Executive Summary

For startups entering European markets, understanding VAT for startups is not a back-office formality. It is a structural requirement that shapes pricing, invoicing, cash flow, and go-to-market execution from the first transaction. Yet many founding teams, particularly those schooled in U.S. tax logic, arrive underprepared. The mechanisms differ fundamentally. The stakes are higher. And the penalties for inattention are real. This guide walks through how value-added tax works across European jurisdictions: what triggers registration, how input tax recovery generates real financial advantage, what reporting obligations actually demand of a finance team, and why companies that treat it as a strategic function scale more cleanly than those that relegate it to administration and later spend capital on remediation. For CFOs navigating cross-border growth, readiness on this front is not optional. It is foundational.

Why VAT Catches Startups Off Guard

Most early-stage companies built in the United States carry a mental model of tax that does not survive contact with Europe. In the U.S., sales tax is a point-of-sale addition, calculated after the transaction, collected from the buyer, and remitted to the state. It is visible, discrete, and relatively straightforward to administer.

VAT for startups entering Europe operates on entirely different logic. It embeds itself in every stage of the value chain. EU-wide directives and each member state’s own implementing rules govern it simultaneously, creating a layered compliance environment that no single jurisdiction fully controls. And it applies not just to finished goods sold to consumers, but to B2B services, digital products, cross-border transactions, and in many cases, to activities that a U.S.-trained finance team would not immediately recognize as taxable events.

Having led finance functions across SaaS platforms, logistics operations, digital marketing firms, and cybersecurity organizations, I have seen this gap repeatedly. It is not a failure of intelligence. It is a failure of frame. The companies that close that gap early build with leverage. The ones that do not spend months unwinding errors.

The Mechanics of EU VAT

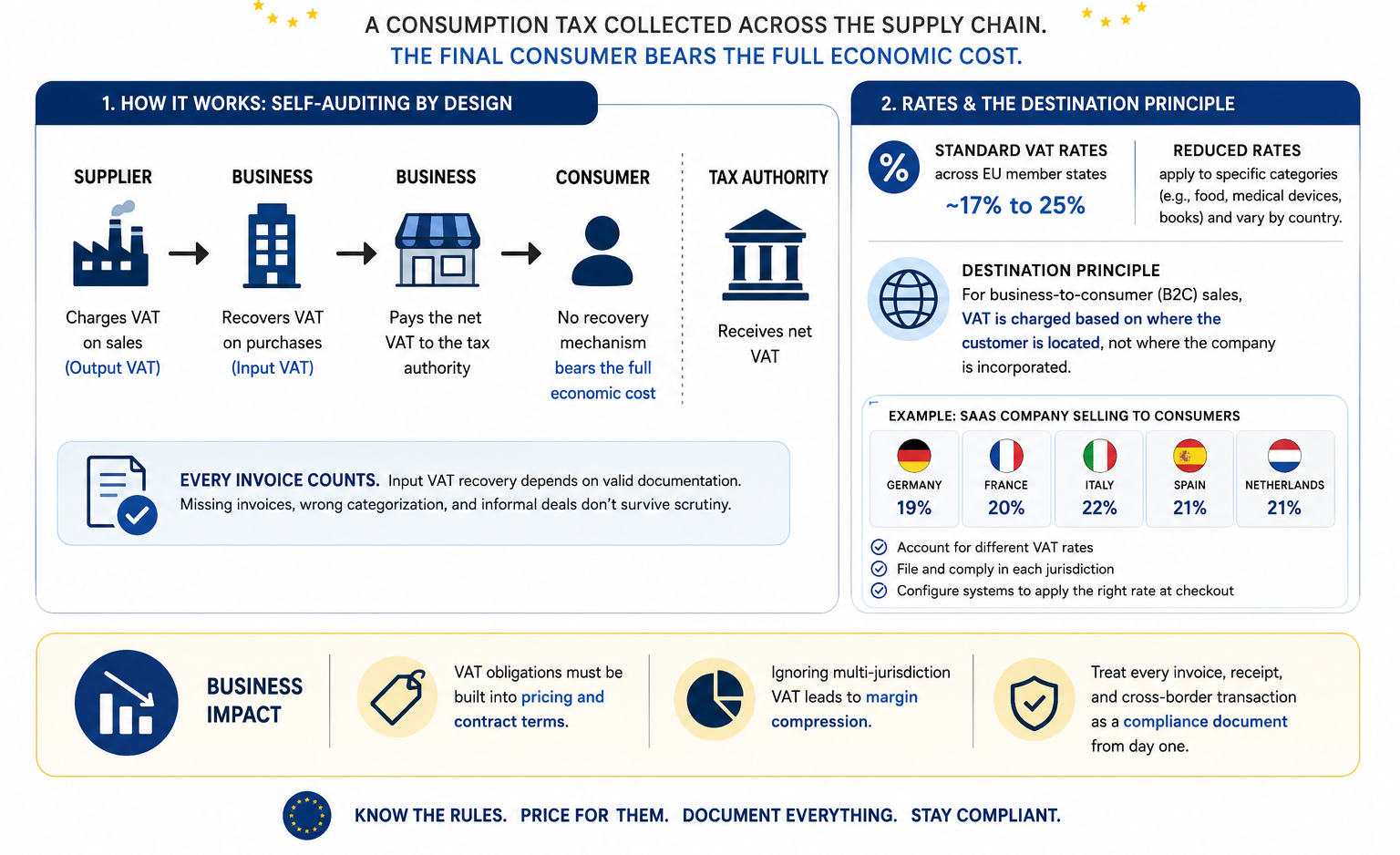

Value-Added Tax is a consumption tax that moves incrementally through the supply chain. Each business charges VAT on its sales, known as output VAT, and recovers VAT on its purchases, known as input VAT. The business then remits the net difference to the tax authority. The final consumer bears the full economic cost because they have no mechanism to recover it.

This self-auditing structure is one reason EU tax authorities enforce it with confidence. Every participant in the chain has an incentive to document what they paid, because that documentation is the basis for their own recovery claim. Missing invoices, miscategorized transactions, and informal arrangements do not survive scrutiny.

For a startup entering this environment, that means treating every vendor invoice, every customer receipt, and every cross-border transaction as a compliance document from the beginning.

Rates, Jurisdictions, and the Destination Principle

Standard VAT rates across EU member states range from roughly seventeen percent to twenty-five percent. Reduced rates apply in specific categories, including certain food items, medical devices, and books, but these categories are not uniform across jurisdictions.

The governing principle for determining which rate applies to a given transaction is the destination principle. For business-to-consumer sales, VAT is charged based on where the customer is located, not where the company is incorporated. A SaaS platform serving consumers across five EU countries must account for five different VAT rates, file in each jurisdiction, and configure its billing system to handle the variation.

This has direct implications for pricing strategy. Gross margins that hold in a single-jurisdiction model will compress the moment layered VAT obligations go unaccounted for in product pricing and contract terms.

When Registration Is Required

VAT registration is triggered by activity, not by profitability. A company can be pre-revenue and still have registration obligations depending on how it is structured. The most common triggers include:

- Selling goods or services to customers within a given EU country

- Storing inventory in-country, including through third-party fulfillment centers

- Employing staff or operating a branch within a jurisdiction

- Exceeding distance-selling thresholds on cross-border consumer sales

For digital services and SaaS providers, the threshold question is particularly important. The EU introduced a harmonized distance-selling threshold of ten thousand euros in annual cross-border B2C revenue across the EU. Once that threshold is crossed, the destination-based VAT rules apply in full.

The One Stop Shop Regime

Registering individually in every EU country is administratively heavy. To address this, the EU introduced the One Stop Shop (OSS) framework. Under OSS, a company registers in a single member state and files one consolidated VAT return. That return covers all EU B2C sales. This is a meaningful simplification for SaaS platforms, content services, and digital marketplaces.

However, OSS does not cover all scenarios. Business-to-business transactions, physical goods that require local warehousing, and marketplace seller arrangements typically require country-level registrations in addition to or instead of OSS. The choice between a centralized OSS approach and a multi-entity structure carries both compliance and operational consequences. Finance leaders should evaluate it deliberately, not arrive at it by default.

The Reverse Charge Mechanism

For B2B transactions within the EU, the reverse charge mechanism shifts the VAT reporting obligation from the seller to the buyer. When both parties hold VAT registration, the seller issues an invoice without charging VAT, and the buyer self-assesses the tax on their own return. No cash changes hands, but both parties must document the transaction correctly.

This mechanism is useful in that it reduces the seller’s administrative burden across jurisdictions. But it requires precision. The invoice must explicitly reference the reverse charge. Both parties must be VAT-registered. And the transaction must qualify under the applicable rules. Errors at this stage do not disappear. They accumulate until an audit surfaces them.

Input VAT and the Case for Early Registration

One of the most underappreciated aspects of the VAT system for startups is the input VAT recovery mechanism. Companies can offset any VAT paid on qualifying business expenses against the VAT liability on sales. That means vendor invoices, software subscriptions, professional services, and other operating costs that carry VAT represent recoverable amounts, provided the company holds a valid registration and documents the expenses correctly.

For a pre-revenue or early-revenue company incurring meaningful operational costs in Europe, this creates a direct financial argument for registering earlier than strictly required. Some jurisdictions allow retroactive registration, giving companies the opportunity to claim input VAT on historical purchases, but the process demands careful documentation and a considered approach.

What Cannot Be Recovered?

Not all input VAT is recoverable. Entertainment expenses, certain vehicle costs, and costs with partial business use are subject to restrictions that vary by country. Companies that do not distinguish between recoverable and non-recoverable input VAT in their accounting systems often find themselves overstating their VAT position, which raises flags during compliance reviews and due diligence.

Across finance transformations I have led, from a logistics operation managing over one hundred and twenty million dollars in revenue to a cybersecurity organization with multi-entity global architecture, one finding has been consistent. Acquirers and auditors examine input VAT records among the first things they review. They are a proxy for the quality of the overall finance function.

VAT Returns and Reporting Obligations

Once registered, companies file periodic VAT returns on a monthly, quarterly, or annual basis depending on the jurisdiction and activity volume. These returns reconcile output VAT with input VAT incurred. The net balance is then either paid to the tax authority or claimed as a refund.

VAT returns are not summary documents. They require transaction-level detail: customer identification numbers, invoice references, applicable rates, and documentation supporting any cross-border treatment. Several EU jurisdictions now require real-time or near-real-time reporting, electronic invoicing mandates, or submission of Standard Audit Files for Tax.

The Consequences of Non-Compliance

Late filings, underpayments, and documentation failures do not go unnoticed. Most jurisdictions apply penalties on fixed schedules, and in the most serious cases, tax authorities deny input VAT claims retroactively. When a company is growing rapidly across multiple markets simultaneously, the temptation to delegate VAT filings without oversight is understandable. The consequences of doing so are not.

Centralizing VAT tracking within a capable ERP or finance stack is not an optional upgrade. It is the operational foundation that makes compliance scalable. In building finance organizations across SaaS, digital marketing, and professional services environments, the finance teams that struggled most with cross-border expansion were almost always the ones running VAT on spreadsheets long after the business had outgrown them.

VAT as a Strategic Function

Go-to-Market Implications

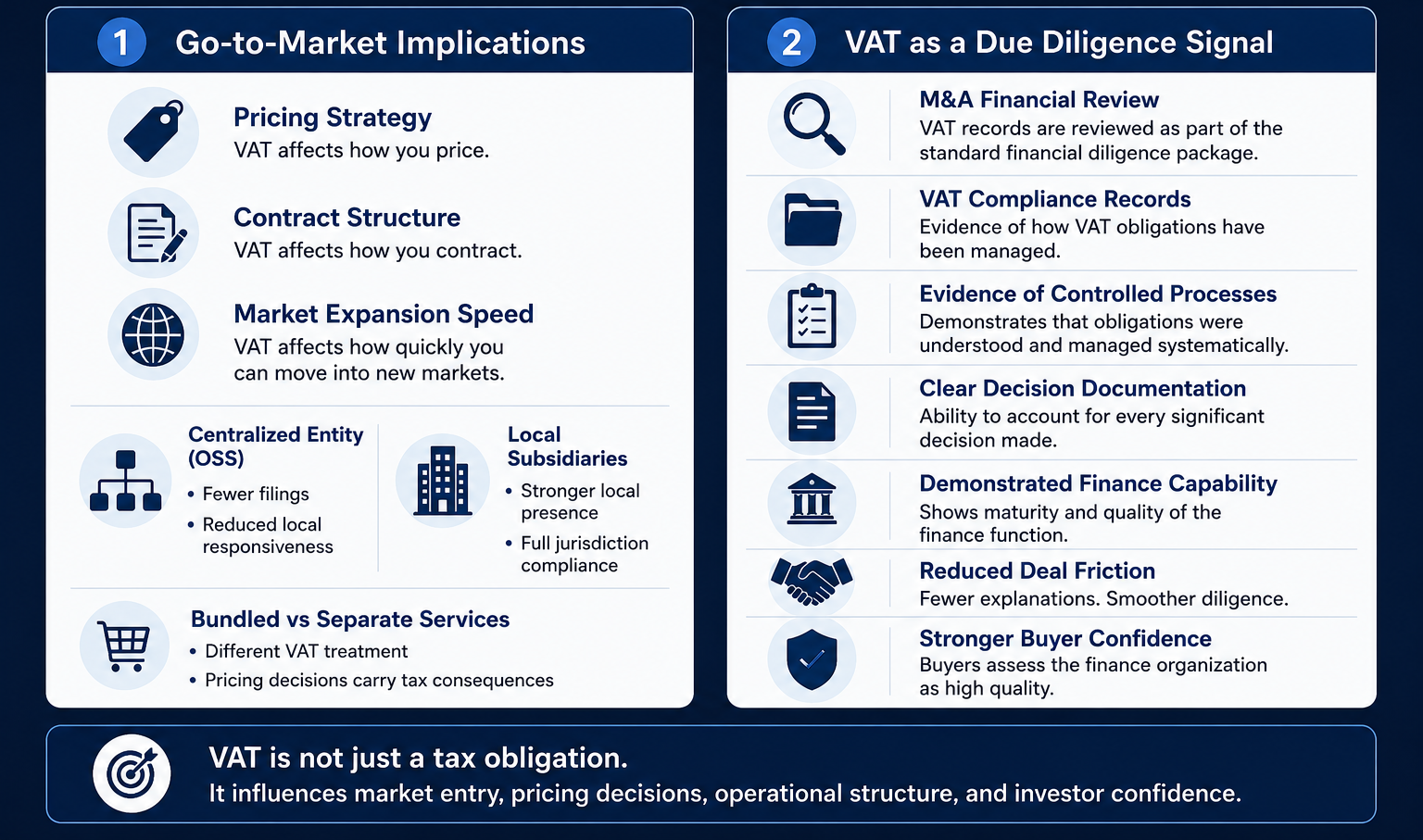

VAT is not just a cost. It is a variable that affects how you price, how you contract, and how quickly you can move into new markets. A company that discovers its VAT obligations only after signing its first European enterprise contract is already behind.

The decision between serving Europe from a centralized entity versus establishing local subsidiaries carries different VAT implications. Centralized models with OSS may reduce filing frequency but can limit local market responsiveness. Localized entity structures may offer operational advantages and cleaner regulatory relationships but require full VAT compliance in each jurisdiction.

Bundled pricing, volume discounts, and hybrid service arrangements also affect how VAT is calculated and reported. A software license bundled with implementation services may be subject to different VAT treatment than each component sold separately. These are not accounting technicalities. They are pricing decisions that must be made with full awareness of their tax consequences.

VAT as a Due Diligence Signal

In every M&A process I have participated in, across transactions totaling over one hundred and fifty million dollars, VAT records are reviewed as part of the standard financial diligence package. What auditors and acquirers are looking for is not perfection. They are looking for evidence that the finance function understood its obligations, managed them systematically, and can account for every significant decision made.

Companies that have treated VAT compliance as an afterthought spend the diligence phase explaining gaps rather than demonstrating capability. That has a cost, both in terms of deal friction and in terms of how buyers assess the quality of the broader finance organization.

Conclusion

VAT compliance is the kind of obligation that rewards companies for treating it seriously early and penalizes those who defer it until the cost of remediation is higher than the cost of getting it right from the start. For startups entering European markets, the question is not whether VAT applies. In most cases, it does. The question is whether the finance function is structured to handle it deliberately. That means mapping customer locations and transaction types before the first invoice goes out, configuring billing and ERP systems for jurisdiction-specific treatment, establishing clear processes for input VAT recovery, and building the reporting infrastructure that audits and acquirers will eventually examine. VAT readiness does not require a large team. It requires clear thinking, capable systems, and the organizational discipline to treat compliance as a function that serves strategy, not one that competes with it.

Disclaimer: This blog is intended for informational purposes only and does not constitute legal, tax, or accounting advice. You should consult your own tax advisor or counsel for advice tailored to your specific situation.

Hindol Datta is a seasoned finance executive with over 25 years of leadership experience across SaaS, cybersecurity, logistics, and digital marketing industries. He has served as CFO and VP of Finance in both public and private companies, leading $120M+ in fundraising and $150M+ in M&A transactions while driving predictive analytics and ERP transformations. Known for blending strategic foresight with operational discipline, he builds high-performing global finance organizations that enable scalable growth and data-driven decision-making.

AI-assisted insights, supplemented by 25 years of finance leadership experience.