Executive Summary

Cash runway and burn rate are among the most consequential metrics a CFO manages. Burn rate reveals the velocity of capital consumption. Runway converts that velocity into a countdown. Together, they frame every strategic decision the organization makes, from hiring to fundraising to market expansion. Yet the challenge is not calculating these numbers. It is connecting them to a credible, ground-up growth forecast that earns the trust of boards, investors, and leadership teams. This article explores the discipline behind that connection, drawing on over twenty-five years of executive experience across cybersecurity, SaaS, gaming, logistics, digital marketing, medical devices, and nonprofit sectors. Forecasting is not an act of optimism. It is an act of operational precision. The CFO who masters it transforms cash burn from a source of anxiety into a strategic instrument.

Understanding the Metrics That Drive Strategic Clarity

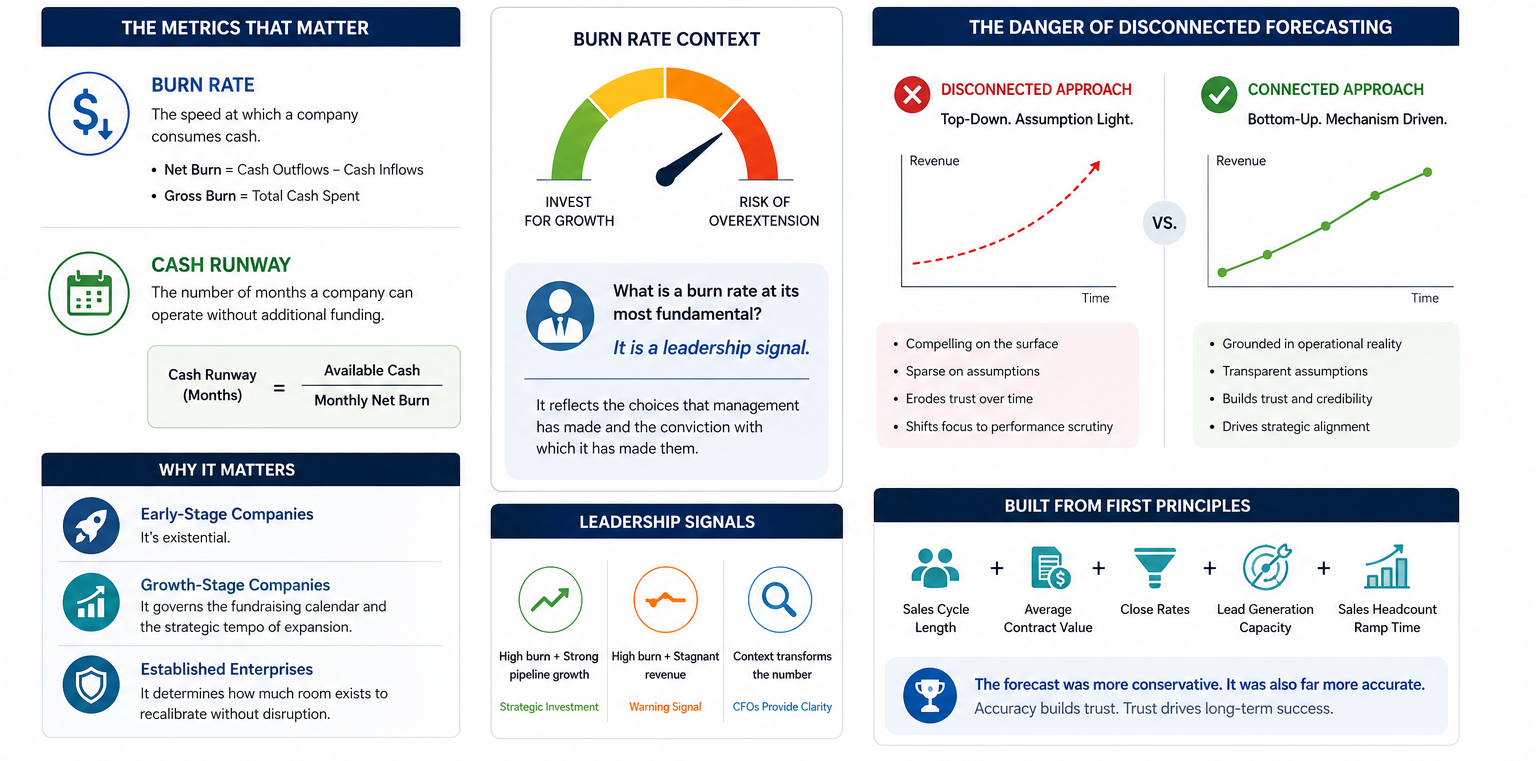

Burn rate represents the speed at which a company consumes its available cash. It is a deceptively simple figure. Net burn is the difference between cash outflows and cash inflows in a given period. Gross burn captures total cash spent, independent of revenue. Both matter. Together, they reveal how aggressively a company is investing in its own future and how much time it has to generate returns before capital runs out.

Cash runway follows directly from burn rate. Divide available cash by monthly net burn and the result is the number of months a company can sustain operations without new funding or material revenue acceleration. For early-stage companies, this number is existential. Growth-stage companies, it governs the fundraising calendar and the strategic tempo of expansion. For established enterprises navigating a capital markets shift, it determines how much room exists to recalibrate without disruption.

What is a burn rate, then, at its most fundamental? It is a leadership signal. It reflects the choices that management has made and the conviction with which it has made them. A high burn rate in a period of strong pipeline growth reads differently than a high burn rate against a backdrop of stagnant revenue. Context transforms the number. The CFO’s role is to supply that context with precision and transparency.

The Danger of Disconnected Forecasting

The most common failure in financial planning is the disconnect between a revenue forecast and the operational reality beneath it. Boards and investors have seen this pattern many times. A compelling top-down projection derived from market size arrives without the supporting mechanics. The growth chart rises sharply. The assumptions behind it are sparse.

This approach may be persuasive in the short term. Over time, it erodes trust. When actuals fall short of projections, the conversation shifts from strategic alignment to performance scrutiny. Credibility, once damaged, is rebuilt slowly and at significant cost.

During a period leading a SaaS company through a rapid international expansion, the temptation to lead with headline growth was real. Instead, the financial model was rebuilt from first principles: sales cycle length, average contract value, close rates, lead generation capacity, and sales headcount ramp time. The resulting forecast was more conservative than the board initially preferred. It also proved far more accurate. That accuracy became the foundation of a relationship built on trust rather than hope.

The lesson is durable across sectors. Whether in cybersecurity, logistics, or digital marketing, a forecast that is grounded in operational mechanics consistently outperforms one built from market aspiration.

Building a Forecast That Earns Belief

A credible growth forecast begins with revenue mechanics.

- What is the current pipeline?

- What is the average deal size?

- What is the close rate by stage?

- How many qualified opportunities are being generated per month, and what programs produce them?

- How many quota-carrying salespeople are active, and what is their ramp time to full productivity?

These questions are not glamorous. They are essential. They anchor the revenue forecast to testable, observable inputs. When actuals diverge, the model reveals where and why. That transparency is what separates a living financial model from a static projection.

The next layer connects revenue to headcount. If bookings are forecast to double, what does that require in sales support, customer success, implementation, finance, and engineering? Each incremental dollar of revenue carries an operational footprint. Ignoring that footprint produces a forecast that looks sound on the surface and breaks down in execution.

Costs must be modeled with equal discipline. Variable costs rise with volume. Step-function costs appear at scale thresholds. Infrastructure expenses in cloud-based environments track closely with usage. Every line item deserves scrutiny. Is this cost fixed or variable? What triggers a step change? What is the sensitivity of total burn to changes in volume or timing? These questions transform a static budget into a dynamic planning instrument.

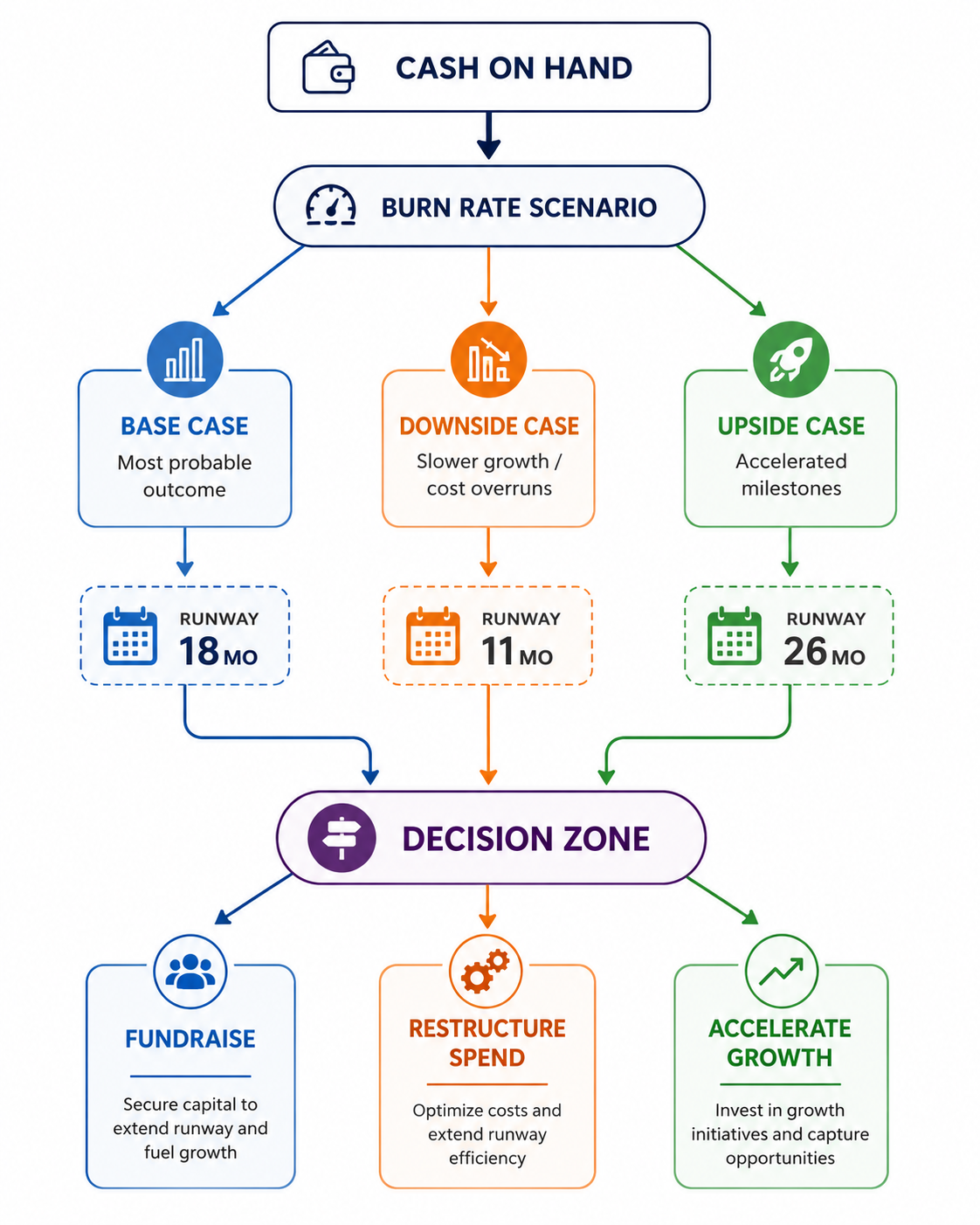

The Three-Scenario Framework

One of the most effective planning tools for managing cash runway is the three-scenario model. The base case reflects the most probable operating outcome given current pipeline, team capacity, and market conditions. The downside case accounts for slower customer acquisition, delayed hiring, or cost overruns. The upside case captures the potential of accelerated growth if key milestones are hit ahead of schedule.

This framework communicates something important to investors and boards. Management is not locked into a single narrative. It has thought through the range of outcomes and has a response prepared for each. That dynamic posture builds confidence. It demonstrates that the company understands its own levers.

The diagram below illustrates how the three scenarios translate into different runway profiles, reinforcing why ground-up assumptions matter for every case:

Each scenario path demands a distinct strategic response. The CFO who has modeled all three arrives at board conversations prepared, not reactive.

Communicating with Precision and Humility

Numbers do not speak for themselves. The CFO must give them language. When presenting a financial forecast, measured language builds more trust than confident assertion. Sharing assumptions rather than conclusions invites dialogue. Acknowledging where the model is strong and where it is fragile demonstrates intellectual honesty.

A lesson learned early in executive practice: overpromising may win the room once. It weakens the relationship over time. When targets are missed, the conversation changes in tenor and in tone. The forecast becomes a source of tension rather than a tool for alignment.

The better approach is to treat the forecast as a floor, not a ceiling. Positive surprises above the plan build momentum. They compound into credibility over successive quarters. Investors and boards remember the CFO who delivered more than was promised, just as they remember the one who repeatedly fell short.

Equally important is the practice of sharing forecast evolution over time. When the model changes, explaining why demonstrates learning and agility. It prevents the perception that numbers are being managed rather than reflected. It reinforces the narrative that management is becoming more precise as the business matures.

Operating Metrics as the CFO’s Early Warning System

Revenue is an outcome. What drives it is a set of observable, measurable leading indicators. Pipeline health. Sales conversion rates. Customer onboarding speed. Net revenue retention. Support response time. These metrics tell the story before the numbers confirm it.

The most effective financial leaders build dashboards that surface these drivers in real time. During a period of finance and analytics leadership at a cybersecurity company, the enterprise KPI framework tracked bookings, utilization, backlog, recurring revenue, pipeline health, customer margin, and retention across a multi-entity global structure. That visibility enabled early course corrections before variance reached the income statement.

This approach also strengthens investor communication. Rather than waiting for quarterly results, management can share leading indicators that signal trajectory. Investors who see the right metrics moving in the right direction develop confidence in the business model, not just the most recent period.

When the Market Shifts: The Discipline of Recalibration

Capital markets do not remain static. In periods of abundant capital, growth commands a premium. Investors reward revenue multiples. Burn rate is accepted as the cost of ambition. In periods of capital constraint, the calculus reverses. Profitability, burn multiples, gross margin, and contribution margin become the metrics that determine valuation and investor appetite.

Companies that can navigate both modes are the ones that endure. Those that cannot adjust become cautionary cases.

This transition is never comfortable. It requires slowing hiring, repricing or renegotiating contracts, exiting non-core markets, and refocusing product investment. More than any of that, it requires the courage to present a revised narrative to the board and investors, one that honestly acknowledges that yesterday’s strategy is no longer viable in today’s conditions.

During a period of growth-first strategy at a digital marketing organization, revenue scaled from single-digit millions to well over one hundred million dollars over a compressed timeframe. That scale was possible because the financial model was built to support it, connecting every dollar of spend to a measurable growth outcome. When market conditions changed in other assignments, the same discipline applied in reverse: every line of cost was tied to a specific value driver, and anything that could not demonstrate that connection was a candidate for reduction.

The experience that runs across these transitions, from a forty-eight-million-dollar capital raise at a mission-driven education institution to overseeing over one hundred million dollars in gaming sector acquisitions, is this: the quality of the financial model determines the quality of the decisions made from it. A rigorous model supports sound decisions in growth and in constraint alike.

Credibility as the Currency of Financial Leadership

Forecasting is not primarily a technical discipline. It is a leadership act. The forecast tells the organization where it is going. It sets the expectations against which performance is measured. It frames every hiring decision, every capital allocation choice, every conversation with an external partner or investor.

A good forecast does not guarantee the future. It prepares the company to respond to it. That preparation is what transforms runway cash from a countdown into a planning horizon. It is what transforms burn rate from a risk signal into a measure of intentional investment.

Investors are seeking coherence. They want evidence that the business understands how capital converts into milestones. Also, how the management has thought through setbacks and has considered a response. They are not looking for guarantees. They are looking for a leadership team that knows what it knows, knows what it does not know, and is honest about both.

That honesty, sustained over time and reflected in actual results, is what builds the relationships that sustain companies through cycles of growth and constraint.

How often should a CFO update the burn rate and runway forecast?

Burn rate and cash runway should be reviewed at minimum on a monthly basis, aligned with the close of each accounting period. In high-growth or capital-constrained environments, a rolling thirteen-week cash flow model updated weekly provides a more responsive view of the operating position. The forecast itself, including scenarios and key assumptions, should be formally revisited with the board on a quarterly basis or whenever a material change in business conditions warrants it, such as a significant shift in customer acquisition pace, an unexpected cost event, or a change in the fundraising timeline. The goal is not to produce a static document but to maintain a living model that reflects the current state of the business with enough lead time to act before options narrow.

Conclusion

Cash runway and burn rate are not metrics to be managed for appearances. They are instruments of strategic clarity. When a CFO builds a forecast grounded in operational mechanics, communicates it with transparency, and updates it with intellectual honesty as conditions evolve, those metrics become a source of confidence rather than anxiety. The discipline required is not merely financial. It is organizational. It demands that leadership understand the dependencies within the business, the levers available for adjustment, and the conditions that would trigger a change in strategy. Across twenty-five years of financial leadership spanning cybersecurity, SaaS, gaming, logistics, digital marketing, medical devices, and nonprofit sectors, the single most consistent finding is this: credibility is built not by predicting the future accurately, but by preparing for it thoughtfully. That preparation is what turns capital into outcomes and ambition into lasting value.

Disclaimer: This blog is intended for informational purposes only and does not constitute legal, tax, or accounting advice. You should consult your own tax advisor or counsel for advice tailored to your specific situation.

Hindol Datta is a seasoned finance executive with over 25 years of leadership experience across SaaS, cybersecurity, logistics, and digital marketing industries. He has served as CFO and VP of Finance in both public and private companies, leading $120M+ in fundraising and $150M+ in M&A transactions while driving predictive analytics and ERP transformations. Known for blending strategic foresight with operational discipline, he builds high-performing global finance organizations that enable scalable growth and data-driven decision-making.

AI-assisted insights, supplemented by 25 years of finance leadership experience.