Executive Summary

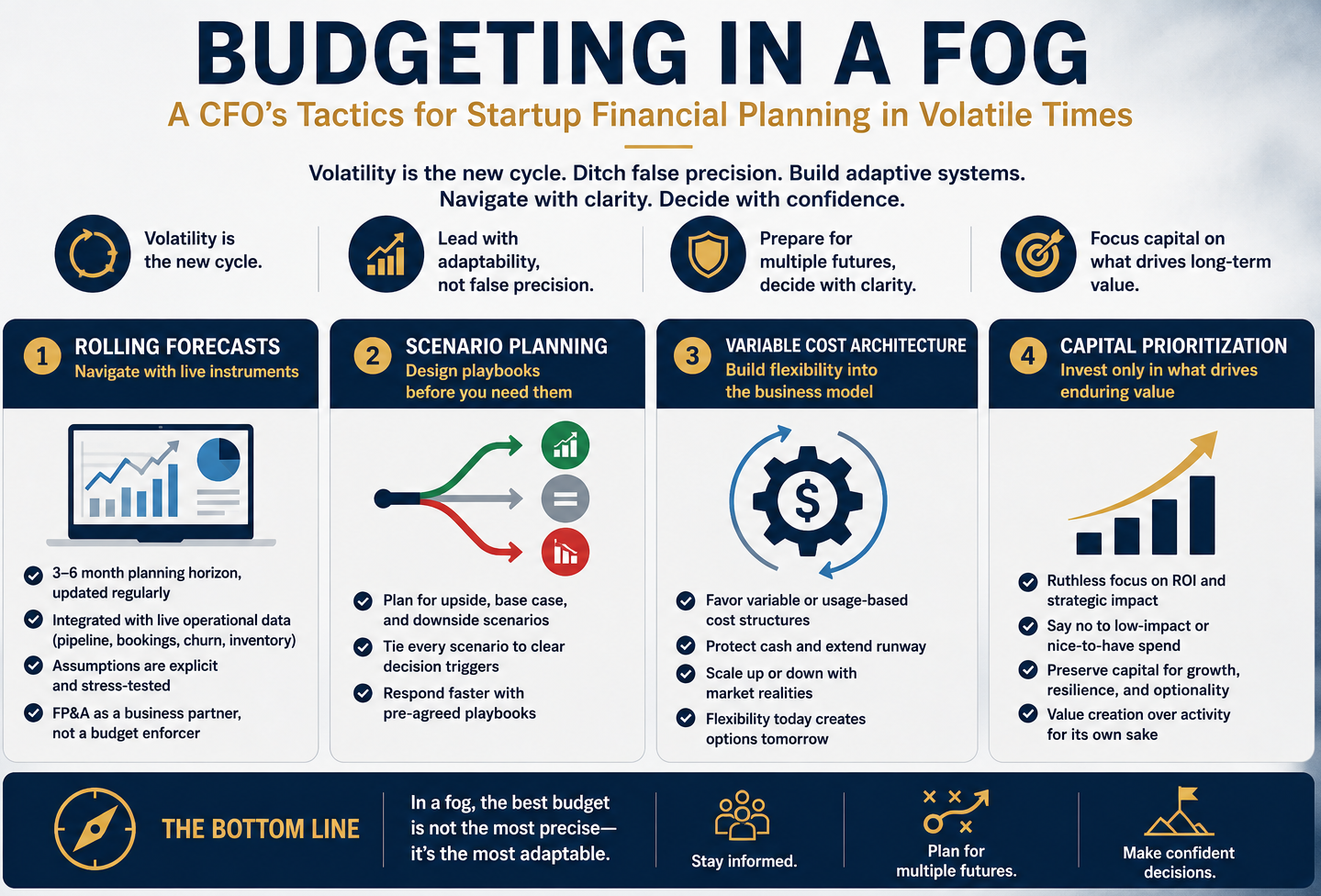

Volatility is no longer an episode in the business cycle. It is the cycle. For finance leaders navigating startup financial planning and high-growth environments, this reality demands a fundamental rethinking of how we budget. The traditional annual plan, built for a world of assumed predictability, is inadequate for an era of supply disruptions, shifting consumer behavior, and macroeconomic uncertainty. This article makes the case for a new budgeting paradigm grounded in rolling forecasts, scenario modeling, variable cost architecture, and disciplined capital prioritization. Drawing on over twenty-five years of CFO and VP Finance experience across cybersecurity, SaaS, gaming, logistics, and nonprofit sectors, the following pages offer a framework for finance leaders who must steer with confidence even when visibility is limited. Budgeting in a fog is not about accepting less. It is about building more.

The World That Budgeting Was Built for No Longer Exists

There is a certain comfort in the annual budget. For decades, it served its purpose because the world honored the assumptions baked into it. Costs behaved predictably, contracts closed on schedule, and the macroeconomic environment generally respected internal plans. That world is gone. The finance leaders who succeed today are not those who build more elaborate spreadsheets but those who build more adaptive frameworks. Having guided finance organizations through cybersecurity scale-ups, global logistics operations, SaaS expansions, and a nonprofit with an exponential mandate, one truth has remained constant. The quality of decisions in uncertainty matters far more than the precision of the plan. The CFO’s role has evolved from financial steward to strategic navigator, and navigation in fog requires different instruments than navigation in clear skies.

The Illusion of Precision

Precision in volatile budgets is often a mirage. A forecast projecting a 7.3 percent increase in second-quarter marketing spend creates an impression of rigor. In practice, it is false confidence dressed up in decimal places. When inflation is unstable, and consumer behavior shifts with every macro headline, granularity does not reflect sophistication. It reflects wishful thinking.

Early in my career, working alongside consulting practices where analytical rigor was both craft and expectation, I learned that the most dangerous number in a financial model is one that everyone believes without questioning its assumptions. Across every industry since, the finance leaders who commanded the most credibility were those who led with calibrated uncertainty rather than manufactured precision. Structure remains essential, but it must be built on rolling forecasts, scenario ranges, and explicit assumptions that can be examined, debated, and updated.

Rolling Forecasts: Navigating with Live Instruments

In sailing, you do not navigate fog with last year’s chart. You use the instruments available in the moment. Rolling forecasts are the financial equivalent. Rather than defending a twelve-month plan against the reality that contradicts it, they allow finance to maintain a living view of the company’s trajectory, updated as real operational data arrives.

During my tenure leading finance and analytics at a fast-growing cybersecurity and identity access management firm, one of the most consequential decisions was building an enterprise KPI framework delivering live data on bookings, pipeline health, customer margin, utilization, and retention. What that architecture enabled was not just reporting. It enabled decision-making at cadence, without waiting for the quarterly close to confirm what the business already knew. In practice, the rolling forecast model requires:

- Shorter planning horizons of three to six months, updated monthly or quarterly

- Tight coupling with live operational data: pipeline, bookings, churn, and inventory levels

- Explicit documentation of key assumptions so they can be stress-tested as conditions shift

- A redefined FP&A role as business partner rather than budget enforcer

At an interim CFO engagement with a high-growth SaaS company, the most meaningful contribution was not building the financial model itself but redesigning the conversation between finance and business unit leadership. Once operators understood the forecast as a living dialogue rather than a binding sentence, the quality of information flowing in improved dramatically, and so did the quality of decisions flowing out.

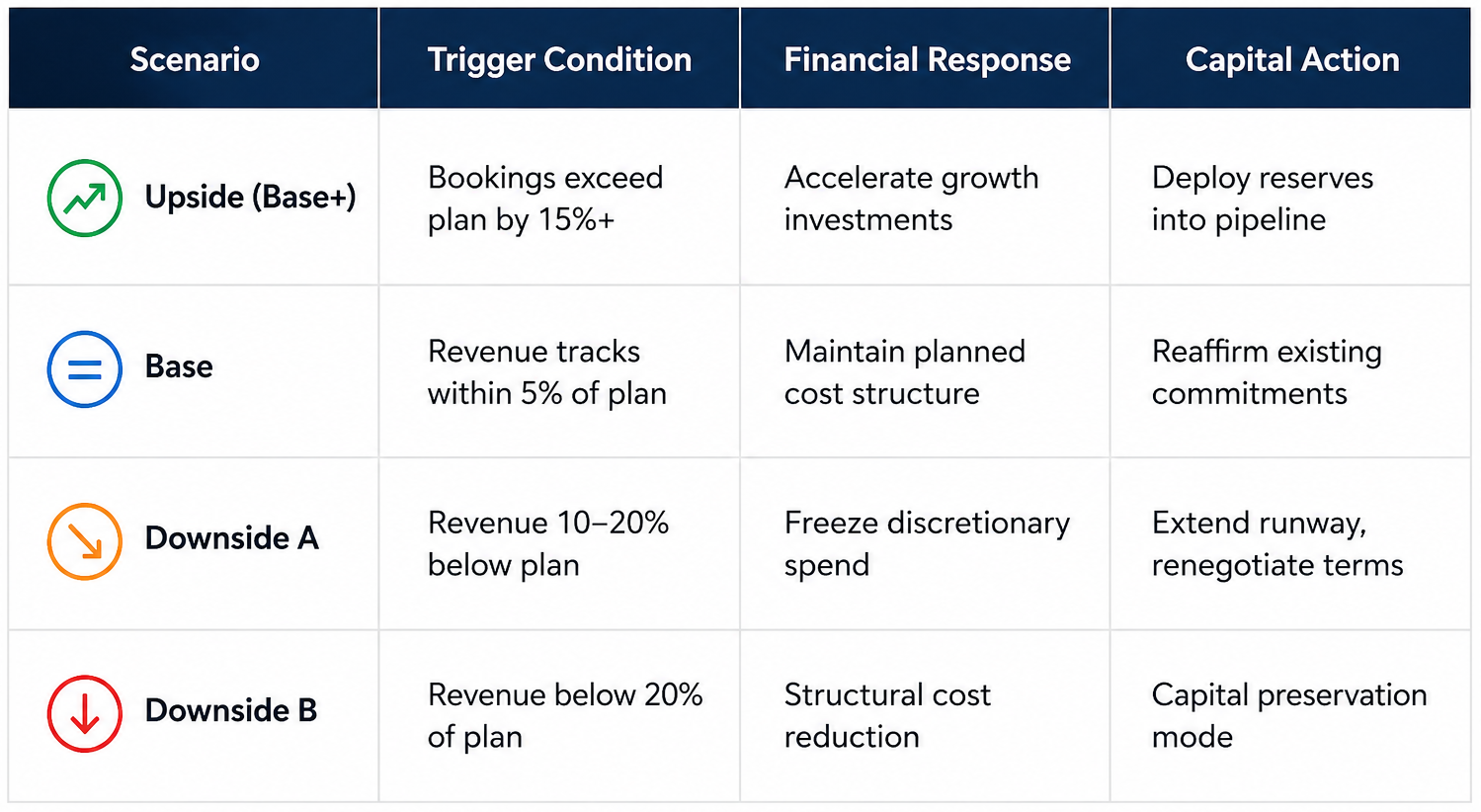

Scenario Planning: Designing Playbooks Before You Need Them

When visibility is low, you do not bet on a single outcome. You plan for a range of them. Scenario planning is the discipline that translates this principle into organizational readiness, answering the questions leadership will inevitably face: What happens to cash flow if European revenue declines by twenty percent? How do margin targets hold if supply costs increase for two consecutive quarters? These are stress tests, and they build the institutional muscle memory that allows organizations to respond with clarity rather than panic.

The critical discipline is ensuring every scenario is tied to a decision set. A scenario without an action plan is simply an interesting forecast. Below is the framework I have used across multiple executive roles to give boards a structured way to think about scenario-response logic:

The value of this framework is not the table itself. It is the conversation that forces before a crisis arrives. When leaders have already agreed on what Downside B looks like and what it requires, the decision to execute becomes faster, less emotional, and far more coordinated.

Variable Cost Architecture: Building Flexibility into the Business Model

Budgeting for volatility is not primarily about cutting costs. It is about designing the cost structure to move with the business. There is a meaningful difference between a company that slashes expenses in a downturn because it has no other option and one that activates pre-designed flexibility because it planned for that possibility.

One of the clearest examples comes from an engagement in the cannabis manufacturing sector, where regulatory timelines were entirely outside management control. Rather than building a fixed cost base, the approach structured operations with contingent labor, usage-based vendor agreements, and a compliance infrastructure that could scale up or stand down as operational approvals permitted. That architecture kept the company financially viable through delays that would have been fatal to a less flexible structure. Finance leaders across industries can apply the same logic:

- Shifting fixed marketing commitments to performance-based channels

- Structuring vendor contracts with volume tiers or exit provisions

- Using contingent labor in functions where volume is uncertain

- Tying executive compensation to real-time business performance rather than plan adherence

Capital Prioritization: The Real Work of Volatile Budgeting

When conditions are uncertain, the instinct is to freeze. In practice, this rarely succeeds. In business, time lost is opportunity lost. Companies that allocate resources strategically during periods of uncertainty consistently emerge stronger than those that don’t. The most effective response is disciplined prioritization. Not all costs carry equal strategic weight, and not all growth initiatives deserve equal patience.

Across a career that has included scaling a digital marketing firm from nine million to one hundred and eighty million dollars in revenue, managing over one hundred and fifty million dollars in merger and acquisition transactions, and raising more than one hundred and twenty million dollars in capital, the consistent lesson is that capital allocation discipline is the single most consequential financial practice in a volatile environment. Budgeting in uncertain conditions is not an expense containment exercise. It is a capital allocation exercise. Every dollar in the budget is an implicit endorsement of the initiative it funds.

The CFO as Communicator: Translating Uncertainty for Stakeholders

In volatile periods, the CFO’s communication responsibilities expand alongside the analytical ones. Boards want to know how leadership is adapting. Investors expect transparency, not false confidence. The CFO must become a skilled translator of uncertainty.

Having led investor relations through a forty-eight-million-dollar capital raise at a mission-driven education institution, one consistent observation stands out: boards and investors do not punish leaders for uncertainty. They punish leaders for surprises. Effective communication in volatile times operates across three registers:

- Clarity: describing the specific variables being modeled and the range of outcomes they produce

- Candor: acknowledging where margin targets may be at risk under certain conditions

- Calm: demonstrating that the organization has runway and a decision-making framework independent of any single scenario

Thinking in Probabilities: The Mental Model Beneath the Framework

Behind every technique in this article is a more fundamental shift. The best CFOs think in probabilities rather than certainties, operating more like investors than scorekeepers. They assign confidence levels to forecasts, account for fat-tail risks, and update their views as new data arrives rather than defending prior positions.

A career beginning at a major public accounting firm and a global management consulting practice instills deep respect for methodological precision. But it also teaches that models are only as good as their assumptions. The transition to operating CFO sharpened a further insight: the value of financial analysis lies not in the output itself, but in the quality of judgment it supports. Budgets are not destinations. They are the best maps available today, subject to revision as the landscape changes. Finance teams incentivized to protect point estimates will hide emerging risks. Finance teams incentivized for transparency and analytical quality will surface them in time to act.

Conclusion

Fog in business is not always the enemy. It reveals which leaders can navigate without a clear horizon and distinguishes organizations built for genuine resilience from those built only for favorable conditions. The CFO who thrives in volatile conditions has built a planning infrastructure that functions without requiring certainty. They communicate with disciplined honesty rather than manufactured confidence, and allocate capital only after thinking through the full range of possible outcomes. Whether navigating startup financial planning with limited runway, managing a multinational enterprise, or stewarding a mission-driven institution through structural change, the principle is the same: budget as though every dollar carries strategic weight, every scenario deserves a response plan, and every forecast is simply the best picture available today. You will not eliminate the fog. But you will learn to move through it with purpose, and that is what the organizations on the other side of this uncertainty will remember.

Disclaimer: This blog is intended for informational purposes only and does not constitute legal, tax, or accounting advice. You should consult your own tax advisor or counsel for advice tailored to your specific situation.

Hindol Datta is a seasoned finance executive with over 25 years of leadership experience across SaaS, cybersecurity, logistics, and digital marketing industries. He has served as CFO and VP of Finance in both public and private companies, leading $120M+ in fundraising and $150M+ in M&A transactions while driving predictive analytics and ERP transformations. Known for blending strategic foresight with operational discipline, he builds high-performing global finance organizations that enable scalable growth and data-driven decision-making.

AI-assisted insights, supplemented by 25 years of finance leadership experience.