Executive Summary

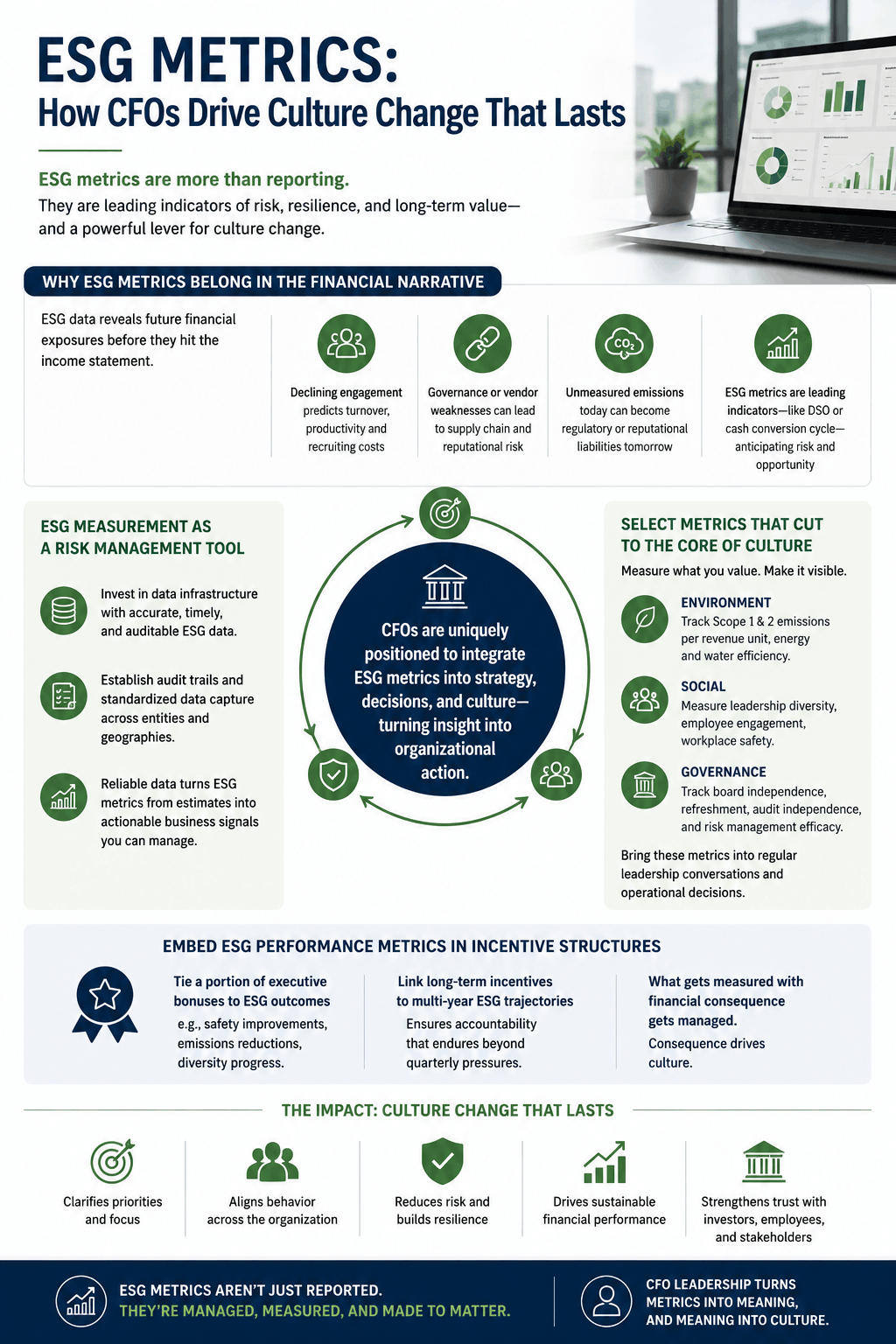

ESG metrics have crossed the threshold from compliance formality to a strategic instrument. For the CFO, they represent something more than a reporting obligation: they are leading indicators of financial exposure, organizational resilience, and long-term value. Carbon intensity, board independence ratios, leadership diversity data, and workplace safety trends each carry signals that a well-constructed financial model cannot afford to ignore. The CFO who embeds these measures into incentive structures, capital allocation decisions, and regular management rhythms does not simply satisfy an investor audience. That CFO reshapes what the organization pays attention to, which in turn reshapes how it behaves. Culture follows consequence. This article explores how finance leaders can use ESG metrics to drive genuine, measurable culture change across an organization.

Why ESG Metrics Belong in the Financial Narrative

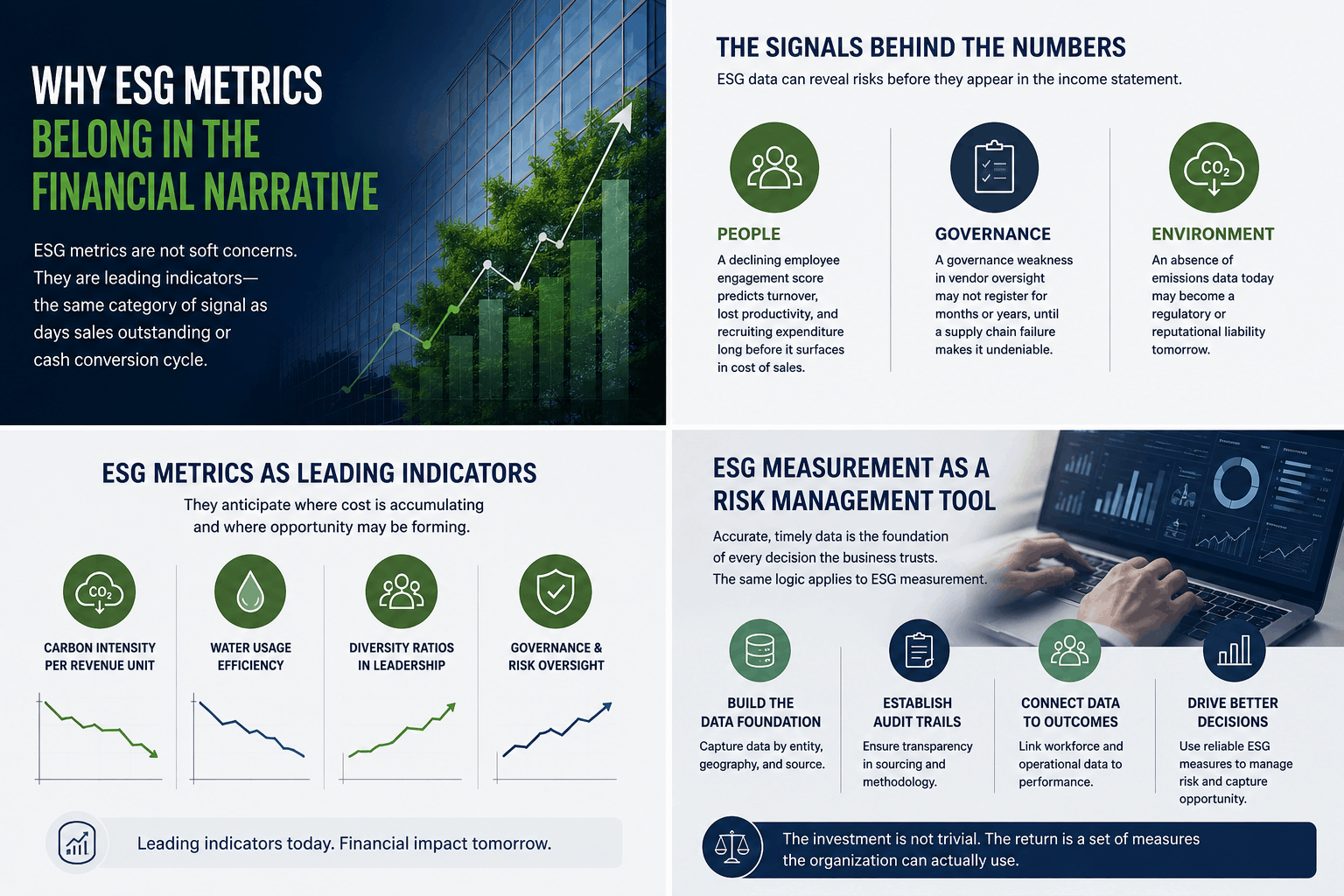

There was a time when the finance function could treat sustainability reporting as a parallel track, maintained by a different team and reviewed by a different audience. That separation is no longer credible. Investors, credit markets, and talent increasingly evaluate organizations through the lens of ESG performance metrics. The CFO who relegates these measures to a footnote misses what they are actually communicating: forward-looking risk.

Consider the signals embedded in ESG data that the income statement has not yet recognized:

- A declining employee engagement score predicts turnover, lost productivity, and recruiting expenditure long before it surfaces in cost of sales.

- A governance weakness in vendor oversight may not register for months or years, until a supply chain failure makes it undeniable.

- An absence of emissions data today may become a regulatory or reputational liability tomorrow.

These are not soft concerns. They are unpriced costs waiting for a trigger.

The CFO role, at its most rigorous, is to see around corners. ESG metrics examples such as carbon intensity per revenue unit, water usage efficiency, or diversity ratios in leadership are not altruistic additions to the financial model. They are leading indicators, the same category of signal as days sales outstanding or cash conversion cycle. They anticipate where cost is accumulating and where opportunity may be forming before either appears in the profit and loss statement.

ESG Measurement as a Risk Management Tool

During my time leading finance for a cybersecurity company, one of the most valuable investments the finance organization made was in the architecture of operational data pipelines. Accurate, timely data was the foundation of every decision the business trusted. The same logic applies to ESG measurement. Without a reliable data infrastructure, what are esg metrics in practice? They are estimates, prone to challenge, difficult to act on, and unconvincing to sophisticated stakeholders.

Building that infrastructure is a CFO-level responsibility. It means establishing audit trails for sourcing decisions, capturing energy and emissions data by entity and geography, and connecting workforce data to performance outcomes. The investment is not trivial. The return, however, is a set of measures the organization can actually use.

Selecting Metrics That Cut to the Core of Culture

Not all ESG metrics carry equal cultural weight. Some sit at the periphery: one-time philanthropy programs, isolated community events, or compliance certifications that have no operational consequence. Others sit at the center: the measures that surface daily in the choices managers make, the vendors the organization selects, the projects it funds. The CFO’s task is to identify the latter and make them visible.

The selection criterion is coherence. What does the organization claim to value? The answer should determine what gets measured:

- The organization must track Scope 1 and Scope 2 emissions per revenue unit with granularity and report them honestly, including when the trend is unfavorable.

- If it advocates for inclusive leadership, the finance team must measure the ratio of women and underrepresented groups at the senior management level consistently, not selectively.

- If governance is the declared priority, board refreshment cycles, internal audit independence, and risk management efficacy must each have an owner and a trendline.

The power of a well-chosen metric lies not in its precision alone but in its consequences. When a CFO raises energy consumption relative to target in a weekly leadership huddle, that act sends an unambiguous message: ESG performance is not a quarterly exercise reserved for the investor deck. It is part of the rhythm of management. When the organization evaluates supply chain partners against sustainability criteria, it signals that its ESG expectations extend outward as well as inward.

Embedding ESG Performance Metrics in Incentive Structures

Culture is not sustained through memo or aspiration. It is sustained through consequence. The most durable signal a CFO can send is to anchor ESG outcomes in compensation design.

When a portion of executive bonus eligibility depends on workplace safety improvements, emissions reductions, or progress on leadership diversity targets, those outcomes stop being optional priorities. They become embedded in the formula. Long-term incentive plan vesting tied to multi-year ESG trajectories creates accountability that survives quarterly earnings pressure. These are not decorative additions to the compensation framework. They are structural commitments.

During the years I led finance for a digital marketing firm that scaled from nine million to one hundred and eighty million dollars in revenue, I learned one clear lesson: what gets measured with financial consequence gets managed with financial discipline.The same principle applies directly to ESG targets. Once they carry economic weight, they attract the same quality of attention as revenue and margin.

Fairness and robustness are prerequisites. Metrics linked to compensation must meet a clear standard:

- An independent audit or assurance process must verify them, so that the numbers the organization rewards reflect the numbers it actually achieved.

- They must be transparent enough to invite comparison across business units and reward genuine progress over time.

- They must cascade beyond the executive tier, so that middle managers can see how their department’s sourcing choices, commuting policies, and resource consumption contribute to the same calculation.

Tying executive bonuses to corporate-level emissions is a reasonable starting point. But the organization gains genuine cultural momentum only when the accountability reaches further down.

The Internal Value of External Disclosure

Disclosure is commonly understood as an outward gesture, a communication to investors, regulators, or the public. Its internal function is equally important and frequently underutilized.

When the CFO commits to quarterly ESG reporting with entity-level breakdowns, that commitment changes what the organization pays attention to between reporting periods. Procurement teams begin asking suppliers to account for their environmental footprint. Engineering teams surface product development options with lower resource intensity. Human resources considers how benefits design affects commuting behavior and workforce composition. The disclosure obligation becomes an organizational discipline.

The CFO can reinforce this effect through selective internal transparency. Sharing ESG dashboards with the broader management population, not only the executive team, creates collective ownership of progress and shortfall alike. Employees who can see where the organization stands are employees who understand that the journey belongs to everyone, not only to those responsible for the report.

This approach requires the right systems. Data pipelines must feed reporting with accuracy. Audit trails must support the claims being made. Analytics must connect diverse data points into coherent narratives. These are technical investments, but they carry cultural returns. A CFO who led the ERP and BI architecture overhaul at a mission-driven education institution, where a forty-eight million dollar capital raise demanded precisely this level of financial and operational rigor, understands that infrastructure and credibility are inseparable.

Leadership Signals and the Architecture of Cultural Change

Metrics and incentives create conditions. Leadership creates conviction. The CFO who defines ESG targets with care but then directs capital allocation without reference to ESG readiness sends a contradictory signal that culture will read accurately.

Consistency of word and action is the standard that matters. Does the CFO evaluate proposed investments against ESG criteria? Does the CFO consider sustainability-linked financing structures when arranging credit facilities? Do external auditors attest to emissions and ethics practices? Does the leadership team make workforce decisions with full awareness of their effect on inclusion goals? These are not rhetorical questions. They are the tests that reveal whether ESG is a strategic priority or a communications exercise.

The proving ground is the routine, not the exceptional. Supply chain renegotiations, vendor onboarding processes, real estate decisions, acquisition due diligence: these are the ordinary events in which ESG considerations either appear consistently or do not appear at all. Having overseen more than one hundred and fifty million dollars in M&A transactions across sectors including gaming, logistics, and cybersecurity, I have seen how easily integration decisions can reinforce or undermine stated organizational values. The diligence process is a moment of cultural declaration, not only financial assessment.

Conclusion

ESG metrics earn their place in the CFO’s toolkit not because they satisfy a reporting obligation, but because they do what the best financial instruments always do: they surface what matters before it becomes expensive to ignore. Selecting the right measures, embedding them in incentive structures, building the data architecture to support credible reporting, and leading with consistency across capital and operational decisions are how metrics become culture. The work is patient and cumulative. It does not announce itself in a single quarter. But for the finance leader who insists that ESG forecasting belongs alongside cash forecasting, that diversity outcomes belong in succession planning rather than only in public relations, and that emissions data belongs in the investment model rather than only in the sustainability report, the organization will eventually reflect what it has been consistently asked to measure. Culture changes slowly, and then all at once.

Disclaimer: This blog is intended for informational purposes only and does not constitute legal, tax, or accounting advice. You should consult your own tax advisor or counsel for advice tailored to your specific situation. Hindol Datta is a seasoned finance executive with over 25 years of leadership experience across SaaS, cybersecurity, logistics, and digital marketing industries. He has served as CFO and VP of Finance in both public and private companies, leading $120M+ in fundraising and $150M+ in M&A transactions while driving predictive analytics and ERP transformations. Known for blending strategic foresight with operational discipline, he builds high-performing global finance organizations that enable scalable growth and data-driven decision-making.

AI-assisted insights, supplemented by 25 years of finance leadership experience.