Executive Summary

Cost transformation strategies separate organizations that adapt quickly from those that remain trapped by decisions made years ago. Many costs labeled as fixed are simply habits that have gone unquestioned. They were once practical choices. Over time they became constraints that limit how quickly an organization can respond to change. This article explores how finance leaders can reshape cost structures rather than simply reduce them. It draws on experience across cybersecurity, SaaS, gaming, logistics, digital marketing, medical devices, and nonprofit organizations, and examines the long-term effects of cost reduction on growth, innovation, and customer experience. The article also explores how leaders can redirect capital toward strategic priorities, how sequencing shapes outcomes, and how benchmarking against industry peers can surface hidden patterns. The goal is to treat cost not as a constraint to manage, but as a structural choice that reflects ambition and shapes what an organization can become.

Reading Cost Structures as a Reflection of Strategic Intent

Finance leaders often treat cost structures as accounting artifacts, lists of line items to revisit once a year. In practice, they reveal far more. They show where an organization has chosen permanence and where it has left room for movement. They reflect decisions about control, risk, and the pace of change that an organization is comfortable with.

Two cost structures with the same total spend can describe very different organizations. One may show comfort with risk and a bias toward speed. The other may show a strong preference for certainty, even where that certainty no longer reflects current conditions.

The split between fixed and variable costs looks mechanical on paper. Rent, salaried labor, and insurance sit on one side. Raw materials, commissions, and transaction based fees sit on the other. In practice, the boundary is far less stable than it appears.

The Line Between Fixed and Variable Is Rarely Permanent

Many costs carry the fixed label only because an organization has allowed them to remain that way. They are commitments that once felt familiar rather than commitments that remain optimal. In a business environment that now shifts faster than most forecasts can anticipate, that familiarity becomes a liability rather than a comfort.

The role of a finance leader in this context is not to slash spending indiscriminately, nor to outsource everything in search of flexibility. It is to question the logic behind permanence itself. Why does the organization own a particular asset. What justifies concentrating headcount in a high cost location. And why keep a support function internal rather than sharing it across the business. These are not cost cutting questions. They are agility questions, and they sit at the center of any serious cost transformation strategy.

Building an Effective Cost Transformation Strategy Around Reshaping, Not Reducing

The most durable cost transformation strategies prioritize reshaping over reducing. Reduction targets a number. Reshaping targets the underlying logic that produced that number in the first place, and it tends to hold up far longer.

This distinction became clear to me during a finance transformation in the nonprofit and education sector, where we reduced monthly burn from eight hundred thousand dollars to two hundred thousand dollars. The result mattered, but the method mattered more. We did not simply remove line items. We questioned long-standing commitments around space, staffing models, and vendor relationships, and we rebuilt the cost base around how the organization actually needed to operate going forward.

Moving From Ownership to Flexibility

In another transformation, a technology business carried more than seventy five percent of its cost base in fixed commitments, and the shift toward agility took a similar form. Infrastructure moved toward consumption based models rather than fixed ownership. Compensation structures incorporated more variable components tied to outcomes. The organization renegotiated long-term software licenses into more flexible arrangements and sublet underused office space.

None of these moves were primarily about saving money in the short term. Each one converted a fixed commitment into something that could expand or contract with the business. Over time, leadership asked departments not only to own their budgets, but to articulate how flexible their spending was and how quickly it could adjust when conditions changed.

Weighing the Long-Term Cost of Cutting Too Quickly

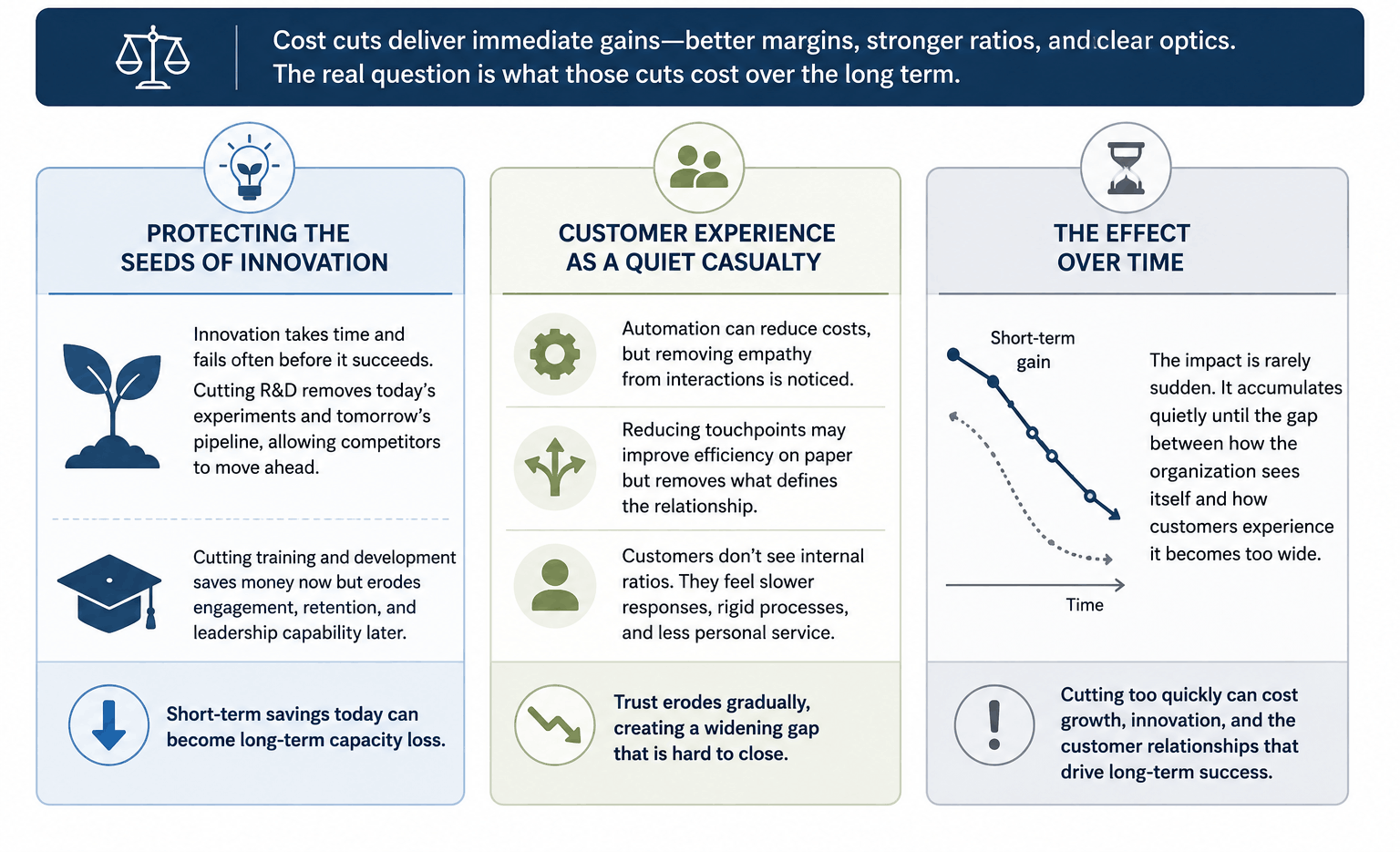

Cost reduction often produces an immediate and visible benefit. Margins improve, ratios look healthier, and the changes are easy to communicate. The more difficult question is what those reductions cost the organization over a longer horizon, particularly when it comes to growth capacity, innovation, and customer experience.

Protecting the Seeds of Innovation

Innovation rarely produces immediate revenue, and it fails often before it succeeds. This makes it an easy target whenever budgets tighten. Yet the experiments removed during a cost cutting cycle often represent the foundation for differentiation several years later. A R&D budget reduced sharply without apparent short-term impact can quietly remove an organization’s future product pipeline, leaving competitors to move ahead unopposed.

The same pattern applies to training and development budgets, which are frequently classified as non-essential during efficiency drives. The financial saving is immediate and visible. The erosion in engagement, retention, and management capability tends to surface months later, by which point it is far harder to trace back to its original cause.

Customer Experience as a Quiet Casualty

Customer experience sits at the sharper edge of cost reduction. Automation can reduce service costs, but if it removes empathy from the interaction, customers notice. Reducing touchpoints can improve efficiency on paper, while quietly removing the qualities that once defined a brand’s relationship with its customers.

Customers do not see internal cost ratios. They experience slower responses, more rigid processes, and less personal service, and they draw their own conclusions from those experiences. The effect is rarely sudden. It accumulates gradually, in the same way that trust accumulates, until a gap opens between how an organization sees itself and how its customers experience it.

Reallocating Capital Toward Strategic Priorities

A core part of any cost transformation strategy is not simply removing spend, but redirecting it. Most cost structures contain pockets of spending that made sense under earlier strategies and earlier constraints, but no longer connect clearly to where the organization is headed.

In one engagement, a detailed review uncovered nearly twelve million dollars in low-yield spend spread across systems support, underperforming partnerships, and procurement contracts that had simply continued by default. None of it was wasteful in an obvious sense. Each item had a history. The opportunity was in converting that spend into something that supported the organization’s current direction.

That capital was redirected toward priorities that included:

- Technology investments that strengthened core operating capability

- Improvements to the customer journey aimed at reducing churn

- Workforce development that preserved institutional knowledge during change

The results were not immediate, but they were measurable over time. Retention improved, response times shortened, and internal confidence grew, because employees could see that leadership was converting savings into investment rather than absorbing them into the budget process.

Not every cost carries the same kind of value, and reallocation works best when this is acknowledged early. Some costs protect relationships. Some provide room for experimentation that has not yet produced results. Removing these without care can weaken parts of the organization that are difficult to rebuild later. The most effective approach treats reallocation less like a single transaction and more like an ongoing editorial process, weighing each adjustment against what it might quietly take away as well as what it visibly returns.

Sequencing Cost Transformation for Lasting Impact

Even a well designed cost transformation strategy can fail if the timing is wrong. Cost reduction introduced before strategic priorities are clear often removes capacity an organization needs just as it begins to move in a new direction. The energy meant to fuel transformation can be spent before transformation truly begins.

The more durable approach sequences cost work after strategy has been clarified and priorities have been sharpened. At that point, cost decisions become an expression of strategy rather than a substitute for it.

Communication plays a quiet but significant role in this sequencing. Stakeholders tend to focus on what is being removed unless leadership shows them, with equal clarity, what is being built in its place. Framing a cost transformation strategy around investment rather than cuts alone changes how it lands internally. People who understand why a change is happening tend to support it, adapt to it, and in some cases improve on it, in ways that no directive could achieve on its own.

Benchmarking Cost Structures Against Industry Peers

Benchmarking offers a useful, if sometimes uncomfortable, perspective on cost transformation. It answers a question that internal analysis alone cannot. How does an organization’s cost structure compare with others operating at a similar scale, and what does that comparison suggest about its readiness to grow.

During a period when I helped scale a digital marketing organization from nine million dollars to one hundred and eighty million dollars in revenue, we rebuilt the cost structure repeatedly to keep pace with that growth. What was efficient at one scale became a constraint at the next, and benchmarking against faster growing peers helped identify where the structure was lagging before it became a visible problem.

Benchmarks as Invitations, Not Verdicts

A cost ratio that sits above or below an industry median is not, by itself, good or bad. High customer service costs may reflect inefficiency, or they may reflect a deliberate investment in experience. Low research and development spend may reflect discipline, or it may reflect underinvestment in future relevance.

The most useful benchmarks tend to be the ones that prompt a deeper question rather than a quick conclusion. A cost-to-revenue ratio that looks favorable at first glance may, on closer inspection, reflect deferred investment in areas such as infrastructure or security, areas that eventually require attention regardless of how the numbers appear today.

The most informative comparisons often come not from the average, but from organizations that scale unusually well. These organizations tend to be deliberate about where they carry weight and where they stay light, choosing carefully what to build internally and what to access through partners. Studying that pattern, rather than simply matching a median, tends to produce more useful insight for an organization working through its own transformation.

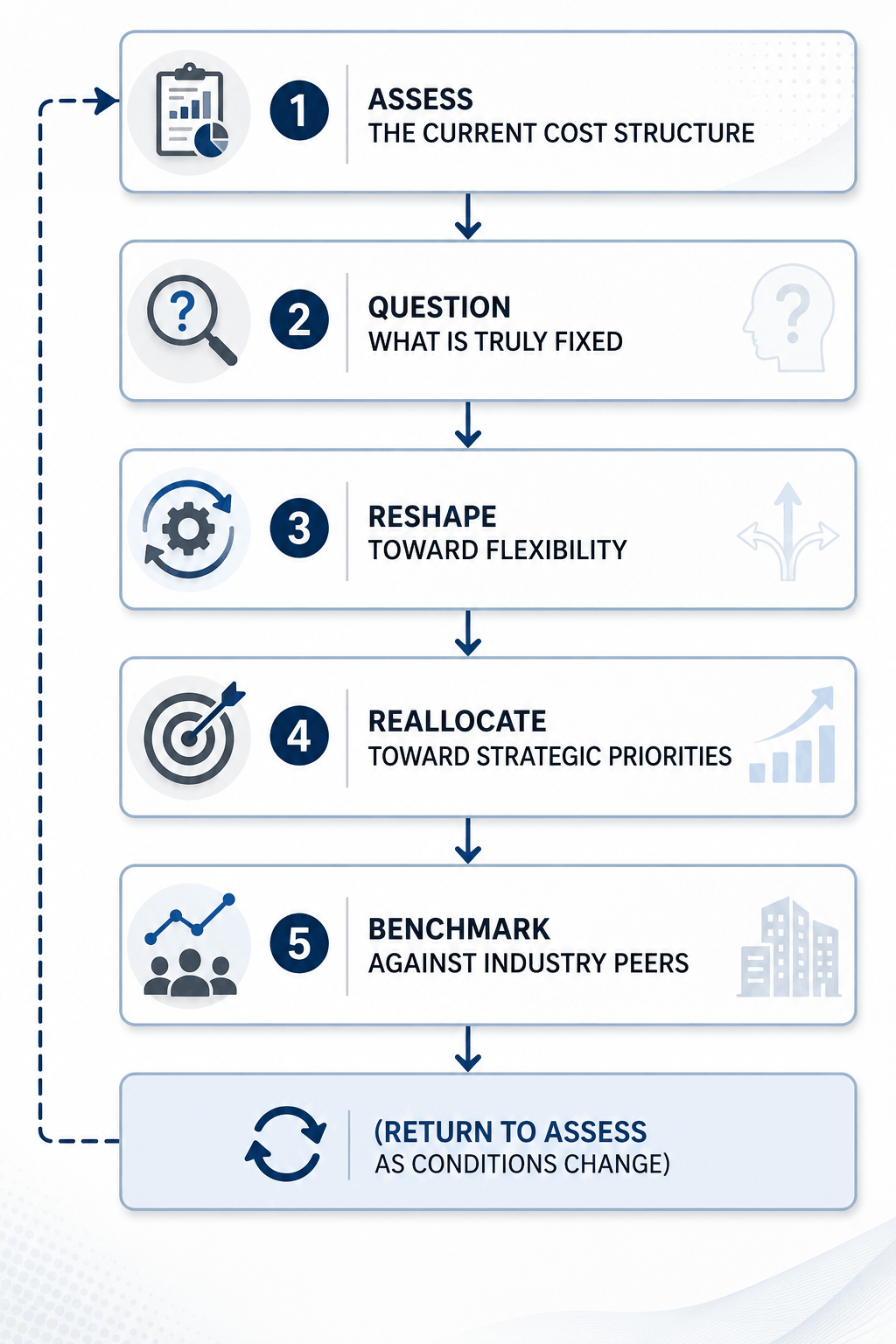

A Simple Framework for Cost Transformation

The pattern across these examples can be summarized as a continuous cycle rather than a single event. The diagram below outlines how the elements connect.

Conclusion

Cost transformation strategies are ultimately about intention rather than arithmetic. The question worth asking is not only what can be trimmed, but what the organization is trying to become, and whether its current cost structure supports that direction. Across cybersecurity, SaaS, gaming, logistics, digital marketing, medical devices, and nonprofit work, the same lesson repeats itself. Costs that are reshaped with purpose tend to support growth, while costs that are simply cut tend to resurface as constraints later, often in areas such as innovation, talent, or customer experience. Reallocating capital toward priorities that matter, sequencing change so that strategy leads rather than follows, and benchmarking honestly against peers all play a role in this process. None of these steps replace the underlying discipline of asking why a cost exists in its current form, and whether it still earns its place. For CFOs and finance leaders, the most valuable habit is treating the cost structure as something to actively shape, review, and adjust, rather than something to inherit and leave unexamined until the next downturn forces the question.

Disclaimer: This blog is intended for informational purposes only and does not constitute legal, tax, or accounting advice. You should consult your own tax advisor or counsel for advice tailored to your specific situation. Hindol Datta is a seasoned finance executive with over 25 years of leadership experience across SaaS, cybersecurity, logistics, and digital marketing industries. He has served as CFO and VP of Finance in both public and private companies, leading $120M+ in fundraising and $150M+ in M&A transactions while driving predictive analytics and ERP transformations. Known for blending strategic foresight with operational discipline, he builds high-performing global finance organizations that enable scalable growth and data-driven decision-making.

AI-assisted insights, supplemented by 25 years of finance leadership experience.