Executive Summary

Every long-lived asset carries a shadow cost: the legal obligation to retire it. Asset retirement obligation accounting under ASC 410 requires organizations to recognize, measure, and accrue for that cost from the moment the obligation is incurred and can be reasonably estimated. Many companies, particularly those operating under lease agreements with restoration clauses or managing capital-intensive physical infrastructure, consistently under-apply this standard.

The consequences range from balance sheet distortions and understated liabilities to costly surprises at lease exit, acquisition diligence, or regulatory review. This article examines the foundation and mechanics of ASC 410, identifies where high-growth and capital-intensive organizations most frequently overlook it, and explains how it connects to broader capital planning and environmental reporting. Drawing on experience across logistics, manufacturing, regulated research facilities, and data infrastructure, the perspective here is operational and grounded in the realities finance leaders actually face.

Why Asset Retirement Obligation Accounting Demands Attention

There is a natural tendency in capital planning to focus on the cost of acquiring and operating an asset. The cost of removing it receives considerably less attention. That imbalance is a structural gap in how many organizations think about asset ownership, and it is one that carries real financial consequences when left unaddressed.

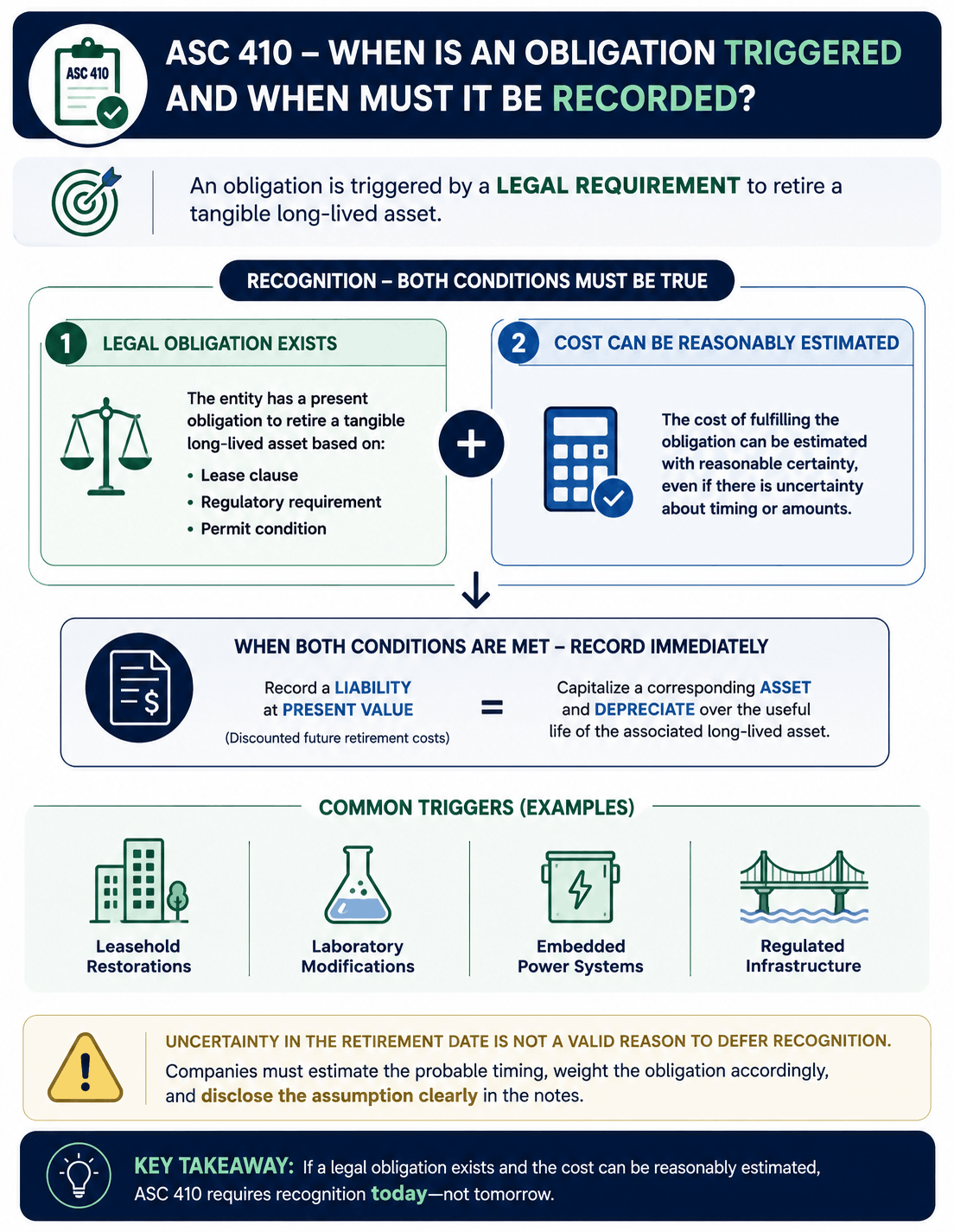

ASC 410 exists to close it. The standard requires entities to recognize a liability for the legal obligation to retire a tangible long-lived asset when the obligation is incurred and the cost can be reasonably estimated. Companies record that liability at present value, capitalize a corresponding asset, and depreciate it over its useful life. Each period, the liability accretes upward, reflecting the increasing proximity of the future settlement.

This is not a concern limited to oil wells and nuclear facilities. Any company that installs specialized equipment, modifies a leased space, or operates in a regulated environment may carry a retirement obligation. Clean rooms, fume hoods, chemical storage systems, reinforced flooring, and embedded power infrastructure are all common triggers. A lease clause requiring restoration upon exit is typically the legal incurrence event. The accounting obligation follows from it directly.

The Mechanics: Recognition, Estimation, and Accretion

Recognition and Initial Measurement

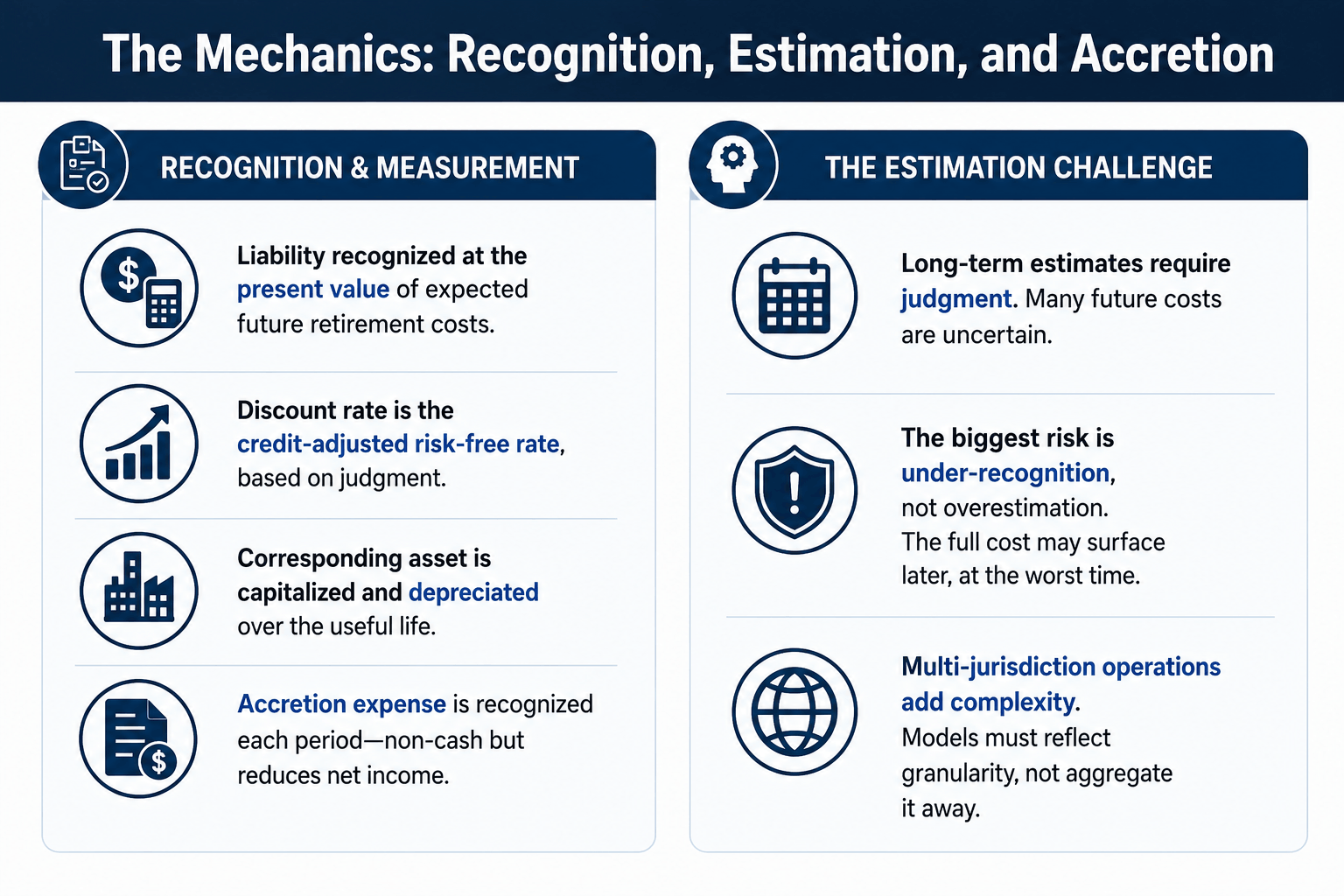

When an asset retirement obligation is identified, the liability is booked at the present value of expected future retirement costs. The discount rate applied is typically the credit-adjusted risk-free rate, a figure that requires genuine judgment. A highly leveraged early-stage company will carry a meaningfully different rate than an established manufacturer, and that difference shapes both the opening balance and the accretion profile over the life of the asset.

The corresponding capitalized asset is depreciated over the useful life of the associated long-lived asset. The accretion expense, recognized on the income statement each period, is non-cash but substantive. It reduces net income and signals that the company is managing with discipline toward an eventual cash settlement.

The Estimation Challenge

Estimating retirement costs fifteen or twenty-five years into the future requires as much judgment as calculation. Future labor rates, permitting costs, regulatory standards, and remediation requirements are all variables. None can be known with precision at the time of initial recognition.

The most common failure mode is not aggressive estimation. It is under-recognition: assumptions made so conservatively that the obligation becomes effectively invisible on the balance sheet. When settlement eventually arrives, the full cost surfaces at once, frequently at the least convenient moment. Companies operating across multiple geographies face further complexity. A renewable energy operator removing equipment across several jurisdictions may face staggered timelines, varying regulatory frameworks, and different labor markets. The model must reflect that granularity, not aggregate it away.

Where the Standard Is Most Often Missed

High-growth companies are particularly vulnerable. The operational focus on revenue traction and product development creates blind spots around physical infrastructure. The obligation, however, does not wait for the organization to be ready for it.

In one situation I encountered during an advisory engagement, a research-intensive company had made significant modifications to a leased facility over several years. The company had installed specialized ventilation systems, chemical storage, and environmental controls under a lease that required full restoration upon exit. No one had accrued the retirement obligation. When management terminated the lease ahead of schedule, an estimated two and a half million dollars hit the income statement at once. A liability that should have been recognized and accreted over years arrived as a single, disruptive line item.

The root cause was not careless accounting. Legal, facilities, and finance had simply not coordinated to identify the lease clause as a trigger for ASC 410 recognition. That coordination is a governance matter as much as a technical one.

Environmental liabilities add a further dimension. Companies in sectors claiming sustainability leadership face pointed questions from investors when decommissioning costs are absent from the balance sheet. The failure to recognize these obligations is increasingly visible in diligence reviews and ESG evaluations alike. Accretion expense, presented transparently and connected to asset lifecycle planning, signals financial stewardship. Relegating it to footnotes invites exactly the scrutiny that transparency would prevent.

Capital Planning Implications

Recognizing an asset retirement obligation changes the economics of the original investment decision. The question is no longer only whether the organization can afford the asset. It is whether the organization can afford the asset and its eventual exit.

In capital budgeting discussions, the inclusion of retirement costs forces a more complete evaluation of full lifecycle return. Depreciation of the capitalized retirement asset, accretion of the liability, and the eventual cash settlement all affect return metrics and investment hurdle rates. For capital-intensive businesses, these numbers belong in the analysis from the beginning, not discovered at the point of exit.

In my experience building financial operating models and capital approval frameworks across sectors including logistics, manufacturing, and data infrastructure, organizations that integrate retirement planning into their capital review processes make consistently better investment decisions. They are also meaningfully better positioned when auditors, acquirers, or investors examine the balance sheet.

Conclusion

Asset retirement obligations are not a back-office accounting matter. They are a statement of how an organization understands the full arc of its asset base. Finance leaders who recognize, measure, and communicate these obligations clearly demonstrate stewardship that extends well beyond technical compliance. The obligation is incurred at inception. The discipline to account for it is a choice. Every CFO overseeing capital-intensive operations, regulated facilities, or leased spaces with restoration clauses should treat ASC 410 not as a burden but as a tool. It sharpens capital decisions, disciplines balance sheet presentation, and signals to investors and acquirers alike that the organization can carry what it builds all the way to its conclusion.

Disclaimer: This blog is intended for informational purposes only and does not constitute legal, tax, or accounting advice. You should consult your own tax advisor or counsel for advice tailored to your specific situation.

Hindol Datta is a seasoned finance executive with over 25 years of leadership experience across SaaS, cybersecurity, logistics, and digital marketing industries. He has served as CFO and VP of Finance in both public and private companies, leading $120M+ in fundraising and $150M+ in M&A transactions while driving predictive analytics and ERP transformations. Known for blending strategic foresight with operational discipline, he builds high-performing global finance organizations that enable scalable growth and data-driven decision-making.

AI-assisted insights, supplemented by 25 years of finance leadership experience.