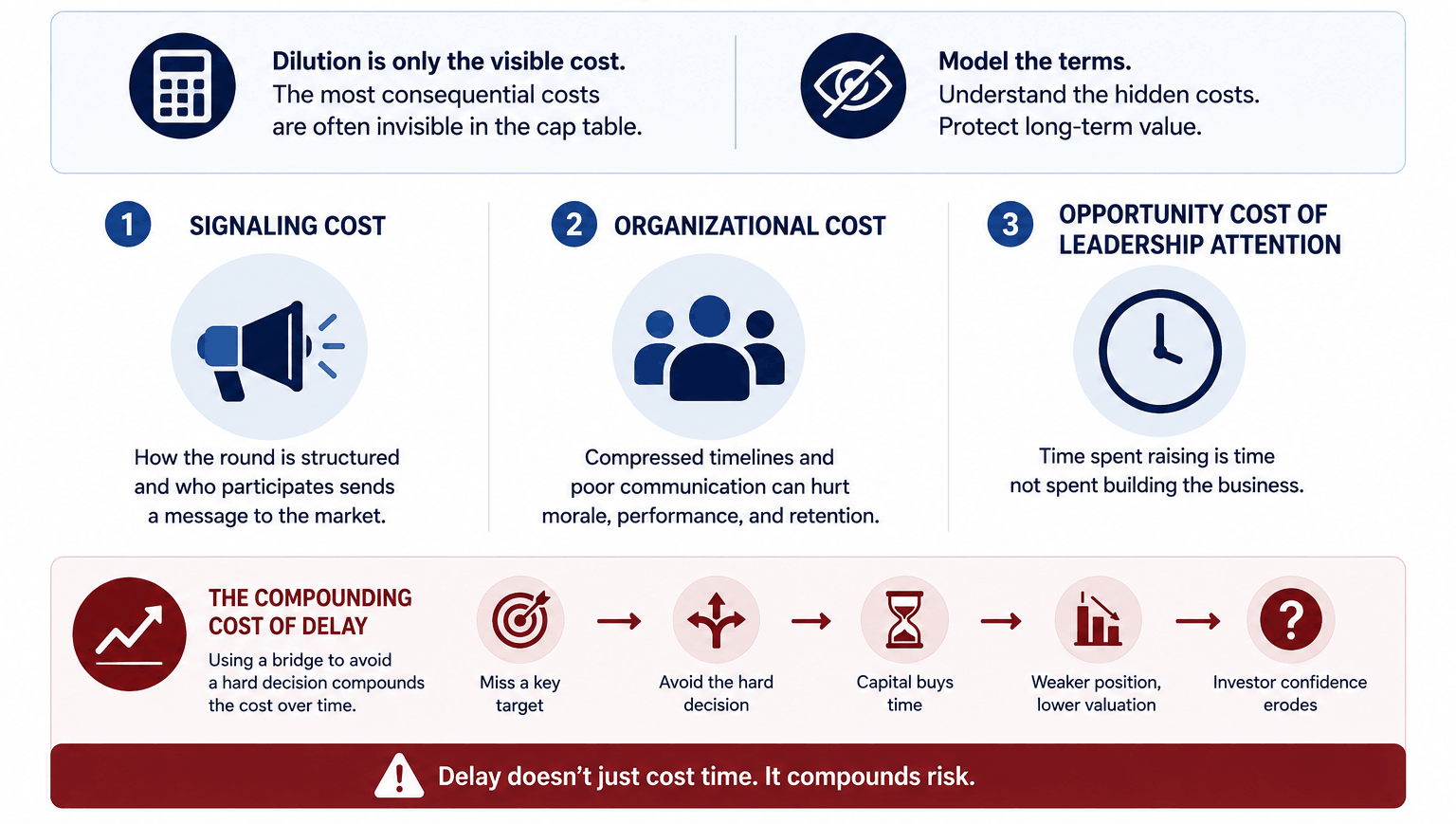

Beyond Dilution

Most discussions of bridge round cost begin and end with dilution. That is the visible and quantifiable dimension. A convertible note with a valuation cap and a discount translates into ownership transfer at conversion. Warrants and liquidation preference stacking add further complexity. These are real costs, and any founder or CFO who does not model them across multiple valuation scenarios before accepting terms is taking on unnecessary risk.

But the more consequential costs are often invisible in the cap table.

The first is signaling cost. How a bridge round is structured and communicated sends a message to the broader investor market. A round led by an existing institutional investor who is increasing their position signals conviction. A round composed of small checks from angels and advisors, assembled under time pressure, signals something entirely different. Future investors will ask who participated and why. The answer shapes the due diligence narrative before a single conversation occurs.

The second is organizational cost. Bridge rounds compress timelines and sharpen priorities in ways that can either clarify or fracture a team. When leadership does not communicate the reason for the bridge with transparency, employees fill the information gap with speculation. Performance suffers. Key personnel begin to evaluate their options. The cultural cost of a poorly messaged bridge can outlast the financial cost by months.

The third is the opportunity cost of leadership attention. Raising a bridge is not a passive process. It consumes founder and executive bandwidth at precisely the moment when the business requires their full focus. Every week spent in investor meetings and legal review is a week not spent closing customers, fixing product gaps, or stabilizing operations.

The Compounding Cost of Delay

There is one more dimension that deserves particular attention: the cost of using a bridge to avoid a hard decision.

In my work across organizations of varying scale and sector, I have seen this pattern repeatedly. A company misses a key performance target. Rather than facing the implications of that miss directly, whether through a strategic pivot, a workforce restructuring, or an honest conversation with the board, leadership opts for a bridge. The capital buys time. But the underlying problem is not addressed. Six months later, the company is in a structurally weaker position, with less negotiating leverage, a lower implied valuation, and investors who are now questioning whether the leadership team has the judgment to navigate difficulty.

The compounding cost of delay is not linear. It accelerates. And it is one of the most important concepts I draw on when advising leadership teams in capital planning.

When a Bridge Round Is the Right Move

Not every bridge is a warning sign. Some are legitimate and well-timed extensions of a staged capital plan. The following conditions tend to characterize a bridge that is worth pursuing:

- The company has reached a defined operational milestone but the next institutional round is delayed due to market timing or investor process, not performance concerns.

- Leading indicators, specifically pipeline velocity, sales cycle compression, and gross margin trajectory, show clear and documentable improvement.

- Existing investors are participating, at least in part, which demonstrates continued conviction rather than passive tolerance.

- The capital requirement is specific, the deployment plan is detailed, and the outcome that triggers the next round is measurable.

- The leadership team can articulate not just what went wrong in the previous period, but what has structurally changed and why the bridge leads to a different outcome.

That last point deserves particular emphasis. Investors are not afraid of setbacks. They are afraid of leadership teams that cannot honestly diagnose them. A founder who says, “We missed our Q2 ARR target by 18 percent, but our net revenue retention improved to 112 percent and our enterprise conversion rate has increased meaningfully over the last two quarters” is telling a credible story. That is fundable. Narrative without data is not.

How to Structure a Bridge with Integrity

Aligning Capital to Milestones

The most important structural principle in bridge financing is milestone alignment. The capital plan must be reverse-engineered from the outcome, not forward-projected from the ask. If the goal is to reach a specific ARR threshold before raising a Series B, every deployment decision should trace back to that objective.

This means the bridge capital plan should include:

- A monthly cash flow projection broken into use-of-funds categories

- Scenario-based modeling that distinguishes between base, downside, and upside outcomes

- A clear statement of what milestone unlocks the next round and a realistic timeline to reach it

- A defined set of leading indicators that will be tracked weekly and reported to the board

In my experience building financial operating models across sectors as varied as identity security, gaming, and medical devices, the organizations that manage bridge capital most effectively are those that treat the bridge period as a compressed version of their normal operating cadence, with higher frequency reporting, tighter spend controls, and more disciplined OKR reviews.

When I led the finance function at a high-growth digital marketing company that scaled from nine million to one hundred and eighty million dollars in revenue, the discipline of connecting every capital allocation to a measurable output was foundational. That principle applies with even greater force when a company is operating under the constraints of bridge financing.

Cap Table and Terms Discipline

Bridge rounds frequently involve convertible instruments. This creates flexibility in the short term but can introduce complexity at conversion if terms are not negotiated with discipline.

Founders should model dilution at multiple valuation scenarios, specifically at the valuation cap, at the anticipated Series B price, and at a downside scenario below both. Warrants, if demanded by investors, should be evaluated as part of the total cost of capital, not as an add-on. Multiple liquidation preferences stack against founder and employee equity at exit. These terms matter not just for the current round but for how subsequent investors will read the cap table.

The signaling effect of terms is also real. A bridge structured at a steep discount with aggressive downside protections may communicate something to the next investor that the founder did not intend. Clean, simple terms that reflect a genuine shared belief in the near-term outcome are almost always preferable.

The Internal Execution Imperative

Once the bridge is closed, the real test begins. Capital is not the deliverable. Execution is.

The bridge period demands a specific operating rhythm. Weekly OKR reviews tied to cash deployment. Monthly board updates that are data-first, with variance analysis against the original deployment plan. A willingness to adjust tactics quickly when early signals indicate a hypothesis is not holding.

This is where finance leadership earns its keep. Not in the fundraising conversation, but in the weeks that follow. Building the operational infrastructure to track bridge-period performance requires clarity on which metrics matter most under pressure. In my work designing KPI frameworks and BI systems, I have consistently found that the most useful metrics in a constrained capital environment are leading indicators, not lagging ones. Pipeline velocity and cohort-level churn are more actionable than revenue totals because they tell you what is coming before it arrives in the income statement.

Internal communication is equally critical. The team will know something significant has happened. The leadership decision is not whether to communicate but how. A bridge framed as a strategic capital stage aligned with specific outcomes, with a clear explanation of what the company is building toward, preserves morale and focus. A bridge that is treated as a confidential matter or explained only vaguely tends to generate the speculation it was designed to prevent.

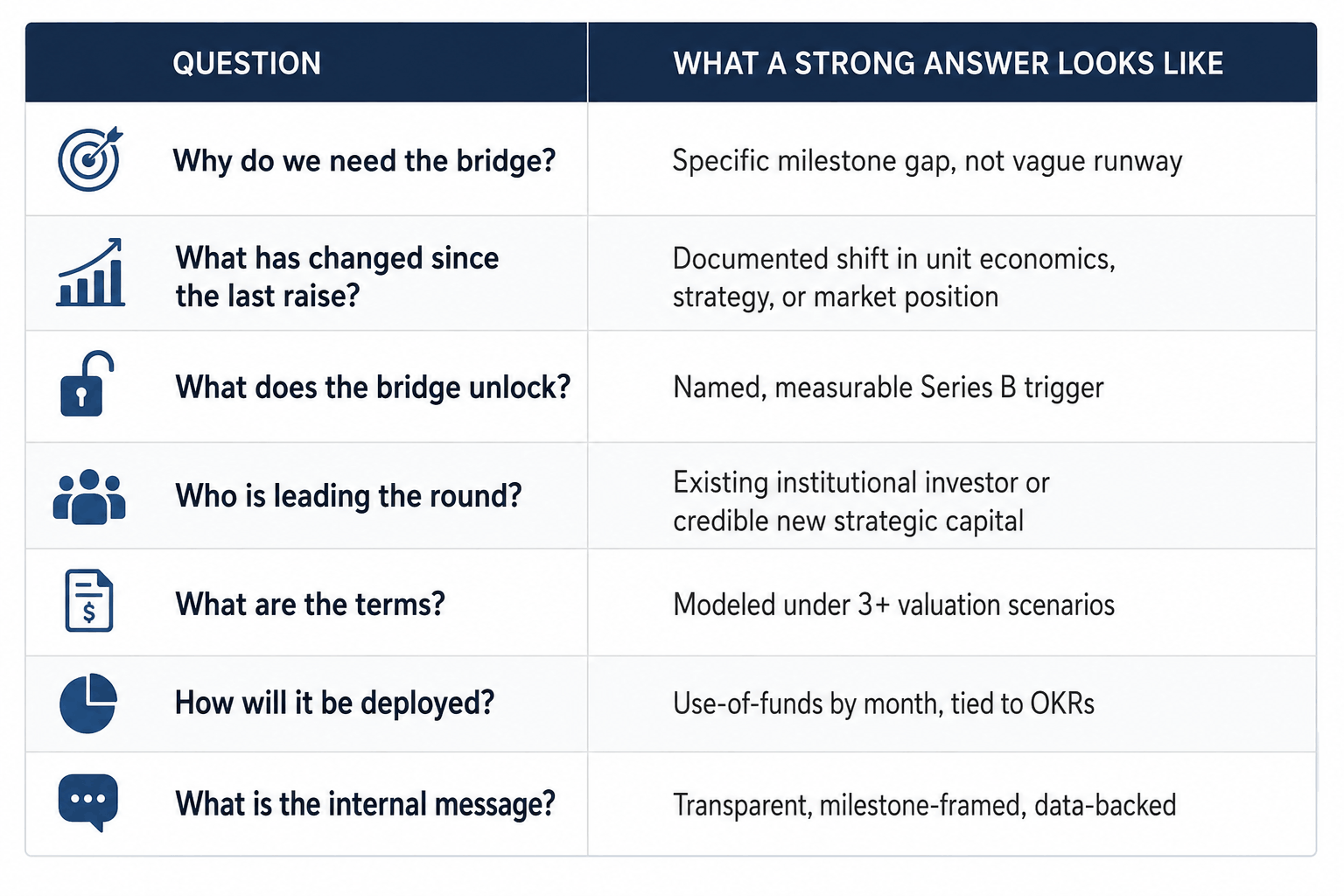

A Decision Framework for Bridge Rounds

The following framework may assist leadership teams in evaluating whether a bridge is appropriate and how to approach it:

No framework replaces judgment. But a leadership team that can answer each of these questions with specificity before approaching investors is in a fundamentally stronger position than one that cannot.

Conclusion

A bridge round is not a verdict on the company. It is a test of the leadership team’s clarity, honesty, and operational discipline. The executives who navigate it well are those who face the numbers directly, communicate with transparency, structure terms with strategic discipline, and treat the bridge period as an accelerant rather than a reprieve. Over two decades of working at the intersection of capital markets and operating execution, across sectors ranging from cybersecurity and SaaS to gaming and logistics, I have seen this distinction play out consistently. The bridge itself is neutral. What the company does with it is not. Founders and CFOs who approach it with rigor, humility, and a well-constructed plan earn the trust of their investors and the loyalty of their teams. Those who treat it as a delay tend to find that time, like capital, is finite, and that both run out at the same moment.

Disclaimer: This blog is intended for informational purposes only and does not constitute legal, tax, or accounting advice. You should consult your own tax advisor or counsel for advice tailored to your specific situation.

Hindol Datta is a seasoned finance executive with over 25 years of leadership experience across SaaS, cybersecurity, logistics, and digital marketing industries. He has served as CFO and VP of Finance in both public and private companies, leading $120M+ in fundraising and $150M+ in M&A transactions while driving predictive analytics and ERP transformations. Known for blending strategic foresight with operational discipline, he builds high-performing global finance organizations that enable scalable growth and data-driven decision-making.

AI-assisted insights, supplemented by 25 years of finance leadership experience.